Eng

Eng

Taxes and Taxation

Reference:

Mitin, D.A. (2023). Assessment of the potential indicative excise rate for filter cigarettes in the EAEU. Taxes and Taxation, 3, 47–61. https://doi.org/10.7256/2454-065X.2023.3.40703

|

Library

|

Your profile |

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.|

Taxes and Taxation

Reference:

Mitin, D.A. (2023). Assessment of the potential indicative excise rate for filter cigarettes in the EAEU. Taxes and Taxation, 3, 47–61. https://doi.org/10.7256/2454-065X.2023.3.40703

Assessment of the potential indicative excise rate for filter cigarettes in the EAEU

DOI: 10.7256/2454-065X.2023.3.40703EDN: RHLPTMReceived: 10-05-2023Published: 05-07-2023Abstract: The article evaluates the compliance of the EAEU member states with the provisions of the Agreement on the principles of conducting tax policy in the field of excises on tobacco products in the member states of the Eurasian Economic Union (hereinafter referred to as the EAEU), and also assesses the potential indicative excise rate for filter cigarettes in the EAEU for 2029. The subject of the study is the excise rates for filter cigarettes in the EAEU member states. The purpose of the study is to assess the prospects for the EAEU member states to achieve the level of the indicative rate established by the Agreement on the Principles of Conducting Tax Policy in the Field of Excises on Tobacco Products in the EAEU for 2024 and to develop proposals for the level of the indicative rate for the future period and a general model for its formation. The methodology of the work is based on the general logical and empirical methods of research, which, in the face of limited data, make it possible to calculate the potential excise rate for filter cigarettes in the EAEU member states for 2029. It is shown that the current model of establishing an indicative excise rate for filter cigarettes based on the euro needs to be changed due to the significant volatility of the national currencies of the EAEU member states. Factors that can influence the desire of countries to continue the policy of systematic increase in excise rates on filter cigarettes are also highlighted. The recommendations obtained as a result of the study can be used by the competent authorities of the EAEU member states when setting the indicative excise rate for filter cigarettes for future periods. Keywords: excises, tax policy, EAEU, taxation, indicative rate, tobacco products, harmonization, forecasting, international taxation, indirect taxesThis article is automatically translated. You can find original text of the article here. Introduction:

In the current economic conditions, it seems difficult for a single country to overcome the crisis and move into the stage of sustainable development [1]. Therefore, regional integration associations are of great importance for development. One of the dynamically developing integration associations is the EAEU, which currently unites 5 states: the Republic of Armenia, the Republic of Belarus, the Republic of Kazakhstan, the Kyrgyz Republic and the Russian Federation. The EAEU began its functioning as an international economic organization in 2015. The purpose of the Union is to create conditions for the stable development of the economies of the member States in the interests of improving the living standards of their population. For this: - a single market of goods, services, capital and labor resources is being formed (four freedoms); - comprehensive modernization, cooperation and increasing the competitiveness of national economies in the global economy are being carried out. The unified policy is carried out in the areas agreed by the EAEU member states: customs tariff, non-tariff, technical regulation, etc. The coordinated and coordinated economic policy of the Union requires gradual convergence and harmonization of the legislations of its members in various areas. In particular, a balanced tax policy is necessary for the sustainable development of the integration association. The tax policy of the EEA is aimed at supranational regulation and harmonization of the tax legislation of the member countries of the integration association in terms of taxes directly affecting the markets of goods - VAT and excise taxes, as well as labor – personal income tax. At the same time, the actual tax rates, tax benefits and other parameters important for the country's economy are set by the EAEU member state independently. In some cases, agreements are concluded between Member States aimed at bringing the rates of individual taxes closer together. Currently, tax regulation of excise taxation in the EAEU occurs only in relation to the most sensitive categories of goods: strong alcohol and tobacco. At the same time, a supranational Agreement has been signed only with respect to excise taxes on cigarettes with a filter [2]. In turn, with regard to excise taxes on alcoholic beverages, the draft of the relevant agreement was developed back in 2018 [3], but has not yet been ratified by the Parties. The tax policy in the field of excise taxation of tobacco products on the territory of the EAEU is closely related to the operation of the international agreement "Framework Convention on Tobacco Control of the World Health Organization" [4], adopted in May 2003 and signed by all EAEU member States, in order to reduce mortality due to tobacco use. As you know, one of the most effective ways to regulate the level of consumption of any product is pricing policy. As a result, in order to fulfill obligations under an international act on the territory of the EAEU, there is a tendency to systematically increase excise rates on cigarettes with a filter [5]. Paragraph 1 of Article 3 of the Agreement on the Principles of Conducting Tax Policy in the Field of Excise Taxes on Tobacco Products of the EAEU Member States dated 19.12.2019 (hereinafter referred to as the Agreement) establishes that harmonization (convergence) the rates of excise taxes on tobacco products are carried out by establishing a single indicative rate for tobacco products every 5 years, as well as the permissible ranges of deviation of the actual rates of excise taxes on tobacco products from the indicative rate. In accordance with Article 4 of the Agreement, the indicative excise tax rate for cigarettes with a filter for 2024 is set at 35 euros, as well as the maximum possible ranges of deviation from it of no more than 20% (down or up). In accordance with paragraph 4 of Article 3 of the Agreement, the EAEU member States no later than 2 years before the end of the period of application of the indicative rate within the framework of the work of the advisory body under the Board of the Eurasian Economic Commission (hereinafter referred to as the Commission) on issues of tax policy and administration, proposals are being developed on measures to harmonize (approximate) excise rates on tobacco products for the next period of application of the indicative rate. Based on the above, an analysis of the dynamics of changes in excise rates on tobacco products in the EAEU member states for the period 2019-2023, as well as in the forecast period of 2024, was carried out.

