Eng

Eng

Taxes and Taxation

Reference:

Kaplina, E.S. (2025). Financial offside: tax risks of the sports industry. Taxes and Taxation, 2, 23–43. . https://doi.org/10.7256/2454-065X.2025.2.73670

|

Library

|

Your profile |

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.|

Taxes and Taxation

Reference:

Kaplina, E.S. (2025). Financial offside: tax risks of the sports industry. Taxes and Taxation, 2, 23–43. . https://doi.org/10.7256/2454-065X.2025.2.73670

Financial offside: tax risks of the sports industry

DOI: 10.7256/2454-065X.2025.2.73670EDN: FUUKFPReceived: 12-03-2025Published: 04-05-2025Abstract: The article discusses current issues of tax risks arising in the sports industry in the context of the phenomenon referred to as "financial offside". The main factors of the tax risks are considered, including the imperfection of legislation and the practice of minimizing tax obligations by sports organizations. Special attention is paid to the differences in taxation of non-profit and commercial organizations operating in the sports industry. The research covers the theoretical foundations of taxation of sports industry organizations, including the structure of the sports sector, the theoretical and practical features of tax accounting are studied and summarized. The subject of the study is the peculiarities of taxation of organizations involved in the sports industry. The analysis of key tax aspects is carried out, such as accounting for sponsorship, depreciation of fixed assets, accounting for management expenses and the risks of retraining relationships with the self-employed into labor. The author concludes that "financial offside" creates significant tax risks in the sports industry. The analysis revealed gaps and contradictions in legislation that make it difficult for both non-profit and commercial organizations to operate. For non-profit structures, the main risks are associated with incorrect accounting of sponsorship, management costs and depreciation. Commercial organizations face problems of illegal optimization, including the illegal write-off of modernization costs, the retraining of advertising costs, and the risks of renegotiating contracts with self-employed trainers into an employment relationship. The scientific novelty lies in the proposed recommendations for improving the regulatory framework regarding the qualification of sponsorship, marketing services and management costs. It also suggests ways to document contracts with self-employed trainers to mitigate business risks. Keywords: tax risks, financial offside, sports industry, taxation, commercial organizations, non-profit organizations, self-employed coaches, sponsorship assistance, targeted financing, marketing expensesThis article is automatically translated. You can find original text of the article here. The modern sports industry is an entire architecture of entities that not only provide services in the field of sports, but also serve this industry [1]. In a broad sense, the sports industry is an autonomous part of the service sector, including organized multi–level activities carried out through information, communication and intellectual processes, and possessing both common and specific characteristics inherent only to it [2]. It includes not only sports competitions within the framework of professional sports and high-performance sports, but also actively developing mass and student sports, as well as media sports as a separate trend from 2023. These entities cannot function without infrastructure, logistics, media space and advertising [3], therefore they are also integral elements of the structure of the sports industry (Figure 1).

