|

Taxes and Taxation

Reference:

Popova, E.M., Guseinova, G.M., Goncharova, A.V. (2022). Assessment of regional measures of tax support for business in the context of the COVID-19 pandemic. Taxes and Taxation, 4, 57–76. https://doi.org/10.7256/2454-065X.2022.4.38563

Assessment of regional measures of tax support for business in the context of the COVID-19 pandemic

Popova Evgeniya Mikhailovna

Senior Educator, the department of World Economy, Entrepreneurship and Humanities, Chita Institute (Branch) of Baikal State University

672000, Russia, Zabaikal'skii krai, g. Chita, ul. Anokhina, 56

|

p_e_m_2013@mail.ru

|

|

|

Other publications by this author

|

|

Guseinova Guzel Mukhtarovna

PhD in Economics

Associate professor, Department of Finances, Saint Petersburg State University of Economics

191023, Russia, g. Saint Petersburg, ul. Sadovaya, 21

|

|

guseynova.g@unecon.ru

|

|

|

Other publications by this author

|

|

|

Goncharova Aleksandra Vladimirovna

Student, Department of World Economy, Entrepreneurship and Humanities, Chita Institute of Baikal State University

672000, Russia, Zabaikalsky Krai, Chita, Anokhina str., 56

|

|

gonsasha2010@mail.ru

|

|

|

|

DOI: 10.7256/2454-065X.2022.4.38563

EDN: VXVAXD

Received:

04-08-2022

Published:

03-09-2022

Abstract:

The implementation of quarantine measures and the decline in economic activity in 2020 became an impetus for the implementation of a stimulating tax policy not only at the federal, but also at the subnational level. The article examines the experience of countercyclical fiscal policy in the OECD countries, highlights the factors of relatively modest tax support provided to small and medium-sized businesses at the subnational level. The object of the study is stimulating tax expenditures provided in accordance with the legislation of the Russian regions to support economic entities in the conditions of restrictive measures caused by the spread of a new coronavirus infection. The research methodology is based on the methods of formal logic, statistical and econometric analysis. The scientific novelty of this study consists in conducting a comprehensive analysis covering all subjects of the Russian Federation in which stimulating tax expenditures were actually provided, and assessing the regional tax policy implemented during the COVID-19 pandemic through the prism of key budget parameters and indicators of socio-economic development. The regional tax policy was carried out in conditions of large-scale fiscal support from the federal center and deterioration of the state of subnational finances due to the growth of deficit budgets. During the 2020 pandemic, the constituent entities of the Russian Federation provided tax benefits on taxes that account for a small share in the revenues of regional budgets. Since the main purpose of tax incentives was to solve liquidity problems and maintain employment, investment tax incentives for corporate income tax were not introduced in Russian regions. The study of the actual and forecast dynamics of GRP allowed us to conclude that the tax support measures implemented in the Russian subjects stimulated economic activity and helped to smooth out the negative consequences of the coronacrisis.

Keywords:

tax expenditures, tax benefits, subnational budgets, regions, small business, gross regional product, property taxes, simplified taxation system, inter-budget transfers, coronacrisis

This article is automatically translated.

You can find original text of the article here.