Dynamics of changes in excise rates for cigarettes with a filter in the EAEU member states (based on the average exchange rate of national currencies to the euro by year)

1) For the period 2019-2023, the excise tax rates on filtered cigarettes in the Republic of Armenia increased from 15 euros per 1,000 cigarettes to 34 euros (+19 euros). The average annual growth rate of rates for 5 years (2019-2023) is 15%. While maintaining the current growth rate, and also taking into account the average exchange rate of the dram to the euro for the period under review, the excise tax on cigarettes with a filter in 2024 will amount to 33 euros per 1000 pieces, which corresponds to the level of the indicative excise rate established by the Agreement. 2) The excise tax rate on cigarettes with a filter of the I price group in the Republic of Belarus for the period under review increased from 7 to 33 euros per 1000 pieces (+26 euros). The average annual growth rate over 5 years is 67.3%. While maintaining the current growth rate, and also taking into account the average exchange rate of the Belarusian ruble to the euro for the period under review, the excise tax on cigarettes with a filter in 2024 will be 55 euros per 1000 pieces, which is 31% higher than the upper threshold of the indicative rate established by the Agreement. The excise tax rate on cigarettes with a filter of the II price group (until 2022, the III price group) for the period under review increased from 20 to 50 euros per 1000 cigarettes (+30 euros). The average annual growth rate over 5 years is 34.5%. While maintaining the current growth rate, and also taking into account the average exchange rate of the Belarusian ruble to the euro for the period under review, the excise tax on cigarettes with a filter for the II price group will be 68 euros per 1000 pieces, which is 61% higher than the indicative rate set by the Agreement. 3) During the period under review, the excise tax rates on cigarettes with a filter in the Republic of Kazakhstan increased from 20 to 33 euros per 1000 pieces (+ 13 euros). The average annual growth rate over 5 years is 12.8%. While maintaining the current growth rate, and also taking into account the average exchange rate of tenge to euro for the period under review, the amount of excise tax on cigarettes in 2024 will be 15,900 tenge or 34 euros per 1,000 units (according to the average exchange rate of tenge to euro for the period under review), which corresponds to the level of the indicative rate established by the Agreement. 4) In the Kyrgyz Republic, during the period under review, the excise tax rate on cigarettes with a filter increased from 19 to 28 euros per 1,000 pieces (+ 9 euros). The average annual growth rate for 5 years is 10.9% per year. While maintaining the current rate of increase in excise taxes, as well as the average level of the som rate to the euro, the excise rate for cigarettes with a filter in 2024 will be 28 euros per 1000 pieces, which corresponds to the lower threshold of the indicative rate level established by the Agreement. 5) In the Russian Federation, the excise tax rate on cigarettes with a filter for the period under review increased from 35 to 45 euros per 1000 pieces (+10 euros). The average annual growth rate over 5 years is 8%. While maintaining the current growth rate, and also taking into account the average exchange rate of the ruble to the euro for the period under review, the excise tax on cigarettes with a filter in 2024 will amount to 46 euros per 1000 pieces, which is 10% higher than the limit level of the indicative rate established by the Agreement. The detailed dynamics of the convergence of excise rates on cigarettes with a filter in the EAEU member states is reflected in Table No. 1. It should be noted that when forecasting the excise tax rate on cigarettes with a filter in the Republic of Belarus for 2024, the average growth rate of the corresponding rate in the Russian Federation was used, since during the period 2022-2023 in the Republic of Belarus there was a significant increase in the rate, which may be a consequence of their rapprochement with the Russian Federation in connection with the creation of the Union State. The continuation of such growth in subsequent periods seems unlikely.

