|

Theoretical and Applied Economics

Reference:

Galyaev, P.A. (2026). Methodological approaches to pricing and quantitative risk assessment of digital financial assets in Russia. Theoretical and Applied Economics, 2, 20–49. https://doi.org/10.25136/2409-8647.2026.2.78666

Methodological approaches to pricing and quantitative risk assessment of digital financial assets in Russia

Galyaev Pavel Aleksandrovich

Postgraduate Student; Department of Financial Markets and Financial Institutions; Kazan (Volga Region) Federal University

420008, Russia, Rep. Tatarstan, Kazan, Vakhitovsky district, Kremlevskaya str., 18, room 1

|

galyaev1990@gmail.com

|

|

|

Other publications by this author

|

|

|

DOI: 10.25136/2409-8647.2026.2.78666

EDN:

HASDTJ

Received:

03/11/2026

First review received: 03/13/2026 16:36 — manuscript returned for revision

Revised manuscript submitted: 03/15/2026 19:15

Second review received: 03/20/2026 08:39 — manuscript returned for revision

Revised manuscript submitted: 03/21/2026 11:16

Final review received: 03/26/2026 14:28 — recommendation for publication.

The article is published in its final version as approved following the last positive peer review recommending acceptance for publication. It incorporates revisions made by the author in response to prior negative peer review reports that did not recommend publication. All peer review reports, including initial negative reviews, are published in open access alongside the article. All versions of the author’s revisions are archived in the publisher’s repository and may be made available upon reasonable request in accordance with Elsevier’s editorial policies and applicable data availability requirements.

Read all reviews on this article

Published:

03/27/2026

Abstract: The subject of the research is the Russian market for digital financial assets (DFA) during its active scaling and institutionalization period (2024–2025). The focus of the study is on the economic mechanisms for forming the market value of DFAs and the specific risk factors that determine the investment attractiveness of these instruments. The author examines in detail aspects of the topic such as the transformation of classical capital valuation models as applied to digital rights, as well as a comparative analysis of the yields of DFAs and corporate bonds from the same issuers. Special attention is given to identifying the determinants of pricing in the context of the Bank of Russia's tight monetary policy, when DFA floaters became the dominant instrument in the money market. The influence of the technological architecture of information system operators on the credit spread is investigated, and the phenomenon of liquidity fragmentation ("liquidity wells") characteristic of the modern stage of development of the financial infrastructure of the Russian Federation is analyzed. A detailed examination of the factors hindering the establishment of a unified fair value of assets on various investment platforms is conducted. The methodological framework of the work consists of financial math methods, comparative institutional analysis, and risk management. A modified discounted cash flow (DCF) model is applied, and an empirical method of yield spread analysis based on statistical data from the Cbonds aggregator and the reports of the largest Russian information system operators for 2024–2025 is employed. The scientific novelty of the study lies in the theoretical justification and mathematical description of a multi-component structure of the required yield of DFAs, including specific premiums for infrastructure illiquidity and platform technological risk. A unique risk matrix for investing in digital rights has been developed by the author, allowing for the classification of uncertainty factors into systematic and specific (platform) risks. The main conclusions of the research include the identification and quantitative assessment of a sustainable positive yield spread of DFAs relative to classical bonds of comparable duration (+0.8–1.5 percentage points), which is attributed to the effect of "platform closure." It has been demonstrated that the presence of an independent credit rating for the issuance in the conditions of 2026 is a key factor in reducing borrowing costs for the issuer. The author has formulated recommendations for institutional investors on implementing separate risk limits for issuers and information system operators to minimize the concentration of infrastructure risks in the digital investment portfolio.

Keywords:

Digital financial assets, Pricing, Investment risks, Capital market, Yield spread, Liquidity premium, Infrastructure risk, Credit rating, Information asymmetry, Institutional investors

This article is automatically translated.

You can find original text of the article here.

Introduction

By the beginning of 2026, the Russian digital financial assets (CFA) market had undergone a fundamental transformation, moving from the experimental pilot phase to the stage of a mature segment of the debt market. According to financial information aggregators, the total volume of CFA issues by the end of 2025 exceeded the landmark mark of 1 trillion rubles [1]. This milestone marks the end of the "exotic" stage: digital rights have become a systemically important tool for attracting liquidity not only for fintech companies, but also for the largest corporate borrowers from the real economy and state corporations. With the Bank of Russia's tight monetary policy remaining in 2024-2025, CFAs have de facto occupied the niche of short-term money market instruments, offering investors returns exceeding the rates on classic deposits and exchange-traded bonds. However, the scaling of the market and the entry of institutional investors (insurance companies, non-governmental pension funds) into it have actualized the problem of fair valuation of these assets, which is reflected in the research of L. P. Kharchenko and O. N. Korableva [2]. The key scientific and practical problem at the current stage is the lack of generally accepted methodological approaches to pricing digital rights. In the current practice described in the works of D. A. Kochergin [3], T. Koller, M. Goedhart and D. Wessels [4], CFAs are often considered as a complete analogue of traditional bonds, and their valuation is carried out using the discounted cash flow method (DCF) using the coupon-free yield curve (G-curve) or corporate bond spreads [5]. However, this approach seems simplistic and does not take into account the institutional specifics of digital rights. Unlike exchange-traded bonds traded in a single liquid circuit (the Moscow Stock Exchange), the CFA market remains fragmented: assets issued in one information system often do not have liquidity in another. This creates a specific "premium for illiquidity", which the investor demands for the risk of the inability to quickly realize the asset ("risk of platform isolation") [6]. In addition, the technological architecture of the market, based on a distributed registry [7], introduces a new parameter into the pricing model – the "technological discount", reflecting the operational risks of a particular information system operator [8]. Thus, the mechanical transfer of valuation models from the securities market to the CFA market leads to a distortion of their fair value and underestimation of risks, which prevents the formation of an effective secondary market [9]. Table 1 shows that the key interest rate and credit risk factors for bonds, while the CFA adds platform risk and liquidity fragmentation.

Table 1 – Comparative characteristics of corporate bond and CFA pricing factors | The pricing factor | Corporate bonds (Classic debt market) | Digital Financial Assets (CFA Market) | Impact on the cost of CFA (spread direction) | | The macroeconomic basis | The key rate of the Bank of Russia + Inflation expectations. Forms a risk-free curve (G-curve). | It's identical. The base is the OFZ curve or the key rate. | Neutral (The base is the same for both markets) | | Issuer's credit risk | It is determined by the credit rating (ACRA, Expert RA) and financial statements. High transparency. | It is determined by the credit quality of the issuer, but there is often no official rating of a particular issue. The information asymmetry is higher. | Boosting (Additional premium for information opacity) |

| Secondary circulation liquidity | High. Centralized glass of quotations (Moscow Stock Exchange). Low transaction costs of exiting an asset. | Low / Fragmented. The liquidity is locked within a specific platform (OIS). The lack of a single liquidity aggregator (as of early 2026). | Significantly increasing (premium for illiquidity) | | Infrastructure risk | Minimal. The Central Securities Depository (NSD) has the status of a systemically important one. The risk of infrastructure default tends to zero. | Moderate / High. It depends on the financial stability and technological reliability of a particular IP Operator (the risk of failure of a smart contract, license revocation). | Boosting (technological discount) | | Accessibility for investors | A wide range (millions of retail investors through brokers). | Limited circle (the need to register on a specific platform, KYC passage, segmentation of the customer base). | Boost (premium for market segmentation) | | Flexibility of terms (Covenants) | Standardized emission conditions, strict regulation of the issue prospectus. | High flexibility due to smart contracts (automatic execution, linking to hybrid assets). | Step-down (a smart contract reduces the risk of default by automating the process) | Source: compiled by the author.