Introduction. The COVID-19 pandemic has caused the need to implement an unprecedented set of state support measures aimed at smoothing the negative consequences of the coronacrisis. Tax expenditures were one of the instruments of state discretionary policy aimed at slowing the decline in GDP. In the domestic scientific literature, many publications are devoted to the application of tax incentives during the period of active introduction of coronavirus restrictions. Shukaeva A.V. gives a brief overview of the main tax breaks and benefits provided by federal legislation to support small and medium-sized businesses, emphasizing their timeliness and targeted nature [1, p. 217]. Kuznetsova N.R., having identified the key forms of tax benefits that were introduced at the level of the subjects of the Russian Federation, concludes about the weak support of enterprises provided by the regional government [2, p. 128]. The article prepared by Ryazantseva N.V., Pashchenko F.S., Borel A.E. also lists the main types of tax benefits provided by regional legislation, but does not specify the amounts of budget losses and target categories of taxpayers [3, p. 98]. In some scientific articles, tax measures to support small and medium–sized businesses are considered in more detail on the example of specific regions: Perm Krai (authors – Zakharkina A.V., Kuznetsova O.A.), Arkhangelsk Region (authors - Frolov A.I., Synkov V.V.) [4, p. 109; 5, p. 72]. However, the analysis of scientific publications made it possible to conclude that the content of the articles is mainly reduced to a review of tax expenditures used to stimulate economic agents, while no critical analysis of the measures being implemented is given and recommendations for improving existing practices are not offered. The same conclusions are reached by E.S. Vylkova, who, after studying scientific papers published on this topic in leading economic journals, summarizes that most of them are of a ascertaining nature without increment of scientific knowledge [6, p. 89]. The author defines the prospects for further research, which consist in the transition from generalization of tax measures to combat the pandemic to the development of scientifically sound proposals for their reform. As for regional measures of tax support for business during the introduction of the most extensive coronavirus restrictions in 2020, the lack of comprehensive studies that would cover all subjects of the Russian Federation and provide in-depth analysis, taking into account the relationship with the main parameters of the budget and indicators of socio-economic development, is a clear gap. In this connection, the object of the study of this article is stimulating tax expenditures provided by regional legislation to support economic entities in the conditions of restrictive measures caused by the spread of a new coronavirus infection. The purpose of the study is to assess the measures of tax support implemented in the Russian regions during the pandemic through the prism of key budget parameters and indicators of socio-economic development. To achieve the above stated goal , it is necessary to solve a number of tasks: – to consider the foreign experience of countercyclical fiscal policy at the federal and subnational levels; – to determine the volume and structure of stimulating tax expenditures provided by the legislation of the subjects of the Russian Federation in the conditions of deterioration of the economic situation as a result of the spread of coronavirus infection; – to study the conditions of the preferential regime for each tax for which tax expenses were provided; – to determine such important budget parameters as the growth rates of revenues and expenditures that were observed in the crisis year 2020 in relation to 2019, the volume, proportion and growth rates of inter-budget transfers from the federal budget and tax revenues; – determine for each region the deviation of the actual value of the GRP growth rate in 2020 from the forecast value. Methodological basis of the research: methods of formal logic, methods of system, statistical and econometric analysis. The empirical basis of the study: reports of international economic organizations (the International Monetary Fund, the Organization for Economic Cooperation and Development), publications prepared by Rosstat and executive authorities of the subjects of the Russian Federation. Countercyclical fiscal policy pursued at the federal and subnational levels: foreign experience. The total amount of financial support provided in different countries of the world in 2020 is estimated at $13.8 trillion, or 13% of world GDP (developed countries account for $11.8 trillion) [7]. In addition, the report of the International Monetary Fund indicates that $7.8 trillion are transfers and shortfall in budget revenues due to a decrease in effective tax rates and the effect of tax deferrals.The International Monetary Fund has published data on the amount of tax expenditures incurred by the budgets of a number of countries in 2020 [7]. Tax expenditures were provided to business entities and households in order to maintain employment, stimulate consumer and investment spending. To ensure comparability of data and obtain more reliable research results, the authors of this article additionally calculated two indicators: the share of tax expenditures in the country's GDP and the error in forecasting the growth rate of real GDP in 2020 compared to the previous year as a deviation of the actual value from the forecast (see Table 1). Table 1 – Data for assessing the impact of tax expenditures on the error in forecasting the growth rate of real GDP |