Table 1 – Dynamics of growth of excise tax rates on tobacco products in the EAEU member states for 2019-2023 and forecast for 2024 (per 1000 pieces)

When translating the actual excise tax rates on cigarettes with a filter in the EAEU member states, the average exchange rate of national currencies to the euro for the year was applied, in accordance with the data of national banks.

Table 2 – The average exchange rate of the EAEU member states to the euro for the period 2019-2023 [6].

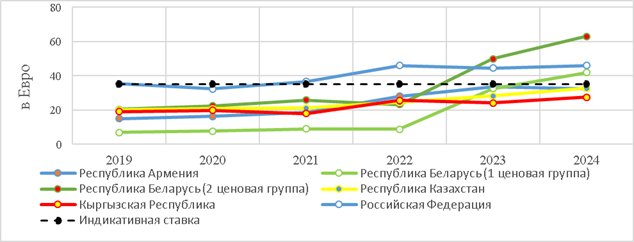

Visualization of the dynamics of changes in excise rates for cigarettes with a filter in the EAEU member states for the period under review is shown in Figure 1.

Figure No. 1. Schedule of convergence of excise tax rates on cigarettes with a filter in the EAEU member states for the period 2019-2023.

According to the results of the analysis of the dynamics of convergence of excise rates on cigarettes with a filter in the EAEU member states for the period 2019-2023, as well as in the forecast period of 2024, the following has been established. 1) The EAEU member States have systematically increased the rates of these excise taxes. The growth rates of excise taxes on cigarettes with a filter in the EAEU member states ranged from 8% to 67%. The average increase in the rates of these excise taxes in the EAEU was 25%. 2) Due to fluctuations in the exchange rates of the national currencies of the EAEU member states, a number of cases have been established when, with an actual increase in the excise tax rate on cigarettes with a filter in national currencies, when converting this rate into euros, negative dynamics was observed relative to last year's level (for example, in the Republic of Belarus (II price category), the Kyrgyz Republic, the Russian Federation). This fact is an indicator indicating the expediency of revising the current model of setting the indicative excise rate. 3) As of 2023, the average excise tax rate on cigarettes with a filter in the EAEU member states is 36 euros. 4) When forecasting excise tax rates for cigarettes with a filter in the EAEU member states for 2024, it was established that while maintaining the current dynamics of the rate growth rate, as well as the inflation rate, all Parties will reach in the reporting period the level of the indicative rate set by the Agreement at 35 euros and acceptable ranges of deviation from it (-20% or 28 euros; + 20% or 42 euros).

Forecast of changes in excise rates for cigarettes with a filter in the EAEU member states for the period 2024-2029.

In accordance with paragraph 4 of Article 3 of the Agreement, the EAEU member states in 2023 should determine the indicative excise tax rate for cigarettes with a filter and the ranges of deviations from it for 2029. In this connection, an assessment of the potential indicative rate of excise taxes on cigarettes with a filter was carried out. It is established that while maintaining the current rates of economic growth, the inflation rate, as well as the current dynamics of the growth rate of excise taxes on cigarettes with a filter, the excise rates in the EAEU member states in 2029 will be:

Table 3 – Forecast of the dynamics of excise rates on cigarettes with a filter in the EAEU member states for 2029.