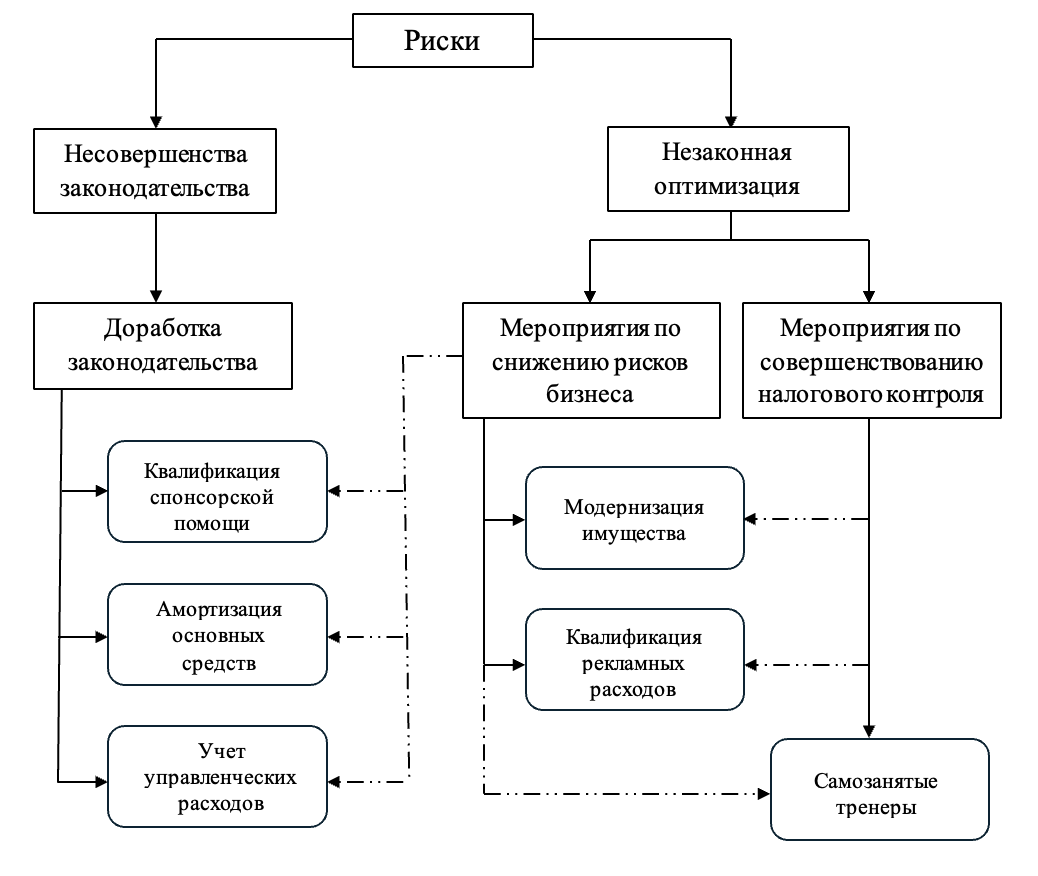

Source: compiled by the author. Figure 1. The structure of the sports industry The object of research in this article will be the segment of mass sports. All sports organizations are represented in various organizational and legal forms and have different goals of activity, among which commercial and non–profit organizations stand out. The modernization of the sports industry and the lack of industry-specific tax legislation in Russia create a "favorable" ground for tax risks. One of these risks is "financial offside", which is a situation where an organization finds itself in a tax risk zone if it crosses the border between acceptable and questionable financial transactions. Offside can occur both in commercial organizations seeking to maximize profits through optimizing tax payments, and in non-profit organizations, where inattention to accounting and the composition of tax bases can lead to excessive tax obligations. As a result, "financial offside" jeopardizes not only the budget, but also the image of the organization. In the scientific literature, the issues of taxation of sports are considered, as a rule, through the prism of double taxation (non-taxation) of athletes [4-7]. Moreover, a significant number of articles investigate the taxation of certain representatives of sports – football players [8]. Thus, Isaeva Yu.A. and Machekhin V. A., in the framework of the study of cross-border taxation of athletes, refer to the problems of applying the OECD Model Convention in the practice of forming mechanisms for taxation of income from international activities [9]. Very little attention is paid to the taxation of legal entities. In particular, E.B. Chernobrovkina, analyzing tax incentives in the field of physical education and sports, comes to the conclusion that "mass, as well as children's and youth sports, sports for the elderly and low-income citizens, and sports as a means of rehabilitation and socialization of citizens should become priorities for stimulation" [10]. Mistineva N. Yu., studying the areas of foreign tax incentives for sports that are priority for implementation, postulates the need to strengthen state support for small businesses in the development of physical education and sports organizations [11]. Similarly, the importance of state support and tax policy for the development of sports is emphasized by Egorova Z. A. and Iglin A.V., paying special attention to direct and indirect taxes in the sports industry [5]. Special attention is paid to the issues of taxation of non-profit organizations, including those represented in the field of the sports industry [12-14]. An analysis of foreign literature shows that the issues of taxation and risk management in sports organizations are considered through the prism of financial management and economic models of sports leagues, with an emphasis on optimizing tax regimes and risk management strategies [15-18]. The purpose of this article is to investigate the nature of tax risks in the sports industry, identify the main mechanisms of their occurrence and propose measures to minimize them. Characteristics of tax risks in the field of non-commercial sports. Tax risks in the sports industry are classified into two groups: imperfect legislation and illegal optimization (Figure 2).

Source: compiled by the author. Figure 2. Groups of tax risks and mechanisms for their elimination In this figure, the author presents a classification of tax risks specific to the sports industry, indicating both general groups and specific types of risks. The main categories include imperfect legislation and illegal optimization, each of which necessitates the use of appropriate tax risk management mechanisms. Figure 2 shows the channels of influence of various tax risk management mechanisms.: The direct impact is shown in solid lines and demonstrates a direct causal relationship between risks and mechanisms for their elimination.; The indirect impact is represented by dotted lines and reflects the indirect impact of the relevant management tools on tax risks. The proposed scheme illustrates an integrated approach to tax risk management in the sports industry, taking into account both legislative aspects and practical tax control mechanisms, which will be discussed later in the article. Each of the risk groups is more applicable to a specific type of organization. For example, non-profit organizations do not aim to maximize profits by optimizing tax obligations, so their activities will address the risks associated with imperfect tax legislation. Non–profit organizations (NPOs) play a significant role in the economy and represent one of the forms of organizational and legal activity. The term "non-profit organizations" usually refers to various structures, including non-governmental organizations, public associations, civil initiatives, charitable foundations and other elements of the third sector of the economy [19]. The main feature of NPOs is that their activities are not focused on making a profit, and entrepreneurial activity is aimed only at the implementation of statutory goals [20]. The share of non-profit organizations in the total volume of sports industry organizations is shown in Figure 3.