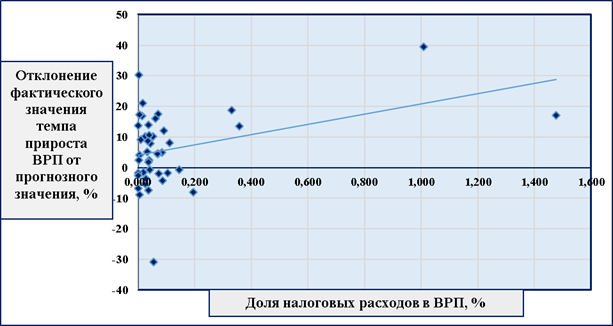

A country | Share of tax expenditures in GDP, % | Real GDP growth rate 2020/2019 (forecast data), % | Real GDP growth rate 2020/2019 (actual data), % | Deviation of the actual value from the forecast value, % | | USA | 2,57 | -5,9 | -3,4 | 2,5 | | China | 1,14 | 1,2 | 2,3 | 1,1 | | Germany | 0,83 | -7 | -4,6 | 2,4 |

| Sweden | 0,63 | -6,8 | -2,9 | 3,9 | | Indonesia | 0,62 | 0,5 | -2,1 | -2,6 | | Poland | 0,59 | -4,6 | -2,5 | 2,1 | | Spain | 0,5 | -8 | -10,8 |

-2,8 | | Finland | 0,42 | -6 | -2,8 | 3,2 | | Australia | 0,32 | -6,7 | -0,004 | 6,696 | | Russia | 0,28 | -5,5 | -3 | 2,5 | | Brazil | 0,19 | -5,3 |

-4,1 | 1,2 | | South Korea | 0,17 | -1,2 | -0,9 | 0,3 | | Argentina | 0,16 | -5,7 | -9,9 | -4,2 | | France | 0,14 | -7,2 | -8 | -0,8 | | Italy | 0,11 |

-9,1 | -8,9 | 0,2 | Source: compiled by the authors based on [7],[8],[9]. The calculations carried out showed that in most countries the actual decline in GDP was less than the forecast level. To provide clarity, a dot diagram was constructed and a trend line was drawn, which demonstrates a direct relationship between the two variables (see Figure 1).

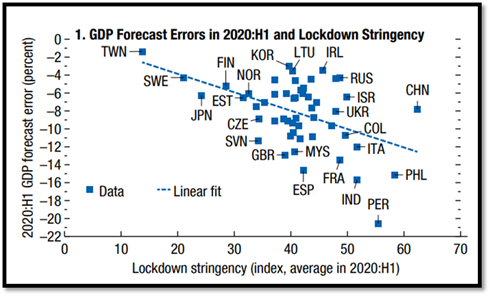

Fig. 1. Assessment of the impact of tax expenditures on the error in forecasting the growth rate of real GDP Source: compiled by the authors. At the same time, the inelasticity of the trend line and the calculated correlation coefficient (0.2) indicate a weak connection, namely, an increase in tax expenditures is not always accompanied by a more significant reduction in the negative growth rates of real GDP. Although tax expenditures stimulated economic activity, nevertheless, there are a number of more significant factors that explain the significant gap in forecast errors with the same amount of tax support: the sectoral structure and the degree of export orientation of the national economy. In addition, the severity of the self-isolation regime should be highlighted as an important factor that influenced the magnitude of the forecast error. Experts of the International Monetary Fund, using an impressive database, conducted a correlation analysis aimed at clarifying the relationship between the degree of severity of the self-isolation regime and the level of economic activity. In Figure 2, you can see a trend line that demonstrates a direct relationship between the index characterizing the severity of the self-isolation regime (the abscissa axis) and the magnitude of the error in the GDP forecast (the percentage deviation of the actual GDP value for the first half of 2020 from its forecast value calculated in January 2020) [8].