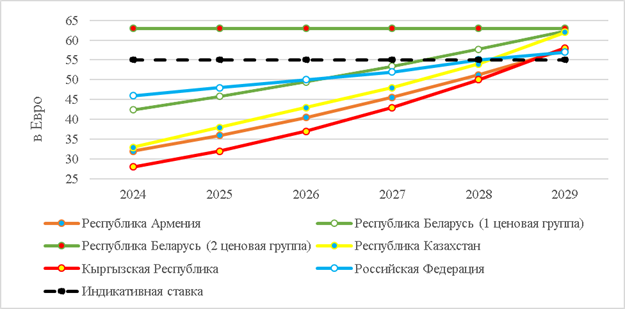

Based on the results obtained, the average level of excise tax rates for cigarettes with a filter in the EAEU member states will be 63 euros. Thus, it is advisable to consider establishing an indicative excise tax rate for cigarettes with a filter at the level of 55 euros or 60 euros. For comparison, in the European Union, the level of excise tax rates on tobacco products is 90 euros per 1,000 cigarettes, while it is going to be increased [7]. In addition, the current permissible level of deviations of the actual excise rates for cigarettes with a filter from the indicative rate seems significant, especially given the potential increase in the indicative rate. In this connection, it is advisable to consider reducing it, especially the possible range of deviation in a smaller direction. It is proposed to set the appropriate range of deviations at the level of 5% down and 15% up. When setting the indicative excise tax rate for cigarettes with a filter at the level of 55 euros and the proposed permissible range of deviation rates from it, the EAEU member states should: a) The Republic of Armenia to reduce the current average annual growth rates of excise taxes on cigarettes with a filter by at least 1% (up to 14% per annum), but not more than 4% (up to 11% per annum). The average growth rate of excise rates for the period 2024-2029 may be 12.5%. b) The Republic of Belarus should maintain the current level of the excise tax rate on cigarettes with a filter of the II price group. c) The Kyrgyz Republic should increase the average growth rate of excise tax rates on cigarettes with a filter by at least 3% (up to 14% per annum), but not more than 7% (up to 18% per annum). The average growth rate of excise rates for the period 2024-2029 may be 16%. d) The Russian Federation should reduce the average annual growth rate of the excise tax rate on cigarettes with a filter by at least 2% (up to 6% per annum), but not more than 5% (up to 3% per annum). On average, the increase in the corresponding excise rates may amount to 4.5%. e) Other EAEU member states should not change the current growth rates of excise taxes on cigarettes with a filter. The projected dynamics of the increase in excise rates for cigarettes with a filter, taking into account the proposed adjustments and an indicative rate of 55 euros, is shown in Figure No. 2.

Figure No. 2. Predicted dynamics of excise tax rates for cigarettes with a filter in the EAEU member states at the indicative rate of 55 euros

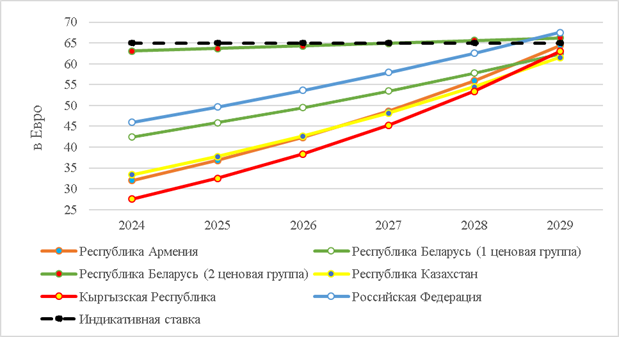

In turn, if the indicative excise tax rate for cigarettes with a filter is set at 60 euros and the proposed possible ranges of deviation from it, the EAEU member states should make the following adjustments to the current average rate increase: a) The Republic of Belarus should reduce the current average increase in the excise tax rate on cigarettes with a filter of the II price group to no more than 1% per annum or maintain the current rate. b) The Kyrgyz Republic should increase the average growth rate of excise tax rates on cigarettes with a filter to at least 16% per year, but not more than 20% per year. The average growth rate of excise rates for the period 2024-2029 may be 18%. c) Other EAEU member states should not change the current rate of increase in excise rates on cigarettes with a filter. The projected dynamics of the increase in excise rates for cigarettes with a filter, taking into account the proposed adjustments to the indicative rate set at 60 euros, is shown in Figure No. 3.

Figure No. 3. Predicted dynamics of excise tax rates for cigarettes with a filter in the EAEU member states at the level of the indicative rate of 60 euros

Discussion issues and proposals for further tax policy in the field of excise taxes on cigarettes with a filter in the EAEU.