Source: compiled by the author on the basis of data from the [System of Professional Analysis of Markets and Companies (SPARK)]. Figure 3. Structure of sports organizations by purpose of activity in 2024 The financing of NGOs is carried out from certain sources: - membership fees if the NGO is based on membership; - voluntary donations or contributions; - funds for targeted financing. In accordance with Article 251 of the Tax Code of the Russian Federation (hereinafter referred to as the Tax Code of the Russian Federation), funds donated to non-profit organizations to support their activities and fulfill their statutory obligations are not taken into account when determining income for calculating income tax. Any income that is not listed in this list is considered non-realized according to paragraph 8 of Article 250 of the Tax Code of the Russian Federation as "gratuitously received property (works, services) or property rights, except for the cases specified in Article 251 of the Tax Code of the Russian Federation." The income tax base of NPOs is formed only when they carry out commercial activities that are not related to the main objectives of the organization. Such income must be accounted for separately and taxed in a generally prescribed manner. Targeted financing expenses and current expenses are not included in expenses when determining the income tax base [Letter of the Ministry of Finance of the Russian Federation dated 03/23/2021 No. 03-07-11/20568]. It is the issue of determining targeted and non-targeted revenues that is at the forefront in determining tax risks [21]. Risk 1. Qualification of sponsorship Within the framework of non-profit organizations, it is necessary to consider the concept of "Sponsorship". This is one of the types of financial assistance provided to NGOs for the implementation of certain types of activities [22]. This characteristic of sponsorship as an institutional financing mechanism is fully reflected in the activities of sports NGOs. Empirical data demonstrate that this type of revenue, along with targeted financing, is a system-forming element of the revenue side of sports organizations, while the commercial component remains secondary (Figure 4).