Fig. 2. Assessment of the impact of restrictive measures on the decline in GDP Source: compiled by the authors. The study concluded that the countries that introduced stricter restrictive measures experienced a more serious drop in GDP compared to the forecast estimates made before the pandemic. The most stringent self-isolation regime was introduced in developed countries, which have the most significant decline in GDP, equal to 4.9%. In the group of developing countries and emerging markets, where restrictive measures were not so long and large-scale, GDP decreased by 2.4% [7]. In the OECD countries, economic entities that belong to small and medium-sized enterprises account for about 99% of the total number of registered enterprises and create 50-60% of gross value added. In this connection, the priority of supporting small and medium-sized businesses was announced not only at the federal, but also at the subnational level. In June-July 2020, the Committee of the Regions of the European Union and the Organization for Economic Cooperation and Development initiated a survey in which more than 300 regions and municipalities of the EU member states participated [10]. As the results of the survey showed, at the time of its conduct, only 1/3 of respondents stated that they were actively implementing measures aimed at restoring and stimulating the economy. While the majority of representatives of regional and local authorities were focused on solving health problems that arose due to a significant increase in morbidity and mortality from a new coronavirus infection. In OECD countries, on average, 33-40% of expenditures carried out in the health sector are financed from subnational budgets [11]. Thus, by mid-2020, a small part of subnational governments have reached the stage of implementing stimulating economic policies. Only 26% of subnational governments identified the degree of support for economic agents through the provision of tax benefits as "significant", 35% – as "limited". The restrained attitude of the regional authorities towards the expansion of the package of tax incentives was probably dictated by pessimistic forecasts regarding the impact of the pandemic on public finances. According to the survey results, about 83% of respondents expected a significant reduction in the tax revenues of subnational budgets. A common feature of the financial systems of the OECD countries is the inflexibility of subnational budgets. Subnational governments, in the event of a reduction in the revenue side of the budget, cannot easily compensate for the shortfall in revenues by issuing bonds due to existing institutional constraints, as well as a less developed and liquid market for subnational securities compared to the federal bond market. This circumstance, combined with the high uncertainty of the external environment, can also be regarded as a factor contributing to the formation of a wait-and-see attitude towards the introduction of additional tax benefits.