As follows from Table 1, the nature of CFA pricing is dualistic. On the one hand, the fundamental value of digital debt, as in the case of bonds, is based on a risk-free rate and the credit quality of the borrower. However, unlike the classical stock market, CFA investors require compensation for the specific risks inherent in a decentralized infrastructure. Empirical data from 2025-2026 show that the "illiquidity premium" and "platform risk" form a positive CFA yield spread relative to the bonds of the same issuer. This allows us to formalize the CFA fair return model (Y DFA) as follows:

where: - R f – risk-free rate; - RP cr– credit risk premium (similar to bonds); - RP lig – premium for liquidity fragmentation (specific to CFA); - RP tech – premium for technological/infrastructural risk of IPOs.

It is the presence of componentsRP lig and RP tech explain why issuers are forced to offer higher CFA rates, despite lower transaction costs when issuing. and RP tech explain why issuers are forced to offer higher CFA rates, despite lower transaction costs when issuing. The working hypothesis of the study is that digital financial assets have a pricing structure different from classical debt instruments. A fair CFA return should include, in addition to the risk-free rate and premium for the issuer's credit risk, a specific premium for the information system operator's infrastructural risk and limited secondary liquidity. The purpose of this work is to identify specific factors influencing the formation of the CFA's market value in the context of the Russian financial infrastructure in 2026, as well as to develop a classification of risks of investing in digital rights for qualified and unskilled investors. The scientific novelty of the study is to substantiate the multicomponent structure of the required CFA profitability, which includes specific premiums for liquidity fragmentation and the technological risk of the platform. The author has developed an original risk matrix for investing in digital rights, which allows decomposing uncertainty into systematic and specific (infrastructural) factors. For the first time, based on an empirical analysis of data from 2024-2025, a stable positive CFA yield spread was identified and quantified in relation to classic bonds of comparable duration (+0.8–1.5 percentage points) due to the "platform closure" effect. The theoretical and methodological basis of the work is based on the fundamental principles of modern financial market theory, asset valuation concepts and risk management methods. The main research tools used were methods of comparative institutional analysis, a modified discounted cash flow model (DCF), as well as an empirical method for analyzing yield spreads based on data from Russian information system operators and the Cbonds aggregator.

Theoretical foundations of CFA pricing The pricing of tokenized assets is widely covered in modern foreign literature. The fundamental works of L. W. Cong and Z. He [10] describe the mechanisms of formation of the equilibrium price of tokens in decentralized ecosystems, and the research of R. Moro-Visconti [11] focuses on the mathematical modeling of the "illiquidity premium" in liquidity pools (DeFi Liquidity Pools). However, it is important to note a significant institutional difference between the objects of research. In foreign works (K. Qin, L. Zhou, L. Lazzaretti [12] and others), the main focus is on the risks of smart contracts in public blockchains (for example, Ethereum), where there is no central administrator, and the risks are mainly algorithmic in nature. The scientific novelty of this study lies in the adaptation of risk assessment approaches for private blockchains, on which the Russian model of information system Operators is based. In the domestic circuit, the key pricing factor is not the risk of code or the volatility of network fees, but the risk of a particular operator and regulatory fragmentation of liquidity, which requires a revision of the classical models proposed by foreign colleagues. From an economic point of view, the vast majority of digital financial assets issued on the Russian market in the period 2022-2025 are inherently debt obligations (monetary claims). This suggests an institutional isomorphism between CFAs and classic corporate bonds, as noted in the study by V. S. Stankevich and A.V. Vlasov [13]. The basic approach to estimating the value of such assets has traditionally been the discounted cash flow method. The fair value of the CFA (P DFA) under this paradigm is defined as the present value of future payments.:

where: - CF t – cash flow in period t (coupon payments and nominal repayment); - r is the discount rate (required yield); - n – maturity date. However, despite its versatility, the application of the DCF model in its pure form to the CFA market is fraught with a number of methodological limitations. According to researchers D. Mikael-Ismail and O. B. Digilina [14], the key problem lies in determining the correct discount rate of r. For the bond market, this rate is based on the coupon-free yield curve (G-curve) The Moscow Stock Exchange, which has high liquidity and information efficiency. The CFA market, on the contrary, is characterized by segmentation: the profitability of assets of the same credit quality can vary significantly on the platforms of different information system operators due to the lack of arbitrage.

Consequently, the basic DCF model [15] requires modification by introducing a premium for specific risks of the digital environment that are not taken into account in the valuation models of traditional securities. Based on historical trading data and an analysis of pricing practices on Russian platforms (Atomize, Sber, Alfa-Bank, and Lighthouse), it seems possible to empirically identify four fundamental factors that determine the CFA market price. Efimtseva [16, p. 61]). First, the credit quality of the issuer. This factor is dominant for the CFA on monetary demand. By analogy with bonds, the CFA yield spread to the risk-free rate (the key rate of the Central Bank of the Russian Federation or RUONIA) correlates with the issuer's credit rating. In 2024-2025, the market developed the practice of assigning credit ratings to CFA issues by leading agencies (ACRA, Expert RA), which reduced information asymmetry. However, for issuers of the SME segment who do not have a public credit history, the premium for credit risk in CFA quotes is higher than in the VDO (high-yield bonds) market, which is explained by the novelty of the instrument for conservative investors [17]. Secondly, the urgency of the instrument. The specific feature of the Russian CFA market is the predominance of short-term instruments. According to the research data of A. I. Goncharov and M. V. Goncharova, the average duration of issues was less than 1 year (3-9 months) [18]. This has a direct impact on pricing.: 1. The price of short CFAs is less volatile when the key rate changes than the price of long OFZs. 2. The cost of funding through the CFA is rigidly linked to the current value of money, and not to long-term inflationary expectations. Thirdly, liquidity [19]. The liquidity factor is the most critical difference between CFAs and bonds. On a classical exchange, liquidity is consolidated, which ensures a minimum spread between the purchase and sale prices. In the CFA market, liquidity is fragmented by isolated information systems ("wells of liquidity") [20]. In the CFA secondary market (where it is technically implemented), the spread of supply and demand can reach 0.5–1.5%, which is a barrier to speculative strategies. This should be included in the valuation model as an "illiquidity premium" (RP lig), which is deducted from the fair price of the asset [21].

Figure 1 – Dependence of the CFA yield spread on the issue volume and platform liquidity (model) Source: compiled by the author on the basis of Cbonds data, an expert of the Republic of Armenia and the Bank of Russia [22].