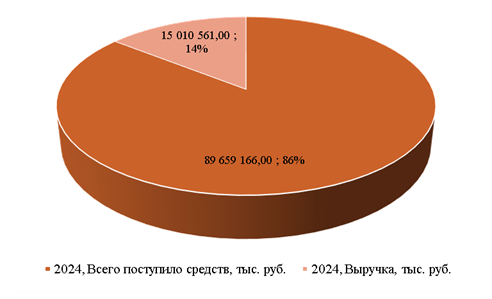

Source: compiled by the author on the basis of data from the [System of Professional Analysis of Markets and Companies (SPARK)]. Figure 4. Distribution of income sources of organizations: comparative analysis of external financing and own revenue in 2024 As follows from the presented figure, targeted financing and sponsorship play a dominant role in the income structure of sports non-profit organizations (a sample of 4,500 companies was analyzed) (86%), while revenue from commercial activities accounts for only 14% of total revenue. This confirms the thesis about the high dependence of the Russian sports sector on external financing, which corresponds to the global practice of NGO functioning in sports. However, sponsorship can sometimes involve some mutually beneficial terms for the sponsored person, as the sponsor provides assistance in exchange for publicly promoting their brand. This process is recognized as a form of advertising, and the sponsor is considered an advertiser [Information Letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated December 25, 1998 No. 37 "Review of the practice of dispute resolution related to the application of advertising legislation"]. Based on this provision, if funds are received from a sponsor in accordance with a contract for the provision of paid sponsorship (including advertising services) and are recognized by the sponsoring organization as other advertising expenses (according to Article 264 of the Tax Code of the Russian Federation), then such receipts are considered as sales income for NPOs and are taken into account when calculating the tax base [Letter Ministry of Finance of the Russian Federation from 26.12.2008 № 03-03-06/4/102], [ Letter from the Department of Tax and Customs and Tariff Policy of the Ministry of Finance of the Russian Federation dated January 17, 2013 N 03-03-06/4/5 "On accounting for the purposes of taxation of profits of organizations of funds received by a public organization under a contract on sponsored advertising"]. However, if a sponsorship agreement is concluded between a sponsoring organization and an NGO, such income is not included in the profit tax base of the non-profit organization, and the sponsor, in turn, does not reduce its tax base (paragraphs 16 and 34 of Article 270 of the Tax Code of the Russian Federation). The main problem is that at the legislative level, the concept of "gratuitous sponsorship" is not fixed, so there is a risk of including this type of income in the corporate income tax base. For most non-profit organizations involved in the field of sports, sponsorship is the main source of income. The inclusion of gratuitous sponsorship in taxable income will significantly reduce the available resources and the level of activity of the organization. In this regard, it is important to provide NGOs with more freedom and opportunities to generate income, which is then used for social purposes. In this case, sponsorship received for statutory purposes may be exempt from taxation [23]. Risk 2. Depreciation of fixed assets For proper taxation, it is critically important to keep separate records of expenses: expenses covered by earmarked funds are not subject to taxation, unlike expenses related to business activities. Considering expenses such as depreciation of fixed assets acquired through targeted financing and used in both statutory and commercial activities, it is important to note that it is impossible to take into account even a part of depreciation, since there is no established procedure for dividing depreciation charges. Risk 3. Accounting for management expenses The expenses of non-profit organizations also include management expenses. Their specificity lies in the fact that they are aimed at carrying out all types of activities of the organization. In this regard, NPOs run the risk of overstating the income tax base, since the Tax Code of the Russian Federation does not include provisions regulating the allocation of management expenses (salaries and accruals of administration and management personnel, rental of premises) to expenses carried out at the expense of targeted financing [Resolution of the Federal Antimonopoly Service of the North-Western District dated 07/06/2009 in case no. A56-50333/2008]. If we consider Articles 252 and 272 of the Tax Code of the Russian Federation, then in accordance with them, proportional division of expenses can be made only by types of activities aimed at making a profit. In the case of NPOs, these articles do not apply due to their main statutory activities. Following Article 313 of the Tax Code of the Russian Federation, an organization has the right to independently determine the tax accounting system and methods of maintaining separate accounting, however, the lack of an unambiguous approach to this procedure leads to tax risks. Thus, the identified tax risks of non-profit organizations are largely due to gaps and imperfections in current legislation, which creates additional difficulties in their activities. However, problems related to tax regulation are typical not only for NPOs, commercial organizations also face a number of tax risks that have their own specifics and are associated with illegal optimization of tax obligations. Mechanisms for eliminating identified tax risks in the non-profit sports industry Elimination of risk 1. Qualification of sponsorship In order to unambiguously recognize gratuitous sponsorship, it is proposed to introduce a new subparagraph 1.2 to paragraph 2 of Article 251 of the Tax Code of the Russian Federation in the following wording: "targeted funds transferred to non-profit organizations under a contract of gratuitous sponsorship and aimed at carrying out their statutory activities." Similarly, to reduce this risk, it is proposed to introduce a new subparagraph 34.1 in Article 270 of the Tax Code of the Russian Federation in the following wording: "in the form of expenses incurred by a non-profit organization aimed at carrying out its statutory activities, moreover, the source of financing for the expenses incurred is gratuitous sponsorship." In addition to the above, it is necessary to consolidate the concept of "gratuitous sponsorship" at the legislative level and establish clear criteria for the exemption of these types of income and expenses from taxation, namely: - a sponsorship agreement providing for the gratuitous and voluntary nature of the assistance, indicating the specific purposes of its provision and the obligation to use it for these purposes; - the act of receiving and transferring the provided assistance; - documents confirming the registration of assistance; - reporting by the recipient, demonstrating the intended use of the funds received. These recommendations will help to eliminate the risk of underfunding of non-profit organizations, whose activities are mainly carried out at the expense of targeted revenues. Risk elimination 2. Depreciation of fixed assets In order to distribute depreciation of fixed assets used in commercial and non-commercial activities, it is proposed to amend subparagraph 2 of paragraph 2 of Article 256 of the Tax Code of the Russian Federation concerning depreciable property. Taking into account the addition, the sub-item will look like this: "The following types of depreciable property are not subject to depreciation: 2) property of non-profit organizations received as targeted income or acquired at the expense of targeted income and used for non-commercial activities; if the property is used for both statutory and commercial purposes, depreciation of property is included in expenses in proportion to the proceeds from commercial activities in the total revenue, including targeted financing and commercial activities". To calculate the share of depreciation of property that is used for both statutory and commercial purposes, it is recommended to follow the following guidelines: 1. Determine the annual depreciation of property Depreciation is usually calculated based on the original cost of a property and its expected useful life. Linear depreciation calculation formula: "Annual depreciation = The initial value of the property / Useful life." 2. Determine the share of revenue in the total income from targeted financing and commercial activities It is necessary to determine how much of the income the property generates from commercial activities. 