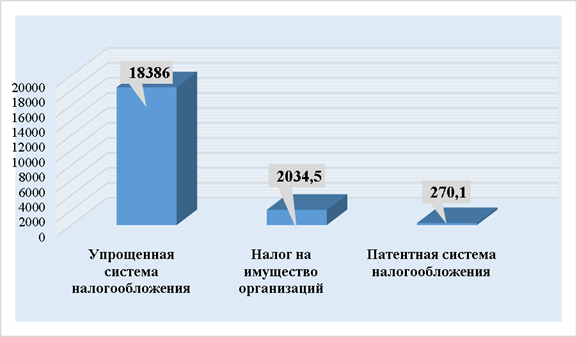

The results of 2020 showed that the COVID-19 pandemic did not have such a serious impact on the financial situation of subnational governments as expected. Although subnational budgets have a less diversified tax revenue structure, studies covering OECD countries show that taxes that form the revenue side of subnational budgets demonstrate lower sensitivity to changes in GDP. If GDP grows by 1%, then property tax revenues will increase by only 0.7%. Property taxes are the main source of income and on average account for 39% of all tax revenues of subnational budgets. Of these incomes, 83% are taxes that are levied on the owners of real estate [12]. Since, unlike the global financial and economic crisis of 2008, the coronacrisis of 2020 was not accompanied by a collapse in real estate prices and even, on the contrary, market prices increased, in fact, the tax revenues of many subnational governments increased. The fact that the pessimistic forecasts regarding the main parameters of subnational budgets have not been fully justified can be explained not only by the fact that the own revenues of subnational budgets are characterized by greater stability during crises, but also by the large-scale financial assistance provided by the central government. In the article, Doherty S. and Biase P. conclude that national governments absorbed the "fiscal shock" by providing impressive inter-budget transfers, most of which were allocated without special conditions (14 out of 23 OECD countries) [13]. The authors emphasize that the timely financial support of the center helped to prevent a significant reduction in investment costs, which was observed during the financial and economic crisis of 2008. Practice shows that 2/3 of public investments made in OECD countries are financed from subnational budgets [13]. In this connection, the fiscal policy pursued at the subnational level can have a significant impact on the growth rate of the national economy as a whole. Being under the influence of the "scissors" effect (a reduction in income while spending increases) during economic crises, subnational governments, first of all, cut discretionary spending, which includes investments, and thereby implement a pro-cyclical policy. Returning to the factors that can serve as an explanation of why in most of the analyzed countries the actual decline in GDP turned out to be less than the forecast level, it is necessary to highlight inter-budget transfers, largely due to which it was possible to prevent a significant drop in investment expenditures financed from subnational budgets as an important component of GDP (see Table 1). Summing up, it is necessary to draw two important conclusions. Firstly, the main "financial blow" was taken by national governments, on the one hand, allocating transfers unprecedented in volume to subnational budgets, on the other hand, providing additional tax benefits to households and firms due to the deterioration of the economic situation. Secondly, the tax support that was provided to small and medium-sized businesses at the subnational level during the introduction of the most extensive coronavirus restrictions should be recognized as modest, which is largely due to the following factors: high uncertainty of the external environment, pessimistic forecasts, an increase in expenditure obligations of subnational authorities and falling revenues of subnational budgets due to new "coronavirus" tax benefits that were introduced by national legislation [14]. Tax expenditures as a tool to stimulate economic activity: the experience of Russian regions. Based on the analysis of the lists of tax expenditures provided in accordance with regional legislation, the subjects of the Russian Federation were identified in which tax incentives were introduced in 2020 to support enterprises under restrictive measures caused by the spread of a new coronavirus infection. Stimulating tax expenditures were provided in 43 regions, which is 51% of all subjects of the Russian Federation (in fact, regional budgets had falling incomes, according to data posted on the official website of the Ministry of Finance of the Russian Federation) [15]. In the vast majority of Russian regions, the validity period of tax benefits was limited to 2020. In the previous section of this article, it was indicated that by mid-2020, less than 30% of the subnational governments of the OECD countries had adopted special legal acts that established tax incentives to stimulate economic activity. Having studied the lists of tax expenditures compiled by the subjects of the Russian Federation, we came to the conclusion that, on the contrary, the majority of stimulating tax expenditures were introduced by the Russian regions in the first half of 2020: 26% in the first quarter, 68% in the second quarter. In addition, the analysis showed that tax expenditures aimed at supporting enterprises during the period of coronavirus restrictions were provided for the tax levied in connection with the application of the simplified taxation system, patent taxation system and corporate property tax. Accordingly, none of the subjects of the Russian Federation introduced tax benefits for corporate income tax. Inclusion in the Unified Register of Small and Medium-sized Businesses was a general requirement for the realization of the right to receive a tax benefit, regardless of the type of tax. The volume of regional tax expenditures provided to enterprises in the context of the deteriorating economic situation as a result of the spread of coronavirus infection amounted to 20.7 billion rubles, which is comparable to the revenues of the budget of the Altai Republic for 2019. In the total volume of stimulating tax expenditures, 88.9% is accounted for by the tax levied in connection with the application of the simplified taxation system, 1.3% – by the patent taxation system, 9.8% – by the corporate property tax. The structure of tax expenditures is shown in Figure 3.

Fig. 3. The volume of tax expenditures provided by the subjects of the Russian Federation in 2020, million rubles. Source: compiled by the authors. Further, for each tax, we will consider such basic parameters of the preferential regime as the target category of taxpayers, the form of tax expenditures (exemption from taxation, reduced rate, deduction), the amount of reduction in the tax burden, the conditions for granting tax expenditures.

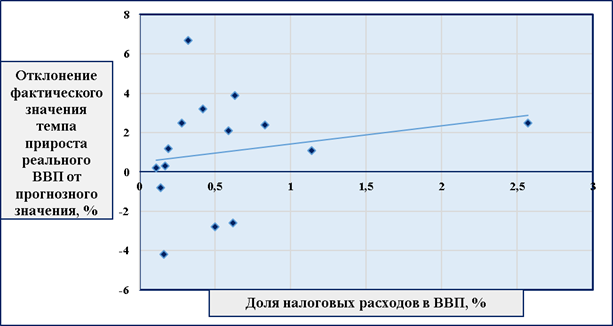

In conclusion, we will analyze regional tax expenditures, taking into account the relationship with the main indicator of socio-economic development of the region – the gross regional product (GRP). As in the first section of this article, in order to ensure comparability of data, we will calculate the share of tax expenditures provided in 2020 in the GRP of each entity and the error in the forecast of the GRP growth rate in 2020 compared to the previous year as a deviation of the actual value from the forecast. In most regions, the share of tax expenditures in GRP was less than 0.2%. In 28 subjects of the Russian Federation, the actual drop in GRP was less than the forecast level (the actual GRP growth was greater than the forecast value). Accordingly, in 15 regions, the actual situation with the dynamics of GRP turned out to be worse than predicted [19]. To ensure clarity, a dot diagram was constructed and a trend line was drawn (see Figure 5).