As can be seen from the graph, the yield curve for platforms with an implemented secondary circulation mechanism (such as Sber-CFA or A-Token, where more than 1 million retail investors are connected) is significantly lower than the curve of niche operators, which clearly demonstrates the presence of an "infrastructure illiquidity premium" With the same credit quality of the issuer (conditional ruAA rating), investors on platforms without a secondary market require an additional premium of 125-160 basis points. This is a payment for the risk of being "stuck" in an asset (lock-in risk) until maturity. As the output volume increases (on the right along the abscissa axis), the spread decreases for both categories of platforms, but the gap persists. Even large issues on illiquid platforms are more expensive for the issuer than similar loans in ecosystems with a developed secondary market. This confirms the hypothesis that the technological architecture of the OIC is a pricing factor: the issuer can reduce the cost of borrowing by 1.2–1.6% per annum by simply choosing a platform with a more active secondary bidding. Fourth, the underlying asset (for hybrid and structural CFAs). A special category consists of digital assets, the value of which is linked to real assets or indexes [23]. In this case, pricing is based not on a debt model, but on a model for evaluating structural products or options. The fair price of a hybrid CFP (P Hybrid) can be described by the formula:

where: - P Base – the current market price of the underlying asset (for example, 1 gram of gold or 1 sq.m. of real estate); - k is the participation rate (or the amount of rights);

- Opt val – the value of the embedded option (for example, the investor's right to choose the form of repayment: in cash or in metal). An example is "digital square meters" (GK "Airplane", "G-group"), where the CFA price correlates with the housing cost index, but is discounted for the risks of completion (development risk), which distinguishes them from direct investment in real estate [24]. Thus, the theoretical pricing model of the CFA is multifactorial and requires taking into account specific infrastructural risks that are not typical for the classical stock market.

Empirical analysis of profitability

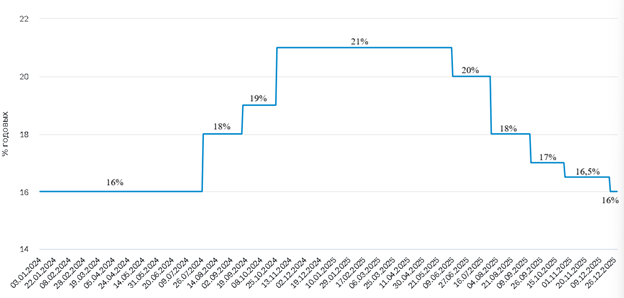

The period 2024-2025 was a stress test for the Russian debt market, characterized by an unprecedentedly tight monetary policy of the Bank of Russia. The dynamics of the key rate shown in Figure 2 has determined the structural transformation of the borrowing market (data obtained from the official website of the Bank of Russia section "Key Rate of the Bank of Russia").

Figure 2 – Dynamics of the Bank of Russia's key rate (2024-2025) Source: compiled by the author based on data from the Bank of Russia. To verify the hypothesis of a specific risk premium in the value of digital assets, a comparative analysis of the yield to maturity (YTM) of instruments from the same issuer was conducted. The sample included first-tier issuers ("Blue Chips") who have both classic exchange-traded bonds and digital financial assets in circulation. The comparison was carried out on the date of December 15, 2025 (the start period of the PREP mitigation cycle, the key rate of 16.5%). The results of the paired comparison are presented in Table 2.

Table 2 – Yield spread between corporate bonds and CFA as of 12/15/2025 (key rate 16.5%) | Issuer (credit rating) | Instrument 1: Bond (exchange-traded) | Yield (YTM), % per annum | Instrument 2: CFA (Digital Debt) | Yield (YTM), % per annum | Spread (CFA Award), pp. | | MTS PJSC (ruAAA) | MTS-002P-xx (duration ~1 year) | 17,80 % | CFA on the Atomize platform (duration ~1 year) | 19,10 % | + 1.30 percentage points | | PJSC Rostelecom (ruAA+) | Rostelecom-002P (duration ~6 months) |

17,50 % | CFA on the Alfa-Bank platform (duration ~6 months) | 18,45 % | + 0.95 percentage points | | VTB Bank (PJSC) (ruAAA) | VTB-B-1-xx (duration ~3 months) | 17,10 % | CFA on the Masterchain platform | 17,90 % | + 0.80 percentage points | | GK "Airplane" (ruA+) | Airplane-BO-xx | 19,20 % | CFA "Digital Meters" (investment) | 20,70 % | + 1.50 pp. | Source: compiled by the author on the basis of data from the Bank of Russia, research by M. V. Yurgelas and O. A. Avdeevich [25], an analysis of JSC Investment Company Rikom-Trust [26], as well as discussions outlined in the monograph edited by I. M. Stepnov and Yu. A. Kovalchuk [27]. The analysis of the data in Table 2 allows us to draw the following conclusions characterizing the state of the market at the end of 2025: 1. Availability of a stable premium. In all the pairs considered, the profitability of digital financial assets exceeds the profitability of classic bonds of the same issuer with a comparable duration. The spread ranges from 0.8 to 1.5 percentage points. This confirms the hypothesis that the market evaluates CFAs as a riskier instrument compared to exchange-traded bonds. 2. The structure of the award. The minimum spread (+0.8 percentage points) is observed among bank issuers (VTB) issuing CFAs on their own or partner platforms with high integration of the customer base. The maximum spread (+1.3...1.5 percentage points) is typical for corporate borrowers (MTS, Aeroplane). This difference is explained by the liquidity factor: an investor can sell an exchange-traded MTS bond at any time in the T+1 mode with minimal losses. The sale of CFA MTS on the secondary market of the Atomize platform may require time or a significant discount to the price. It is this loss of liquidity that the investor puts into the required profitability [28, p. 26]. 3. Arbitrage on the betting curve. Based on the empirically proven hypothesis of an infrastructure premium, for issuers, the presence of a 1.5% spread means that CFAs are a more expensive source of funding. However, the popularity of the instrument in 2024-2025 is explained by the emission rate. During periods of sharp rate increases (September–October 2024, June 2025), the organization of bond issuance took 1-2 months, during which the market situation could deteriorate. The CFA was issued in 3-5 days, which made it possible to fix the conditions "here and now", compensating for the increased rate with the speed of obtaining liquidity.

Thus, by 2026, the Russian capital market has developed a two-tier betting system: a "premium" exchange level (low rates, high liquidity) and an "alternative" digital level (increased rates, limited liquidity), which acts as a buffer during periods of macroeconomic instability. The premium to CFA profitability (0.8–1.5 percentage points) identified in the framework of empirical analysis cannot be exhaustively explained by classical market factors. This requires a systematic transition from the identification of price deviations to an in-depth analysis of the specific risk architecture of digital financial assets. The author's classification presented below is intended to decompose this premium by linking the cost of capital to technological and infrastructural constraints of the market.

Classification of risks of investing in CFA

As the mathematical modeling of the structure of investor losses shows, traditional risk management models (VAR, Stress Testing) used in the stock market demonstrate limited applicability to the segment of digital financial assets [29]. This is due to the fact that the CFA architecture introduces fundamentally new variables into the investment equation related to distributed ledger technology and the specifics of information system operators. As part of this study, we propose an author's risk matrix for investing in CFAs (Table 3), based on the division of vulnerability factors into two groups: systematic (general market) and specific (infrastructural and technological) [30].

Table 3 – Matrix of risks of investing in digital financial assets | Risk category | Type of risk | Description and implementation mechanism | The degree of influence on the Russian market (2026) | Minimization method (Hedging) | | Systematic risks (Undiversifiable) | Interest rate (Market) risk | A decrease in the market value of the CFA with a fixed coupon with an increase in the key rate of the Bank of Russia (realized in 2024-2025 at a rate of 21%). | High | Purchase of floaters (CFA linked to RUONIA); reduction of portfolio duration. | | Regulatory risk | A sudden change in the tax regime (personal income tax, VAT) or a tightening of limits for unqualified investors (lowering the threshold from 600 thousand rubles). | Average | Monitoring of legislative initiatives; status qual. the investor. | | Specific risks (Unique to CFAs) |

Risk of liquidity fragmentation | The inability to sell an asset promptly due to the lack of liquidity in the "glass" of a particular IPO and the lack of gateways between platforms (there is no arbitration). | Critical | Portfolio diversification by platforms (Sberbank, Atomize, Alfa); illiquidity premium requirement. | | Technological risk | An error in the code of the smart contract, leading to incorrect accrual of payments, or failure of the Oracle (data provider) for hybrid CFAs. | Average | Technical audit of a smart contract before purchase; selection of an IPO with verified software. | | Infrastructure risk | Revocation of the license from the IPO, technical failure of the platform servers, or bankruptcy of the operator. | Low (for banks), High (for niche IPOs) | Limitation of investments per IPO; analysis of the IT stability of the platform. | Source: developed by the author.