3. Calculate the share of depreciation from commercial activities To determine the share of depreciation from commercial activities, it is necessary to multiply the annual depreciation by the share of revenue in the total income from targeted financing and commercial activities.: "The share of depreciation from commercial activities = Annual depreciation * The share of property used for commercial purposes." The proposed method is based on the decision of the Arbitration Court and allows for the correct division of depreciation of property between commercial and non-commercial activities for accurate and fair taxation [Decision of December 5, 2019 in case No. A70-19872/2018]. Risk management 3. Accounting for management expenses Due to the inconsistency of the legislation, it is proposed to keep proportional records of management expenses financed by targeted and commercial funds from non-profit organizations. This method of accounting will allow NPOs to include management expenses in the composition of expenses that reduce the tax base in proportion to the share of income from commercial activities in the total income from commercial and statutory activities [Letter of the Ministry of Finance of the Russian Federation dated January 23, 2015 No. 03-03-06/4/2051 ]. In order to eliminate this risk, it is proposed to make adjustments to paragraph 4 of paragraph 1 of Article 272 of the Tax Code of the Russian Federation "The procedure for recognizing expenses using the accrual method". Taking into account the changes, the subparagraph will look like this: "The taxpayer's expenses, which cannot be directly attributed to the costs of a specific type of activity, are distributed in proportion to the share of the corresponding income in the total amount of all taxpayer's income." Characteristics of tax risks in the field of commercial sports Sports commercial organizations are an important element of the sports industry. They combine sports agencies, professional clubs, and fitness clubs, which in turn are interconnected with individuals and individual entrepreneurs who provide their services to sports clubs. In accordance with Article 50 of the Civil Code of the Russian Federation, legal entities of various forms of ownership are recognized as commercial organizations, the main purpose of which is to make a profit [The Civil Code of the Russian Federation (Part One): Federal Law No. 51-FZ]. Within the framework of this article, in the context of commercial organizations, fitness clubs providing services in the field of the sports industry, the number of which is about 10,000 organizations, will be considered directly. Risk 4. Costs of upgrading non-depreciable property According to paragraph 1 of Article 256 of the Tax Code of the Russian Federation, which establishes criteria for classifying property as depreciable, many organizations have difficulties accounting for the costs of repairing and modernizing facilities that do not meet these requirements. In accordance with this standard, only property with a value exceeding 100,000 rubles and a useful life of more than one year can be classified as depreciable. In fitness clubs, the key objects of fixed assets are often exercise equipment, the cost of which in some cases does not reach the minimum threshold for accounting for taxation and depreciation purposes. Let's take an example: the CardioPower X48 elliptical trainer, which costs 89,900 rubles. According to the classifier, sports equipment belongs to the second depreciation group, where the SPI is from two to three years inclusive. Let's assume that the useful life of the simulator is set at 36 months (3 years). The organization has upgraded this equipment by installing a new motor worth 30 thousand rubles. However, the Tax Code does not provide clear guidance on the possibility of depreciation on such improvements and accounting for them as expenses to reduce the tax base. In this situation, two risks arise: for the organization, an increase in the tax base due to the inability to take into account depreciation on this equipment, and for the tax authorities, the risk of underpayment of tax revenues if the company nevertheless begins to calculate depreciation. In this situation, there are two approaches to solving this issue.: 1. Write-off of the cost of modernization as part of material expenses According to subparagraph 3 of paragraph 1 of Article 254 of the Tax Code of the Russian Federation, if the property does not meet the criteria for recognizing it as depreciable (cost less than 100 thousand rubles and useful life of more than 12 months), its value is subject to a one-time write-off as part of material expenses at the time of commissioning. In relation to the case under consideration, the cost of upgrading the simulator can also be attributed to expenses in the tax (accounting) period in which the upgrade was carried out. For example, if a fitness club purchased a simulator in February 2025 and upgraded it in the same month, then in the first quarter of 2025 the total amount of expenses (89,900 rubles for the simulator and 30,000 rubles for the upgrade) in the amount of 119,900 rubles may be reflected in other expenses related to production and implementation [Letter of the Ministry of Finance of the Russian Federation dated March 25, 2010 N 03-03-06/1/173 ]. 2. Depreciation after modernization An alternative approach is based on the fact that if, before the modernization, the value of the fixed asset did not exceed 100 thousand rubles, but the useful life was more than 12 months, and as a result of the modernization, its value exceeded the established limit, such property can be considered depreciable. In this case, the cost of modernization increases the initial cost of the facility, and expenses are accounted for through depreciation over the remaining useful life [Letter of the Ministry of Finance of Russia dated 06/17/2021 No. 03-03-06/1/47706 ]. This approach requires compliance with the conditions established by the tax legislation for the recognition of property as depreciable, and can be applied only if modernization has led to a significant change in the characteristics of the object. If we take the previous example with the purchase and modernization of equipment in one reporting period, then the organization will write off 6,661 rubles to expenses for the first quarter of 2025. ((89 900 + 30 000) / 36 * 2 = 6 661). If we consider the option when the simulator was purchased in December 2024 and immediately written off as non-depreciable property, and the modernization was carried out on it in January 2025, then this simulator can be transferred to depreciable property, and the cost of modernization measures will be taken into account as part of the expenses [Letter from the Ministry of Finance of the Russian Federation dated 06/17/2021 № 03-03-06/1/47706 ]. Calculation example: 89,900 were written off in December 2024 in full as part of expenses, and depreciation on the modernization facility begins to accrue from February 2025. Depreciation for the 1st quarter of 2025: 30 000 / 32 * 2 = 1 875 rubles. The most reasonable approach seems to be the one in which property is recognized as depreciable if its value reaches the minimum threshold (100 thousand rubles) as a result of modernization, which makes it possible to account for expenses through depreciation over the entire useful life. The use of this method ensures an even distribution of the tax burden and minimizes the risks of significant fluctuations in the tax base that occur when the full cost of equipment is written off at one time in one reporting period and there are no corresponding expenses in subsequent periods. This becomes especially relevant in situations where an organization purchases and upgrades several pieces of equipment, which can lead to significant deviations in the amount of taxable profit between reporting periods. Thus, the gradual write-off of costs through depreciation contributes to the stability of financial planning and reduces tax risks. Risk 5. Retraining of advertising expenses into marketing expenses Fitness clubs actively invest in marketing and advertising campaigns aimed at attracting new customers and retaining existing ones. Although the share of these costs is not dominant in the overall cost structure, their proper accounting and optimization are of particular importance from the point of view of tax planning and minimizing fiscal risks. The presented graph (Figure 5) shows the indicated distribution of expenses of fitness clubs by main items (a sample of 3,100 organizations).