It is important to note that the approach used to forecast the dynamics of increasing excise rates on cigarettes with a filter for the planning period 2025-2029 primarily takes into account only economic indicators, but does not take into account circumstances that can have a significant impact on the decision of countries to raise the level of excise rates. As noted earlier, the basis of the tax policy in the field of excise taxes on cigarettes with a filter in the EAEU is the "Framework Convention of the World Health Organization on Tobacco Control". At the same time, a number of scientists note that the regular increase in excise rates on cigarettes with a filter does not significantly affect the reduction in tobacco consumption [8]. Researchers also note a direct relationship between the excise tax rate and the level of illegal turnover of tobacco products [9]. The decrease in the level of tobacco consumption in the EAEU against the background of the actual expansion of the volume of illegal tobacco products was also recorded by specialists of the KPMG consulting firm as part of a study conducted for the Rusbrand Association [10]. In turn, we note that illegal tobacco products are usually bought by people who use this product for a long period of time. At the same time, the increase in prices for tobacco products makes this product less accessible to young segments of the population (teenagers, students), which may affect their decision to purchase it, which will reduce tobacco consumption in the future. Of course, the goal of reducing tobacco consumption cannot be achieved solely by economic measures, an integrated approach is needed in this matter. The actual decision to change excise rates is also significantly influenced by the level of inflation in the country [11]. In turn, this indicator is different in the EAEU member states [12] and changes regularly, which also reduces the prospects for a significant change in the level of the indicative rate. In addition, in the current difficult geopolitical conditions, as well as taking into account the actual economic crisis, an increase in excise rates may cause a wave of social discontent [13], since the actual burden of paying the tax is placed on the end consumer. The level of the indicative rate for 2029 may also be affected by trade policy issues. As you know, the payers of excise taxes are manufacturers, as well as importers of excisable products. According to the analytical report of the Eurasian Economic Commission, Kazakhstan, Armenia and Kyrgyzstan are engaged in tobacco cultivation [14]. At the same time, the main factories for the production of cigarettes with a filter are located on the territory of the Russian Federation. In turn, local cigarette manufacturers from the EAEU member states are practically not represented on the Russian market. As a result, the actual benefit from the increase in excise rates on cigarettes with a filter is received by the Russian Federation. Thus, the decision to establish the future indicative rate of excise taxes on cigarettes with a filter in the EAEU cannot be based solely on economic indicators. In this matter, it is necessary to take into account other aspects that may become the subject of further research. At the same time, regardless of the actual decision on the level of the indicative rate, in order to bring the tax legislation of the EAEU member states closer, the Republic of Belarus is recommended to consider combining excise tax rates on cigarettes with a filter for the first and second price groups by 2029. Considering that earlier a similar association occurred between the third and second price groups of cigarettes with a filter. Also, when planning the indicative excise tax rate for the next period, it is advisable for the EAEU member states to consider changing the benchmark of the indicative rate in the form of euros, due to significant fluctuations in the exchange rates of national currencies. In the form of a new benchmark of the indicative rate can be: - one of the currencies of the EAEU member states; - the currency of the strategic partner – China (Yuan) [15]; - the percentage ratio of the current level of the excise rate and the planned; - the level of purchasing power (the number of packs of cigarettes that an average citizen can buy). If the EAEU member states are not ready to increase excise rates on cigarettes with a filter in the current conditions, it is advisable to consider only changing the possible ranges of deviation of actual excise rates from the level of the indicative rate to a lesser extent. This will contribute to the creation of equal conditions for doing business and interaction between the EAEU countries within the same customs territory [16].

Conclusion

The analysis of changes in excise rates for cigarettes with a filter in the EAEU member states showed that all countries are expected to reach the level of the indicative rate set for 2024. As part of the forecast of excise tax rates for cigarettes with a filter in the EAEU member states for the period 2024-2029, it was proposed to consider setting the indicative excise tax rate at the level of 55 or 60 euros. Also, in order to bring excise rates closer in the EAEU member states, it is proposed to consider reducing the current possible ranges of deviation of actual excise rates from the level of the indicative rate. At the same time, due to fluctuations in the exchange rates of the national currencies of the EAEU member states, a number of cases have been established when, with an actual increase in the excise tax rate on cigarettes with a filter in national currencies, when converting the specified rate into euros, negative dynamics was observed relative to last year's level (for example, in the Republic of Belarus (II price category), the Kyrgyz Republic, Russian Federation). Considering this fact, when planning the level of the indicative excise tax rate for cigarettes with a filter in the EAEU for 2029, it is proposed to consider abandoning the current model of setting the level of the indicative rate in euros, for which alternative approaches are proposed. At the same time, a number of non–economic factors were noted that could influence the actual decision of the EAEU member states to change the level of the indicative excise tax rate on cigarettes with a filter. References

1. Tax risks of the state in modern economic conditions. Advocate A.S., Andreeva A.N., Vishnevskaya N.G., Goncharenko L.I., Zaponkina A.A., Kostin A.A., Krasnobaeva A.M., Malkova Yu.V., Novoselov K .V., Polezharova L.V., Tikhonova A.V., Tyurikov A.G., Moscow, 2022.