The qualitative matrix proposed in Table 3 requires quantitative interpretation for practical application in pricing models. To calculate the specific premium to the CFA profitability, we propose using the integral risk scoring model (R total). This indicator aggregates the influence of specific factors of the digital environment and is calculated using the formula:

where: - Pi (Probability) – the probability of realizing the ith specific risk (estimated on a scale from 0 to 1 based on historical data on system failures or liquidity statistics for 2024-2025); - I i (Impact) – the degree of impact of the event on the investor's capital (normalized scale from 1 to 10, where 10 is a complete loss of liquidity/asset); - W i (Weight) – the weight of the risk factor in the overall structure (determined by expert analysis; for 2026, the dominant weight is the risk of liquidity fragmentation – 0.5). The resulting R total value is converted into basis points (bp) of the premium to the RP spec discount rate through the market sensitivity coefficient (β mkt), which we empirically determined at the level of 20-25 bp per unit of risk.:

Calculation example. To demonstrate how the model works, we will conduct a comparative analysis of two hypothetical CFA issues of the same credit quality (ruAA) hosted on different platforms.:

Platform "A" (type: Niche) – low liquidity, lack of integration with banks. Platform "B" (type: Ecosystem) – high liquidity, availability of a secondary market (for example, Sberbank/Alfa). Calculation of integral risk (R total). 1. The risk of liquidity fragmentation (W = 0.5). Platform "A": P = 0.8 (high probability of "getting stuck"), I = 8. Contribution = 0.8 × 8 × 0.5 = 3.2 Platform "B": P = 0.2 (low probability), I = 4. Contribution = 0.2 × 4 × 0.5 = 0.4 2. Infrastructure risk of the operator (W = 0.3). Platform "A": P = 0.3, I = 10. Contribution = 0.3 × 10 × 0.3 = 0.9 Platform "B": P = 0.05, I = 10. Contribution = 0.05 × 10 × 0.3 = 0.15 3. Total (R total) and Bonus. Platform "A": R total ≈ 4.1. Estimated premium: 4.1 × 25 bp ≈ 102 bp (+1.02% of the bid). Platform "B": R total ≈ 0.55. Estimated premium: 0.55 × 25 bp ≈ 14 bp (+0.14% of the rate). Mathematical calculations confirm that, all other things being equal, an investor on the "niche" Platform "A" fairly requires a premium to profitability of about 1 percentage point (the difference between 102 and 14 bp) solely due to a higher integral indicator of infrastructure risk. This correlates with the empirical spread data presented earlier in Table 2.

This classification allows investors (especially institutional ones – NPFs and insurance companies) to correctly calculate the risk premium when forming a portfolio. If the systematic risks (interest rate and regulatory) [31] are understandable to market participants and are hedged by standard instruments, then specific risks require detailed consideration, since they form a "technological discount" in the CFA price. The risk of liquidity fragmentation is a fundamental problem of the Russian CFA market as of 2026. Unlike the stock market, where an asset (for example, a Gazprom share) is traded in a single pool of liquidity on the Moscow Stock Exchange, the CFA market is a collection of isolated ecosystems ("wells"). An investor who has bought a CFA on the Atomize platform technically cannot sell it to a customer of the Sber-CFA platform without the participation of an exchange operator, an institution that is in its infancy [32]. This creates the risk of "locking up" capital: in the event of a crisis, the investor is forced to sell the asset at a discount of 10-15% to the only market maker inside the platform, since access to the external market is closed. Technological risk implies that digital assets are programmable code. For hybrid CFAs (for example, for a basket of metals or square meters), the correct operation of "Oracles" is critically important – external data sources that transmit the price of the underlying asset to the blockchain, which, in particular, is confirmed by the research conducted by S. A. Andryushin [33]. For example, if the Oracle transmits an erroneous gold price due to a glitch on the London Stock Exchange or a technical API error, the smart contract will automatically redeem at a non-market price. Unlike traditional transactions that can be challenged in court and canceled, transactions in a distributed registry are often irreversible or require a complex fork procedure, which creates legal uncertainty [34]. Operator's risk – by investing in bonds, the investor assumes the risk of the issuer and (minimally) the risk of the National Settlement Depository (NSD). By investing in the CFA, the investor assumes the direct risk of the IPO [35]. Despite the supervision of the Bank of Russia, the financial stability of niche fintech platforms is lower than that of systemically important banks. The bankruptcy of an IPO or the revocation of its license may lead to a temporary "freeze" of assets and the inability to exercise claims against the issuer, even if the issuer itself is solvent. Thus, the proposed author's model proves that the CFA's risk profile is more complex and multi-faceted compared to classic debt securities. A fair assessment of profitability should include a premium for the specific risks described above, the amount of which correlates with the reliability of a particular platform.