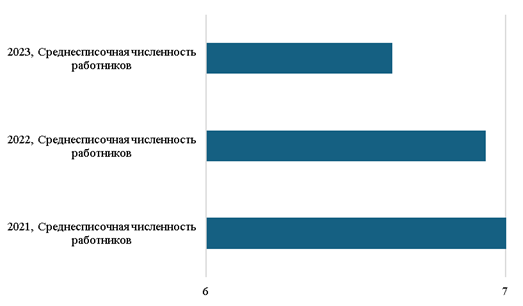

Source: compiled by the author on the basis of data from the [System of Professional Analysis of Markets and Companies (SPARK)]. Figure 5. Cost structure of fitness clubs in 2024 The analysis of the cost structure of fitness clubs revealed a characteristic feature of the distribution of financial flows. As follows from the presented data, the main share of expenses falls on two main cost items: cost of sales and management expenses. At the same time, the share of commercial expenses, which usually include marketing and advertising, is only 1% of the total cost structure. It is important to note that companies can account for marketing expenses on account 26, in which case they will be included in management expenses. Thus, the actual amount of marketing costs of sports organizations may be higher. However, despite the relatively small volume, these expenses represent a strategically important element of the functioning of organizations in the fitness industry. Their special importance is due to their key role in ensuring sustainable business development, which requires as much attention to their planning and accounting as to the main items of expenditure. The accounting procedure for such expenses is regulated by paragraph 4 of Article 264 of the Tax Code of the Russian Federation. Advertising expenses are divided into two types: non-regulated, which can be fully included in expenses (for example, advertising in the media, outdoor and light advertising), and regulated, which are accounted for within 1% of revenue (for example, expenses for prizes within promotions). According to paragraph 27 of Article 264 of the Tax Code of the Russian Federation, the costs of marketing activities can be recognized in full. However, in the context of the modern variety of advertising tools, it is often difficult for organizations to correctly classify such expenses. The tax legislation does not contain clear guidelines regarding the documentary confirmation of marketing services, and the term "marketing" itself is absent from the Civil Code of the Russian Federation. This creates the risk for organizations of incorrectly attributing advertising-related expenses to marketing services, which can lead to an overestimation of the expenditure side and, as a result, to an unjustified reduction in the income tax base. In such a situation, it is particularly important to carefully analyze and justify the nature of expenses, as well as to develop clear criteria for their classification in order to minimize tax risks. In order to reduce the risk of retraining advertising expenses into marketing expenses, organizations need to clearly define the type of expense to which marketing services belong and draw up the following documents [Letter from the Ministry of Finance of the Russian Federation dated December 27, 2007 N 03-03-06/2/238 ]: - regulation on marketing policy; - development of a promotion strategy; - the manager's order to conduct an advertising campaign; - contracts with a detailed description of the advertising content; - certificates of completed works; - documents confirming the placement of advertising (especially on social networks: extracts and reports from advertising cabinets, screenshots of pages on the Internet, documents confirming the traffic of the advertising campaign). - documents confirming the payment. Risk 6. Self-employed trainers: retraining of GPH contracts An analysis of the personnel structure of fitness clubs shows that personal trainers make up the bulk of those employed in these organizations. However, only a small part of them, according to expert estimates, no more than 15-20%, are registered under an employment contract. The vast majority of trainers (80-85%) work as self–employed or individual entrepreneurs, which is confirmed by data from the official websites of large fitness club chains, where there are about 20-30 trainers per club, while service and management personnel also have a place to be (https://www.kommersant.ru/doc/6621984 , accessed: 03/27/2025). Data on the average number of employees of fitness clubs for the period 2021-2023 (Figure 6) shows a downward trend in officially employed personnel, but these figures reflect only a part of the personnel structure, mainly including administrative staff.