Fig. 5. Assessment of the impact of regional tax expenditures on the error in forecasting the GRP growth rate Source: compiled by the authors. The positive slope of the trend line and the calculated correlation coefficient (0.38) indicate that there is a direct relationship between the two variables: an increase in the volume of tax expenditures is accompanied by an improvement in the forecast values of GRP. Thus, there are grounds to assert that the tax support measures implemented in the Russian regions during the 2020 pandemic stimulated economic activity and helped to smooth out the negative consequences of the coronacrisis.

References

1. Shukaeva, A. V. (2020). On measures of state support for small and medium-sized businesses during a pandemic. Economics and Business: Theory and Practice, 12, 216-218.

2. Kuznetsova, N. R. (2021). Regional aspect of budgetary policy under the corona crisis. International Research Journal, 4, 127-129.

3. Ryazantseva, N. V., Pashchenko, F. S., & Borel, A. E. (2020). Regional initiatives to ensure socio-economic stability in the context of the COVID-19 pandemic: support measures for business and employment. HSE Analytical Bulletin on the Economic and Social Consequences of Coronavirus in Russia and in the World, 2, 90-103.

4. Zakharkina, A. V., & Kuznetsova, O. A. (2021). Analysis of the Perm regional regulatory platform of tools for small and medium-sized businesses support under a pandemic of a new coronavirus infection (COVID-19). Ex jure, 1, 100-113.

5. Synkov, V. V. (2021). Support measures for business in the context of the COVID-19 pandemic in the Arkhangelsk region. Ural Journal of Legal Research, 2, 68-76.

6. Vylkova, E. S. (2021). Tax policy under the COVID-19 pandemic: a review of publications in leading economic journals. Management Consulting, 12, 81-94.

7. Fiscal Monitor Update, January 2021. International Monetary Fund [Electronic resource]. Retrieved from https://www.imf.org/en/Publica-tions/FM/Issues/2021/01/20/fiscal-monitor-update-january-2021

8. World Economic Outlook, October 2020: A Long and Difficult Ascent. International Monetary Fund [Electronic resource]. Retrieved from https://www.imf.org/en/Publications/WEO/Issues/2020/09/30/world-economic-outlook-october-2020

9. World Economic Outlook, April 2020: The Great Lockdown. International Monetary Fund [Electronic resource]. Retrieved from https://www.imf.org/en/Publications/WEO/Issues/2020/04/14/weo-april-2020#Growth%20Projections%20Table

10. The impact of the COVID-19 crisis on regional and local governments: Main findings from the joint CoR-OECD survey: OECD Regional Development Papers. Paris, 2020. 38 p. [Electronic resource]. Retrieved from https://www.oecd.org/cfe/the-impact-of-the-covid-19-crisis-on-regional-and-local-governments-fb952497-en.htm

11. The territorial impact of COVID-19: Managing the crisis and recovery across levels of government, 2021. [Electronic resource]. Retrieved from https://www.oecd.org/coronavirus/policy-responses/the-territorial-impact-of-covid-19-managing-the-crisis-and-recovery-across-levels-of-government-a2c6abaf/#section-d1e4246

12. Auerbach, A., William G., Byron L., & Louise S. (2022). Fiscal effects of COVID-19. Brookings Papers on Economic Activity: BPEA Conference Drafts, September 24, 229-278. [Electronic resource]. Retrieved from https://www.brookings.edu/bpea-articles/fiscal-effects-of-covid-19/

13. Dougherty, S., & de Biase, P. (2021). Who absorbs the shock? An analysis of the fiscal impact of the COVID-19 crisis on different levels of government. International Economics and Economic Policy, 18, 517–540.