2. Agreement on the principles of tax policy in the field of excises on tobacco products of the Member States of the Eurasian Economic Union. – Text : electronic. – URL: https://docs.eaeunion.org/docs/ru-ru/01424400/itia_23122019; 3. Draft Agreement on the principles of conducting tax policy in the field of excises on alcoholic products in the member states of the Eurasian Economic Union. – Text : electronic. – URL: https://docs.eaeunion.org/pd/ru-ru/012619/; 4. WHO Framework Convention on Tobacco Control. – Text : electronic. – URL: https://www.un.org/ru/documents/decl_conv/conventions/pdf/tobacco.pdf; 5. Tikhonova A.V. — On the issue of changing the functional role of excises in Russia // Taxes and taxation.-2019.-No. 11.-P. 35-44. DOI: 10.7256/2454-065X.2019.11.31440 URL: https://nbpublish.com/library_read_article.php?id=31440; 6. Exchange rates of the Central Bank. https://www.banki.ru/products/currency; 7. Financial Times. Brussels to propose rise in cigarette taxes and first EU-wide vaping levy. – Text : electronic. – URL: https://www.ft.com/content/6f1c4211-5e54-4aa8-a391-0ec9bc5244de; 8. N. S. Migda, I. E. Nekrasova, S. I. Degtyarev, M. B. Semenyuk, Main problems of excise taxation and directions for improving excise taxes, Notes of a scientist.-2021.-No. 6-1.-S. 402-405. – EDN ODGHZN; 9. Salomatin V.A., Romanova N.K., Shuraeva G.P. Tax policy in the field of excises on tobacco products in Russia // MNIZH. 2018. No. 3 (69). URL: https://cyberleninka.ru/article/n/nalogovaya-politika-v-oblasti-aktsizov-na-tabachnuyu-produktsiyu-v-rossii (date of access: 05/10/2023); 10. Consumption of illegal cigarettes has increased in the EAEU countries. – Text : electronic. – URL: https://rg.ru/2022/05/31/v-stranah-eaes-vyroslo-potreblenie-nelegalnyh-sigaret.html 11. Taxation of the CIS countries / Fomin E.P., Zubkova A.A., Nazarov M.A., Mikhaleva O.L., Lukyanenko L.F., Bityukova T.A., Charikov V.S., Lukyanenkov M. .V., Nesterova O.V., Mustakimov I.R., Chernousova K.S., Dremova E.Yu. // Samara State University of Economics. – Samara, 2013. 12. Monitoring the inflation rate in the EAEU member states. – Text : electronic. – URL: https://eec.eaeunion.org/upload/medialibrary/f35/inflation_3Q2022.pdf 13. Eremeeva, Yu. A. Fundamentals of building excise taxes on certain types of goods / Yu. A. Eremeeva, K. S. Chernousova // International Journal of Humanities and Natural Sciences.-2021.-No. 1-2 (52).-S. 101-104. – DOI 10.24411/2500-1000-2021-1092. – EDN MGBBSS. 14. Reference and analytical materials on the development of cooperation between the Member States of the Eurasian Economic Union in the tobacco industry. – Text : electronic. – URL: https://eec.eaeunion.org/upload/medialibrary/84a/Tabak.pdf; 15. Yuan. Alternative to dollar and euro. – Text : electronic. – URL: https://dokhodchivo.ru/yuan 16. Turban, G. V. Excises as a tool for regulating foreign trade in the EAEU / G. V. Turban // Strategy for the development of the economy of Belarus: challenges, tools for implementation and prospects: collection of scientific articles of the International Scientific and Practical Conference: in 2 volumes, Minsk, 07–08 October 2021. Volume 2.-Minsk: IOOO "Rights and Economics", 2021.-P. 138-143. – EDN HHBSFD

First Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

Second Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||