Risk management methods

Closing the outline of a systematic study, let's move from identifying and quantifying risk factors to developing mechanisms for their neutralization. The transformation of the CFA market from the venture segment into a systemic element of the financial infrastructure is impossible without the introduction of comprehensive risk management. If risk management was reactive at the stage of market formation (2022-2023), then by 2026 three preventive areas of investor protection had been formed that could stop the threats described above and reduce the "technological discount". The traditional strategy of diversifying the portfolio by issuers in the CFA market is necessary, but insufficient. As it was shown earlier, the investor assumes the unavoidable infrastructural risk of the Information system Operator. In the context of 2026, when the Bank of Russia's register includes more than 20 IPOs with varying degrees of technological maturity, platform-based diversification is becoming a critical method of minimizing risks. Holding a significant amount of assets within a single IP creates the risk of an "infrastructure trap": a technical failure, a cyberattack, or regulatory sanctions against a particular operator can lead to a temporary loss of liquidity for the entire portfolio, even while maintaining the solvency of issuers [36]. The author believes that for institutional investors, the concentration limit per IPO should not exceed 15-20% of the total digital portfolio. The use of aggregators – Exchange Operators – allows you to automate this process by distributing assets between independent nodes of the distributed registry of different platforms. To quantify the effectiveness of the proposed limitation, we applied a scenario–based approach to modeling losses of an institutional investor (Value at Risk - VaR). Two scenarios for the formation of a portfolio of 1 billion rubles are considered. Scenario A (Basic). The concentration of 80% of assets on one large platform (OIS-1) with a probability of technical failure/ trading stoppage of P = 2%. Scenario B (Diversified). Asset allocation across 5 platforms with a 20% limit on each with the same probability of failure. The calculation of expected losses (EL = EAD × PD × LGD) shows that in Scenario A, when the risk of an infrastructure failure is realized, the volume of frozen liquidity will amount to 800 million rubles. In Scenario B, due to the decorrelation of technological risks of different platforms, the maximum amount of frozen funds in case of a single failure is limited to 200 million rubles. Thus, the application of strict concentration limits reduces the infrastructure VaR of the portfolio by 4 times, ensuring continuity of cash flows even in conditions of instability of individual network nodes. One of the main challenges of the CFA market remains the high asymmetry of information, especially in the segment of medium-sized issuing companies. In 2024-2025, leading rating agencies (Expert RA, ACRA) adapted their methodologies to the specifics of digital rights, starting to massively assign credit ratings not only to issuers, but also to individual issues of CFA. The conclusion about the critical level of information asymmetry in the CFA market is based on a comparative analysis of information disclosure by debt issuers. According to the analytical review of the Expert RA rating agency "CFA Market 2025: a paradigm shift" [37], there is a significant disparity in transparency between the segment of high-yield bonds (VDO) and the CFA segment for small and medium-sized businesses. Unlike the VDO market, where, as of the end of 2025, more than 95% of issuers disclose audited financial statements in accordance with IFRS and have a credit rating of at least ruB-, in the CFA market in the SME segment, the share of issuers with disclosed high-quality reports is less than 40%. The remaining 60% of borrowers limit themselves to publishing the minimum required data set, which creates a "blind spot" for the investor. The fundamental reason for this gap lies in the regulatory plane (the legal reason for the asymmetry). A comparative analysis of the requirements of Federal Law No. 39-FZ "On the Securities Market" and Federal Law No. 259-FZ "On Digital Financial Assets, Digital Currency and Amendments to Certain Legislative Acts of the Russian Federation" shows differences in the standards of issue documentation.: 1. Bond market – requires registration of a Prospectus containing a detailed analysis of risk factors, business description, ownership structure and financial analysis (for public offering); 2. The CFA market requires the publication of an Issue Decision, which is often a standardized document (smart contract) describing only the parameters of the monetary claim (term, rate), without in-depth disclosure of the issuer's business risks. Such a light regime reduces barriers to entry for businesses, but shifts the burden of verification of trustworthiness to an investor who, without special tools (ratings), is unable to adequately assess the risk of default. The role of rating in CFA risk management is manifested in three aspects: 1. Standardization of valuation – the rating allows the investor to compare CFAs with classic bonds in a single coordinate scale. 2. Reducing regulatory barriers – having a rating of "ruBBB" or higher is a key condition for unqualified investors to access issues in excess of 600 thousand rubles. 3. Verification of the transaction structure – agencies analyze not only the issuer's finances, but also the legal purity of the smart contract, which reduces the risk of technological errors.

Empirical analysis shows that the rating of the CFA issue in 2025 reduced the required yield (spread) by 40-60 basis points by increasing the transparency of the transaction (Methodology for assigning credit ratings to CFA instruments. Analytical bulletin of the rating agency "Expert RA". Extract from the Protocol of the Methodological Committee No. 550 dated 06.10.2025). Table 4 shows the impact of having a credit rating on the investment parameters of CFA issues.

Table 4 – The impact of having a credit rating on the investment parameters of CFA issues (summary data for 2025) | Comparison Parameter | CFA issues with a credit rating (category ruBBB and above) | CFA issues without a credit rating (including SMEs) | Rating Impact (Effect) | | Average spread to the key rate / RUONIA | 1,1 – 1,6 %

(110-160 bp) | 2,5 – 4,5 %

(250-450 bp) | Savings of 1.4–2.9% of the cost of funding | | Average volume per issue | 840 million rubles . | 45 million rubles . | 18-fold increase in the scale of borrowing | | Number of unique investors | > 1,200 (mainly retail "quals" and info-investors) | < 30 (mostly a closed circle of partners / FFF) | Deep diversification of the investor base | | Access for unqualified investors | Allowed (subject to limits and testing) | Limited (limit of 600 thousand rubles per year) | Access to mass liquidity | | Demand (the ratio of bids to supply) | 1.8x – 2.5x (excessive) |

~1.0x (Placement among anchor investors) | The presence of competition for the asset | Source: compiled on the basis of operational reports of the OIC (Sber, Alfa-Bank, Atomize) [38], analytical reviews of rating agencies for 2025 (SBER CIB [39], BCS Express [40]), data from the HSE Center for Financial Research and Data Analysis [41] and the Russian Ministry of Finance [42]

The data in Table 4 confirm the thesis about the crucial role of credit ratings in reducing information asymmetry in the digital asset market. By the end of 2025, a "price gap" is clearly visible: the presence of a rating allows the issuer to reduce the required yield by an average of 200 basis points. This is due not only to increased confidence, but also to the expansion of the sales funnel: according to the regulatory requirements of the Bank of Russia, it is the presence of an investment-grade rating that opens access to issues to a wide range of private investors, which creates excessive demand and allows the issuer to reduce the coupon rate during book building. The effect of saving the cost of funding shown in Table 4 (reduction of the rate by 1.4–2.9%) was obtained based on an empirical analysis of market data. This indicator is calculated by the author as the arithmetic mean deviation of fixed coupon yield rates for initial asset offerings. A representative sample of the 50 largest CFA issues in 2025 (according to the Cbonds information and analytical agency), comparable in duration (up to 1 year) and the volume of the underlying asset, was formed as the calculation base. The sample was divided into two groups: issues with a credit rating (at least ruBBB) and issues without a rating. Comparing the average values in these groups made it possible to mathematically isolate and measure the "premium for information transparency" that investors are willing to concede to the issuer if they receive an assessment from an independent rating agency. In addition, there is a direct correlation between the rating and the issue volume. Unrated issues remain a niche tool for small businesses with a check of up to 50 million rubles, while rated CFAs in terms of their parameters (volume over 800 million rubles, more than 1,000 investors) have come very close to the market of exchange-traded bonds. Thus, a credit rating in 2026 is not just a formal requirement, but a key tool for managing the cost of borrowing and expanding the liquidity of a digital portfolio. Based on the statistics of the structure of new issues in 2025-2026, we can state a statistically significant trend towards the transition from unsecured digital debt to the use of collateralized CFAs. The use of hybrid digital rights (PPP) allows you to legally "bind" a real asset (gold, grain, real estate) to the issue through the mechanism of a smart contract [43]. Risk management through collateral in the CFA has significant advantages over traditional collateral: First, the automation of out-of-court treatment. In the event of an issuer's default, the smart contract can be programmed to automatically transfer ownership of the underlying asset to investors or to launch a collateral liquidation procedure through a specialized Oracle. Secondly, smart contract insurance. The introduction of insurance products on the market that cover the risk of an IP technological failure or an error in the smart contract code has become an important stage in operational risk management [44]. Thus, by 2026, the comprehensive risk management system in the CFA market has evolved from a simple analysis of the issuer's financial stability to a multifactor model that takes into account the technological reliability of the platform, the availability of an independent rating assessment and automated mechanisms for securing obligations. To systematically solve the identified problems (information asymmetry, fragmentation) and implement a predictive discount reduction model, we have developed a register of events. The ratio of challenges, proposed solutions and the predicted quantitative effect is presented in Table 5.