14. Tax Policy Reforms 2021: Special Edition on Tax Policy during the COVID-19 Pandemic, OECD Publishing, Paris, 2021. 75 p. [Electronic resource]. Retrieved from https://www.oecd-ilibrary.org/taxation/tax-policy-reforms-2021_427d2616-en (дата обращения: 19.06.2022).

15. Information on tax expenditures of constituent entities of the Russian Federation: official website of the Ministry of Finance of the Russian Federation [Electronic resource]. Retrieved from https://minfin.gov.ru/ru/perfomance/budget/policy/raskhod/sub/

16. On endorsement of the list of sectors of the Russian economy most affected under deteriorating situation caused by the spread of a new coronavirus infection: Decree of the Government of the Russian Federation of April 3, 2020 N 434 [Electronic resource]. Retrieved from https://base.garant.ru/73846630/

17. On establishing requirements for the conditions and terms of the rent payment deferring under real estate lease agreements: Decree of the Government of the Russian Federation of April 03, 2020 N 439 [Electronic resource]. Retrieved from http://government.ru/docs/all/127163/

18. Koinova, K. A., & Gordienko, M. S. (2022). The impact of COVID-19 restrictions on the fiscal policy of the Russian Federation. Bulletin of EFiUP Universities, 1, 17-25.