Source: compiled by the author on the basis of data from the [System of Professional Analysis of Markets and Companies (SPARK)]. Figure 6. Official average number of employees of commercial organizations in the sports industry This disparity indicates two key trends.: ¾ the desire of fitness clubs to minimize expenses on medical equipment and taxes through the use of flexible forms of employment; ¾ the predominance of non-standard labor relations in this segment of the sports industry. Since 2024, the Federal Tax Service (FTS) of Russia has strengthened control over the activities of fitness clubs, paying special attention to the legality of the registration of employment relations with trainers. The main focus of the tax authorities is aimed at identifying cases when coaches register as self-employed or individual entrepreneurs in order to minimize the tax burden, including personal income tax evasion and insurance premiums [24]. In case of confirmation of such facts, fitness clubs face recalculation of tax obligations, as well as the application of financial sanctions in the form of fines. This situation highlights the need for strict compliance with labor legislation when registering employment and civil law relations with staff. Currently, the National Fitness Community is actively debating with the tax authorities regarding the qualifications of the agency function of fitness clubs. Clubs position themselves exclusively as suppliers of equipment and facilities for sports activities, however, the tax authorities identify a number of risk–oriented signs indicating the possible existence of an employment relationship. These features include: a fixed monthly salary, the absence of a clearly defined work result, the presence of a single source of income for the contractor, a strictly defined work schedule, the complete dependence of the contractor on the customer's infrastructure, the coverage of operating expenses by the fitness club, the absence of self–employed persons from other clients, as well as the performance of work directly related to the main activities of the club. [Resolution of the Arbitration Court of the North-Western District of November 28, 2023 N F07-15491/23 in case N A56-122617/2022]. These factors may indicate the presence of signs of an employment relationship, which raises disputes about the legality of using the agency model in this area. One of the key tools for minimizing the risk of retraining civil law contracts with the self–employed into an employment relationship is a detailed and correct formulation of the terms of such contracts. In order to exclude claims from the tax authorities and prevent the recognition of an employment relationship, fitness clubs need to clearly state the following aspects in the contract:: - the self-employed independently determines the work schedule; - the self-employed is responsible for the result of the work; - self-employed provides the services of an independent contractor; - self-employed uses their own equipment [Decision of November 17, 2023 in case no. A55-18527/2023]; - lack of subordination and indicate that the fitness center does not have the right to give orders and control the process of performing services, except within the framework of the contract; - describe the procedure and conditions for termination of the contract, emphasizing that the contract is not an employment contract and is not regulated by the Labor Code.; - indicate that the self-employed is independently responsible for paying taxes and fees related to their activities.; - emphasize that the self-employed are not entitled to the social guarantees provided for employees (paid leave, sick leave); - the self-employed is obliged to provide certificates of completed works or other documents confirming the provision of services and their payment. Proper and detailed consolidation of these conditions in the text of the contract will eliminate the possibility of interpreting the relationship between the fitness club and the self–employed as labor, thereby minimizing the risk of claims from the tax authorities. This approach ensures legal certainty and reduces the likelihood of re–qualification of civil law relations into labor relations, which contributes to compliance with the norms of tax and labor legislation. Conclusion Financial offside is a serious problem for the sports industry, creating significant tax risks. The analysis revealed significant gaps and contradictions in the current legislation, which create difficulties for both non-profit and commercial organizations. In particular, for non-profit organizations, the key risks are associated with incorrect sponsorship qualifications, difficulties in accounting for management expenses and depreciation of fixed assets. For commercial organizations, the main problems are the illegal optimization of the tax burden, including the illegal allocation of expenses for the modernization of non–depreciable property, the retraining of advertising expenses into marketing, as well as the risks of retraining civil law contracts with self-employed trainers into labor relations. To minimize these risks, it is necessary to improve the regulatory framework, including a clear definition of key concepts such as "sponsorship" and "marketing services", and due attention should be paid to documenting contracts with self–employed trainers. The elimination of the identified problems will not only reduce tax risks, but also create more transparent and sustainable conditions for the development of the sports industry in Russia. The scientific novelty of this study is to build a comprehensive model for classifying the tax risks of the sports industry, including mechanisms for their elimination and channels of influence of the appropriate mechanism on the management of a specific risk. References

1. Zadneprovskaia, E. L., Eremina, E. A., & Shpirnia, O. V. (2023). Finance and taxation in the field of physical culture and sports. Kuban State University of Physical Culture, Sports and Tourism.