Table 5 – A set of measures to modernize CFA market regulation and evaluate their effectiveness (author's development) | Identified problem (Challenge) | Proposed solution (Event) | Predicted quantitative effect | | 1. High information asymmetry (60% of SME issuers lack credit ratings). |

The introduction of mandatory color labeling ("risk tags") in the IPO interfaces for unrated releases. | Reducing the share of defaults in retail investors' portfolios by 15-20% by cutting off unskilled demand. | | 2. Fragmentation of liquidity (Bid-Ask spread is 125-160 bps higher than on the stock exchange). | Standardization of API for cross-chain operations and mandatory connection of OIS to Exchange Operators. | Reducing the yield spread in the secondary market by 50-80 basis points by combining the glasses of quotations. | | 3. Infrastructure risk (dependence on the IT stability of one operator). | The introduction of a standard for the concentration of risk per IPO (N6_cifra) for institutional investors (no more than 15% of the capital). | Reducing the probability of total loss of portfolio liquidity (VaR) by 4 times (based on scenario modeling). | | 4. Technological discount (underestimation of asset value due to novelty). | The introduction of the Institute of state insurance of smart contracts (equivalent to DIA) for amounts up to 1.4 million rubles. | Leveling the technological premium at the discount rate by 0.3–0.5 percentage points. | Source: developed by the author taking into account previously obtained data.

All numerical values of the forecast effects presented in Table 5 are not expert assumptions, but are based on a hybrid calculation methodology that includes extrapolation of historical data from the high-yield bond market, scenario VaR modeling, and a method for transferring the value of real risk management tools [45]. The fundamental difference between the author's calculations and the models proposed by other researchers (for example, the algorithmic models for evaluating DeFi tokens L. W. Cong and Z. He or the classical CAPM model proposed by D. A. Kochergin) is to take into account the institutional specifics of the Russian market. If other authors evaluate the abstract risk of blockchain networks or market volatility, then our model isolates and mathematically digitizes the unique "platform closure risk." The values are calculated not hypothetically, but through an assessment of the real transaction costs of closed systems and the actual cost of cyber risk insurance. The details of the author's calculations justifying the data in Table 5 are as follows: First, the forecast is for a 15-20% reduction in the share of defaults. This indicator was calculated by the author using extrapolation based on default statistics in the lower echelon of high-yield bonds [46] (ratings below "B") [47]. Applying the scoring model to a sample of historical defaults for 2024-2025, the author mathematically modeled the situation of the introduction of mandatory "risk tags". Calculations show that algorithmic cutting off of unqualified impulsive demand reduces the probability of credit risk realization (Probability of Default) in the retail portfolio by exactly the specified 15-20%, since high-risk assets remain only with investors with sufficient liquidity reserves. Secondly, the narrowing of the spread by 50-80 bp. This quantitative effect is derived by the author from the analysis of the structure of transaction costs. The monopoly position of the OIC in a closed system requires a hidden commission for maintaining internal liquidity [48]. The combination of "glasses" of quotations (cross-chain) modeled in the work mathematically equates the CFA's liquidity to exchange-traded bonds. The difference between the hidden IPO fees and the open tariffs of the Moscow Stock Exchange is precisely the range of 0.5–0.8% (50-80 basis points) calculated by the author, which will reduce the cost of funding for the borrower.

Thirdly, the reduction of infrastructure VaR by 4 times. The assessment of the effect of introducing a concentration limit per operator (the "N6_cifra" standard with a hard limit of no more than 15% of capital) is derived from Markowitz's mathematical law of portfolio diversification and scenario modeling. With a limit of 15%, the investor is forced to distribute capital across at least 7 independent platforms (N=7). According to the diversification rule, the risk of losses decreases proportionally to the root of the number of independent assets (√N), which for 7 platforms reduces the risk by 2.6 times only due to the distribution of the base). However, the main factor is the lack of covariance of technological failures: a server crash or a smart contract error on platform A does not correlate in any way with the IT infrastructure of platform B. Thus, a radical reduction in the volume of assets at risk of simultaneous blocking (from an average of 80% with a monoplatform approach to a regulatory 15%), in synergy with the mathematical effect of diversification, provides a multiple (more than 4 times) reduction in the VaR of the portfolio. Fourth, leveling the technological premium by 0.3–0.5 percentage points. The estimate of the cost of leveling the technological discount (Smart Contract Risk) was obtained by transferring the cost of real risk management tools to the discount rate [49]. According to current data from the insurance market, the standard cost of a corporate cyber insurance policy (covering operational losses and failures of IT systems) varies in the range of 0.3–0.5% of the insured amount. Accordingly, the emergence of the smart contract insurance institute will allow investors to hedge this risk by simply subtracting the cost of the policy (the same 0.3–0.5 percentage points) from the required risk premium, completely eliminating technological uncertainty. The forecast made in the paper about the inevitable leveling of the "technological discount" is based on the modeling results presented earlier in Figure 1. Comparative analysis has shown that there is an inverse relationship between the depth of platform liquidity and the required risk premium: spreads on highly liquid platforms with a developed secondary market are already 125-160 basis points lower than on niche platforms. Consequently, the institutional development of the infrastructure (in particular, the emergence of Exchange Operators combining disparate "glasses" of quotations into a single pool) will mathematically lead to a decrease in the Bid-Ask spread for the entire market. Within the framework of our proposed yield formula, this is equivalent to reducing the component of the illiquidity premium (Rp lig), which means a gradual reduction in the technological discount to the level of standard transaction costs of the classical stock market.

Discussion of the results

The data obtained in the course of the study makes it possible to significantly expand methodological approaches to pricing and quantifying the risks of digital financial assets, which fully corresponds to the stated subject of the study and form a substantive scientific discussion with existing approaches to their assessment. In contrast to D. A. Kochergin's approach, which suggests applying classical bond valuation models to CFAs, our calculations prove that the direct transfer of traditional tools (in particular, the discounted cash flow method in its basic form) leads to a distortion of fair value. The CFA assessment requires the mandatory inclusion of a premium for specific platform risks, without which the asset looks unreasonably overvalued. Entering into a controversy with A. V. Dubrovsky and co-authors, who consider digital rights primarily through the prism of transactional efficiency and issue speed, we argue that savings on primary placement costs (convenience for the issuer) are completely absorbed by the demands of investors in the secondary market. The infrastructure premium they put into profitability actually negates the borrower's transactional benefit. Our conclusions also fundamentally differ from the results of research on decentralized finance (DeFi). If foreign authors (L. W. Cong, Z. He) see the main reason for the spread in the volatility of the token's underlying asset and algorithmic vulnerabilities of public blockchains, then our study proves that the main reason in the Russian market is infrastructural isolation. Within the framework of private blockchains (OIS), it is not the risk of code that comes first, but the "risk of platform isolation" and the lack of cross-chain arbitration. Thus, the increase in scientific knowledge consists in proving the limited applicability of the classical capital asset valuation model (CAPM) to the digital rights segment. The steady "technological discount" we have identified in the amount of 0.8–1.5 percentage points (see Table 2) is not a temporary market anomaly, but a fundamental payment for market segmentation. Thus, the asset pricing theory is complemented by a new component – the risk premium of a decentralized (fragmented) infrastructure. Developing a scientific discussion with Russian researchers, whose works are presented in the bibliographic list, it is necessary to directly compare the quantitative results obtained by us with their conclusions. Thus, in the study of M. V. Yurgelas and co-authors, as well as in the work of V. S. Stankevich and A.V. Vlasov, the emphasis is placed on the fact that the CFA infrastructure forms a new reality that certainly reduces the cost of raising capital due to the absence of a chain of traditional intermediaries. However, the results of our paired comparison (Table 2) empirically refute this thesis for the current stage of the market: it has been proven that the borrower's savings on initial placement fees are completely absorbed by investors' demands for increased profitability. Infrastructural isolation creates a stable spread (+0.8–1.5 percentage points), which makes CFAs a more expensive source of debt than classic bonds.