19. Regions of Russia. Socio-economic indicators: statistical compendium. Moscow: Rosstat, 2021. 1112 p.

Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

Assessment of regional measures of tax support for business in the context of the COVID-19 pandemic, the beginning of 2020 became a reference point for the Russian economy, as the vector of the socio-economic agenda was dramatically changed. The spread of the new coronavirus infection COVID-19, coupled with the layered collapse in prices for energy exported by Russia to the lows of twenty years, required the Government to implement a package of measures to support businesses and citizens. First of all, a list of affected sectors of the economy was identified, for which support measures have become the most significant. A number of measures were aimed at supporting small businesses. The key areas of anti-crisis measures to support the economy are: subsidizing loans, direct financing of affected industries, reducing the tax burden, reducing the administrative and control burden on businesses. Accordingly, the COVID-19 coronavirus pandemic has also made adjustments to Russia's tax policy. The Government has taken a number of unprecedented anti-crisis tax measures to support the economy. The presented article is devoted to the problems of assessing measures to support the economy during the acute phase of the coronacrisis. The title of the article corresponds to the content. The purpose of the study is to assess tax support measures implemented in Russian regions during the pandemic through the prism of key budget parameters and indicators of socio-economic development. The author also formulated research tasks aimed at achieving the goal. The article highlights sections with subheadings, which corresponds to the presented requirements of the journal "Taxes and Taxation". In the "Introduction", the author characterizes the relevance and significance of the chosen research area, sets the purpose and objectives of the study. In the section "Countercyclical fiscal policy pursued at the federal and subnational levels: foreign experience", the author describes the experience of developed foreign countries in supporting the economy during the coronacrisis, isolating tax instruments. Of interest is the author's assessment of the impact of tax expenditures on the error in forecasting the growth rate of real GDP and the assessment of the impact of restrictive measures on the decline in GDP. In the section "Tax expenditures as a tool to stimulate economic activity: the experience of Russian regions", which is the main one in the article, the author conducts a comparative analysis of regions on the application of tax measures to support business in the context of a pandemic in the context of three main taxes: the STS, corporate property tax and the patent system. The section "Analysis of regional tax support measures through the prism of key budget parameters and indicators of socio-economic development" is a generalization. The author examines the results of the study taking into account the impact of falling tax revenues on the budget security of the regions. In the same section, the author formulates conclusions based on the results of the study. We suggest that the author highlight a separate section with conclusions at the end of the article. The research uses well-known general scientific methods: analysis, synthesis, comparison, ascent from the abstract to the concrete, logical method, etc. Among the specific economic research methods, the author applied statistical and correlation-regression analysis. The author makes extensive use of the possibilities of illustrating the research results in the article. There are 5 figures and 3 tables. The author should focus in more detail on the interpretation of the results of correlation and regression analysis in terms of assessing the influence of a factor on the result. According to all the presented results, it is impossible to talk about the presence of any significant relationship (on the Cheddock scale), and also taking into account the presented figures, it is not obvious that the dependence is linear. At the same time, the article does not analyze the presence of a nonlinear dependence. The chosen research topic is extremely relevant. This is due to the fact that the COVID-19 pandemic continues, and therefore the study of the experience of the regions of Russia and developed foreign countries in the field of smoothing the negative consequences of the coronacrisis with the help of tax instruments, evaluating the effectiveness of the measures applied, determining the best of them will be in demand in the wake of the ongoing crisis and at the stage of economic recovery, as well as in a mobilization economy. The lessons learned from this experience will certainly be useful for improving tools for overcoming and coping with such crisis phenomena in the future. The article has practical significance in terms of assessing the regional features of business tax support during the coronacrisis. Of interest is the author's conclusion that during the coronacrisis, the subjects of the Russian Federation introduced tax incentives for taxes that account for an insignificant share of regional budget revenues and which did not show a significant decrease by the end of 2020. According to the corporate income tax, which generates more than 30% of the revenue side of budgets and revenues from which decreased to a greater extent in 2020 compared to other taxes, tax benefits were not provided, which, according to the author, is justified. The results of the study can be used by regional authorities and the Government of the Russian Federation to improve tax policy. The author has not explicitly formulated the points of scientific novelty of the study. The increment of scientific knowledge nevertheless takes place in terms of approaches to assessing the effectiveness of tax policy measures during the coronacrisis from the standpoint of both stimulating the economy and budgetary security. At the same time, we suggest that the author supplement the study with an assessment of relative indicators – per capita, since in a comparative analysis of regions, taking into account their differences in budget provision, the use of absolute indicators is not entirely justified and may distort the results. For example, the groupings of regions by tax expenditures are given in absolute terms. How can the city of St. Petersburg and the Yaroslavl Region compare with each other in terms of the amount of tax revenues that have fallen out in absolute terms, if their population differs by 5 times, and budget revenues in 2020 – by 8 times? We believe that the article should be supplemented with the author's vision of scientific novelty. This will increase the attractiveness of the research to the general readership of the journal. The style of the article is scientific and meets the requirements of the journal. The set goal of the study has been achieved, as evidenced by the formed conclusions based on the results of the study. The bibliography is presented by 19 sources, which meets the requirements of the journal. The bibliography is formed primarily by foreign and Russian sources of statistical information, databases, as well as domestic research in the chosen field. The bibliographic apparatus in this article did not allow the development of a full-fledged scientific polemic, appeals to opponents are not sufficient, they should be expanded. For example, there is no analysis of a large-scale study on a similar topic conducted by the staff of the Tax Policy Center of the Financial Research Institute of the Ministry of Finance of the Russian Federation.

The advantages of the article include the following. Firstly, the relevance and significance of the chosen research area. Secondly, the breadth of view on the issues under consideration and the assessment and use of modern approaches to solving problems of international taxation. Thirdly, a practical illustration of the approaches under consideration using the example of foreign countries and Russian regions. Fourth, the breadth of use of illustrative material. Fifth, the use of statistical and correlation-regression analysis tools. The disadvantages include the following. Firstly, there is a need for a more thorough understanding of the results of correlation and regression analysis, as well as an assessment of the possibility of a non-linear relationship between the factors and the resulting indicators. Secondly, there is a need to supplement the study with an assessment based on relative indicators - per capita to confirm the correctness of the conclusions. Thirdly, the need to supplement the article with an explicit assessment of the elements of scientific novelty of the conducted research. Fourth, the need to expand the scientific debate and increase the number of studies on this topic in the list of references. These shortcomings need to be eliminated. Conclusion. The presented article is devoted to the problems of assessing measures to support the economy during the acute phase of the coronacrisis. The article reflects the results of the author's research and may arouse the interest of the readership. The article can be accepted for publication in the journal "Taxes and Taxation".

|

Eng

Eng