2. Arkalov, D. P., & Litvin, A. V. (2023). Economic aspects of sports: Models of optimal resource allocation: Monograph. Udmurt University. 3. Sydyhalieva, A. S., & Isakov, Z. M. (2021). Legal regulation of taxation in the field of television broadcasting of sports events. Bulletin of the Kyrgyz-Russian Slavic University, 3, 109-116. 4. Isaeva, Y. A. (2020). Causes and consequences of double taxation of income of representatives of the entertainment and sports industry from international activities. Economics and Business: Theory and Practice, 2-1, 109-112. https://doi.org/10.24411/2411-0450-2020-10098 5. Egorova, Z. A., & Iglin, A. V. (2013). Problems of taxation in the field of sports. Power, 6, 147-150. 6. Vostrikova, V. A. (2022). International taxation in professional sports. Young Scientist, 24, 187-191. 7. Leshchenko, Y. A. (2017). Current issues of international taxation of athletes’ income (based on materials from the Republic of Belarus). In Actual problems of legal regulation of sports legal relations: Collection of materials of the VII All-Russian scientific and practical conference with international participation (pp. 174-183). Ural State University of Physical Culture. 8. Averchenko, N. S. (2024). On the taxation of football players' income: A comparative legal analysis. Scientific Notes of Young Researchers, 12(1), 14-21. 9. Isaeva, Y. A., & Machekhin, V. A. (2018). Taxation of artists and athletes receiving income through star-companies: OECD approach in foreign countries. In Spring Science Days of HSEM: Collection of reports of the International Conference of Students, Postgraduates, Young Scientists, X International Scientific and Practical Forum of Young Tax Experts (Vol. 2, pp. 135-138). 10. Chernobrovkina, E. B. (2018). Features of taxation in the field of physical culture and sports in the Russian Federation. Bulletin of the O. E. Kutafin Moscow State Law University, 9, 132-140. 11. Mistineva, N. Y. (2016). The tax system as a factor in the development of sports. Priority Directions for the Development of Science and Education, 4-2, 189-192. https://doi.org/10.21661/r-115030 12. Katamadze, A. T., & Ilyushnikova, T. A. (2007). New in the taxation of non-profit organizations. Tax Policy and Practice, 6, 26-33. 13. Sokolov, A. P., & Semenov, D. A. (2022). State tax policy in the field of taxation of non-profit organizations. Industrial Economy, 8(3), 773-777. https://doi.org/10.47576/2712-7559_2022_3_8_773 14. Kozhin, P. S. (2021). Some problems of taxation of profits of non-profit organizations. Taxes and Financial Law, 2, 131-136. 15. Brown, M. T., Rascher, D. A., Nagel, M. S., & McEvoy, C. D. (2021). Financial management in the sport industry. 16. Szymanski, S. (2003). The economic design of sporting contests. American Economic Association Journal of Economic Literature, 41(4), 1137-1187. https://doi.org/10.1257/002205103771800004 17. Forrest, D., & Simmons, R. (2002). The economics of sport. Cambridge University Press. 18. Kleven, H. J., Landais, C., & Saez, E. (2013). Taxation and international migration of superstars: Evidence from the European football market. American Economic Review, 103(5), 1892-1924. 19. Priazhnikova, O. N. (2022). The third sector, social economy, solidarity economy: Approaches to definitions and conceptualization of concepts. Economic and Social Problems of Russia, 3, 15-36. https://doi.org/10.31249/espr/2022.03.01 20. Goncharenko, L. I., Chemeritsky, L. K., Lipatova, I. V., & Smirnova, E. E. (2023). Taxation of non-profit organizations: A textbook. Knorus. 21. Garibov, A.G. (2023). Development of tax incentives for non-profit organizations. Taxes and Taxation, 5, 54-70. https://doi.org/10.7256/2454-065X.2023.5.43992 22. Gushchina, I. E. (2019). Sponsorship: Accounting and taxation. Financial Bulletin: Finance, Taxes, Insurance, Accounting, 10, 42-49. 23. Fedorova, O. S. (2020). Taxation during the participation of commercial organizations in sports events. Taxes and Financial Law, 7, 102-112. 24. Tikhonova, A. V. (2025). Tax factors of labor migration of the population. Finance, 2, 10-17.

First Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

Second Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

Third Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

|