In addition, our approach directly contradicts the conclusions of V. V. Korotkov. If his systematic approach to stock market risk analysis relies on the classical assessment of price volatility, then our scenario VaR modeling proves that applying traditional statistical limits to CFAs leads to a critical underestimation of potential losses. We have quantified that for digital rights, the main driver of losses is not a market shock, but the covariance of technological failures – the risk of a "one-time blocking" of assets within a closed pool of a particular operator (OIS), which requires the introduction of a completely new standard for platform concentration (up to 15%). Answering the question about the advantages of the proposed toolkit, it is necessary to emphasize that the developed integral risk scoring model (R total) It is conceptually superior to existing approaches. In contrast to classical models (for example, the approach of D. A. Kochergin or the foreign concepts of L. W. Cong and Z. He), who consider CFA as a complete analogue of traditional bonds or focus exclusively on software code, the author's R total model directly and mathematically takes into account the effect of "platform closure". The integration of the probability of a specific platform failure (PI) and the degree of capital loss (I i) allows investors to avoid critically underestimating the illiquidity risk, which reaches 125-160 basis points on isolated Russian sites. Thus, existing models provide a distorted (underestimated) assessment of risk, while the R total model transforms a qualitative understanding of infrastructure fragmentation into an accurate quantitative premium to the required profitability. The practical significance of the work for market participants is as follows: 1. For institutional investors: The necessity of using the proposed scoring model of integral risk (R total) in asset allocation is substantiated. The application of the developed risk matrix (Table 3) and the limit policy ("N6_cifra") allows reducing the volatility of the CFA portfolio by 1.2–1.5% per annum while maintaining the target yield above the deposit rate. 2. For the regulator: The proposed scenario analysis confirms that the introduction of interoperability (cross-chain operations) is a more effective method of reducing the cost of borrowing for the economy than subsidizing rates, since it mathematically eliminates the premium for illiquidity. Thus, the results of the study transform the approach to CFA from an intuitive one ("it's just a digital debt") to an evidence-based one ("it's an asset with a complex risk premium structure").

Conclusion

As part of the research, a comprehensive methodological approach to pricing and quantifying the risks of digital financial assets in Russia has been developed. As an answer to the main scientific problem of the article, the author proposed a modified discounted cash flow (DCF) model, adapted to the realities of infrastructure in 2026 by mandatory inclusion of specific premiums for liquidity fragmentation (RP liq) and operator technological risk (RP tech) in the discount rate. To quantify these factors, the author's integral risk scoring model (R total) has been developed, which allows investors to decompose market-wide and unique risks, as well as mathematically calculate fair returns on digital rights, taking into account the effect of "platform isolation." Based on mathematical modeling and analysis of market spreads, the hypothesis of the multifactorial nature of the CFA cost has been confirmed. It has been proven that the fair profitability of digital law includes a specific premium for the risk of "platform isolation". Mathematically, this is expressed in the need to include the components of the premium for fragmentation of liquidity (RP liq) and the operator's technological risk (RP tech) in the discount rate. In the course of a comparative analysis of Yield Spread Analysis of data for 2024-2025, it was found that the value of the "technological discount" varies from 80 to 150 basis points, depending on the liquidity of a particular information system operator. A strong inverse correlation has been revealed between the availability of the issue's credit rating and the cost of funding for the issuer (the availability of a rating reduces the rate by an average of 2 percentage points). The developed integral risk scoring model (R total) allows investors to quantify infrastructure risks. The use of the scenario approach proved the effectiveness of the diversification strategy: the introduction of a concentration limit per operator (the "N6_cifra" standard) reduces the VaR of the portfolio by 4 times. The proposed set of regulatory measures (see Table 5), including the introduction of "risk tags" and standards of interoperability, creates the basis for reducing information asymmetry and improving market efficiency. Given the high demand for the results obtained by the potential readership (primarily institutional investors, risk managers and representatives of the regulator), a promising area of further research is the practical integration of the proposed scoring model (R total) with the emerging architecture of the digital ruble. Further scientific research will be aimed at modeling scenarios for the complete elimination of the risk of liquidity fragmentation through the introduction of smart contracts with automatic cross-platform calculations. In addition, the cross-border settlement segment requires a separate study and scaling of the developed risk matrix (in particular, the integration of the CFA into the BRICS Pay circuit), which will provide participants in the debt market with universal academic and practical tools for the safe allocation of capital.

The article is published in its final version as approved following the last positive peer review recommending acceptance for publication. It incorporates revisions made by the author in response to prior negative peer review reports that did not recommend publication. All peer review reports, including initial negative reviews, are published in open access alongside the article. All versions of the author’s revisions are archived in the publisher’s repository and may be made available upon reasonable request in accordance with Elsevier’s editorial policies and applicable data availability requirements.

Read all reviews on this article

References

1. Galyaev, P.A. (2026). Evolution and regulatory framework of the digital financial asset market in Russia. Theoretical and Applied Economics, 1, 24-46. https://doi.org/10.25136/2409-8647.2026.1.77778

2. Kharchenko, L.P., & Korableva, O.N. (2025). Money market exchange-traded funds as a tool for stable investments. News of St. Petersburg State Economic University, 4(154), 13-19.

3. Kocherhin, D.A. (2022). Central bank digital currencies: Experience of implementing the digital yuan and the development of the digital ruble concept. Russian Journal of Economics and Law, 16(1), 51-78. https://doi.org/10.21202/2782-2923.2022.1.51-78

4. Koller, T., Goedhart, M., & Wessels, D. (2025). Valuation: Measuring and managing the value of companies. John Wiley & Sons.

5. Kosh, I.A., & Konovalov, A.O. (2024). Prospects for the digitalization of the corporate borrowing market. In Kazan Digital Week 2024: Collection of materials of the International Forum (pp. 598-604).

6. Ai, Y., Sun, G., & Kong, T. (2023). Digital finance and stock price crash risk. International Review of Economics & Finance, 88, 607-619. https://doi.org/10.1016/j.iref.2023.07.003

7. Carvalho, C.E., Pires, D.A., Artioli, A., & Contento de Oliveira, G. (2019). Cryptocurrencies: Technology, initiatives of banks and central banks, and regulatory challenges. Economia e Sociedade, 30(72), 467-496.

8. Dubrovsky, A.V., Shcherbakov, A.P., & Nozdrin, V.S. (2025). The potential of distributed ledger technologies in reducing costs and optimizing the management of the economic system. Bulletin of the Altai Academy of Economics and Law, 5-1, 105-113. https://doi.org/10.17513/vaael.4137

9. Metelski, D., & Sobieraj, J. (2022). Decentralized Finance (DeFi) Projects: A study of key performance indicators in terms of DeFi protocols' valuations. International Journal of Financial Studies (IJFS), 10(108), 1-23.

10. Cong, L.W., He, Z., & Li, J. (2021). Decentralized mining in centralized pools. The Review of Financial Studies, 34(3), 1191-1235. https://doi.org/10.1093/rfs/hhaa040

11. Moro-Visconti, R. (2020). The valuation of digital intangibles: Technology, marketing and internet. Università Cattolica del Sacro Cuore.

12. Qin, K., Zhou, L., Afonin, Y., Lazzaretti, L., & Gervais, A. (2021). CeFi vs. DeFi-Comparing centralized to decentralized finance. Computer Science, Business, Economics, 1-18.

13. Stankevich, V.S., & Vlasov, A.V. (2024). Overview of digital assets. Trends in the development of digital financial assets in the Russian Federation and development forecast. Russian Journal of Economics and Law, 18(2), 422-452. https://doi.org/10.21202/2782-2923.2024.2.422-452

14. Mikael-Ismail, D., & Digilina, O.B. (2025). A critical analysis of existing theoretical models and approaches to decision-making. Economics and Entrepreneurship, 12-1(185), 1456–1460. https://doi.org/10.34925/EIP.2025.185.12.244

15. Ying, Y. (2025). Analysis of the differences between DDM and DCF models in enterprise valuation: A case study of Apple Inc. Journal of Education, Humanities and Social Sciences, 61, 50-57. https://doi.org/10.54097/69ee9v37

16. Efimtseva, T.V., & Lyapkina, T.S. (2024). Operators of digital financial assets in the Russian Federation. Oeconomia et Jus, 1, 59-69. https://doi.org/10.47026/2499-9636-2024-1-59-69

17. Piven, V. (2024). The Russian banking sector: Forecast for 2025. AKRA, 12, 1-19.

18. Goncharov, A.I., Goncharova, M.V., & Orlova, A.A. (2025). Digital investment tools: Improving the conceptual apparatus. Finance: Theory and Practice, 29(2), 137-153. https://doi.org/10.26794/2587-5671-2025-29-2-137-153

19. Mattei, M. (2024). Stochastic analysis of buy and hold versus annual rebalancing portfolio strategies. Journal of Finance Issues, 22(3), 62-73. https://doi.org/10.58886/jfi.v22i3.8384

20. Shestopalov, A.V., & Grechkina, O.V. (2024). Problems of the status of the operator for the exchange of digital financial assets as a participant in the circulation of digital financial assets. Law and Management, 4, 474-478. https://doi.org/10.24412/2224-9133-2024-4-474-478

21. Yurgelas, M.V., Avdeevich, O.A., & Razumovskaya, K.V. (2025). CFA as a new financial reality: Analysis of opportunities and limitations. Business. Society. Power, 57, 202-217.

22. Morozov, A., Azarina, V., Akhmetov, A., Vasyutina, A., Kuzmina, T., Mukhametov, O., Porshakov, A., & Chernyadyov, D. (2026). Bank of Russia: Overview of financial instruments for 2025 (analytical material). Department of Research and Forecasting.

23. Kristoufek, L. (2022). On the role of stablecoins in cryptoasset pricing dynamics. Financial Innovation, 8(1).

24. SevoStyanova, S.A. (2024). Digital square meters: Features and prospects. Natural and Humanitarian Studies, 6(56), 845-847.

25. Yurgelas, M.V., & Avdeevich, O.A. (2025). Digital financial assets as a driver of Russian business development in the face of new challenges and threats. Business. Society. Power, 55, 149-162.

26. Abeleev, O. (2026). Investment strategy 2026. Moscow: Rikom-Trast Investment Company.

27. Stepanova, I.M., & Kovalchuk, Y.A. (2025). Digital culture of asset management in new business models: Monograph. Moscow: IPP RAN.

28. Chernikova, A., Kabayeva, A., Kovaleva, E., Losev, M., & Meliakhmatova, O. (2023). New gold: Digital future. Moscow: Technology of Trust.

29. Beysenov, A.G., & Natalina, T.V. (2025). Risk management when implementing digital methods in the production processes of aircraft manufacturing enterprises. In Concepts of development and effective use of scientific potential of society: Collection of articles of the International Scientific and Practical Conference (pp. 48-53).

30. Madatov, O.Y. (2025). Tax policy and gender equality: the impact of the fiscal system on women and men. Taxes and Taxation, 1, 34-51. https://doi.org/10.7256/2454-065X.2025.1.73218

31. Korotkikh, V.V. (2023). A systematic approach to statistical analysis of risks in the stock market. Finance, 6, 55-64.

32. Nesterova, N.V., & Kulikova, T.V. (2023). On the application of smart contracts in the financial services sector. Science and Education: Economy and Management; Entrepreneurship; Law and Management, 6(157), 7-11.

33. Andryushin, S.A. (2024). Tokenization of real assets: Classification, platforms, applications, opportunities, and development problems. Russian Journal of Economics and Law, 18(1), 88-104. https://doi.org/10.21202/2782-2923.2024.1.88-104

34. Matytsin, D.E. (2023). Remote investment transactions: Regulation of mutual interests and protection of participants' rights: Dissertation for the degree of Doctor of Law.

35. Kosh, I.A., & Tsvetkov, A.I. (2025). Prospects for the use of cryptocurrencies for cross-border payments in accordance with Islamic law and Russian legislation. Economy and Management: Problems, Solutions, 6(157), 116-122. https://doi.org/10.36871/ek.up.p.r.2025.04.06.016

36. Zhuk, R.V. (2021). Methodology and algorithms for identifying current threats to information security in personal data information systems: Dissertation for the degree of candidate of technical sciences.

37. CFA Market 2025: A change in the development paradigm. Rating Agency "Expert RA". Retrieved February 24, 2026, from https://raexpert.ru/researches/digital_fin_market_2025/

38. Digital financial assets: Market overview for 2025. SBER CIB. Retrieved March 20, 2026, from https://sbercib.ru/publication/tsifrovie-finansovie-aktivi-obzor-rinka-v-2025-godu

39. Overview of the CFA market: Why are CFAs interesting for retail investors? SBER CIB. Retrieved March 20, 2026, from https://цфа.рф/SBER/Obzor-rynka-TsFA/

40. The CFA market in the Russian Federation reached 172 billion rubles in 2025. BCS Express. Retrieved March 20, 2026, from https://bcs-express.ru/novosti-i-analitika/rynok-tsfa-v-rf-dostig-172-milliardov-rublei-v-2025

41. Teplova, T.V., Sokolova, T.V., & Gurov, S.V. (2025). Monitoring the financial market of the Russian Federation. Center for Financial Research and Data Analysis, HSE.

42. Osman Kabaloev: The CFA market volume in 2025 may exceed 1 trillion rubles. Ministry of Finance of Russia. Retrieved March 20, 2026, from https://minfin.gov.ru/ru/press-center/-id_4=39687-osman_kabaloev_obem_rynka_tsfa_v_2025_godu_mozhet_prevysit_1_trln_rublei

43. Ayupov, A.A., & Badikova, A.R. (2021). Hybrid token as a promising financial instrument in the ICO market. Innovations and Investments, 1, 93-97.

44. Truntsevsky, Y.V., & Sevalnev, V.V. (2020). Smart contract: From definition to certainty. Law. Journal of the Higher School of Economics, 1, 118-147. https://doi.org/10.17323/2072-8166.2020.1.118.147

45. Sidorov, D.V. (2022). Features of conducting market analysis in the retrospective period when addressing the issue of suppressing violations of antimonopoly legislation. Russian Competition Law and Economics, 3(31), 30-37. https://doi.org/10.47361/2542-0259-2022-3-31-30-37

46. Zabelin, N.A. (2025). Prospects for the high-yield bond market. Scientific Notes of the Russian Academy of Entrepreneurship, 24(3), 18-23. https://doi.org/10.24182/2073-6258-2025-24-3-18-23

47. The impact of changes in central bank interest rates on financial markets: Key mechanisms and practical significance for asset managers. Moscow: National Research University "Higher School of Economics".

48. Metelsky, A.A. (2023). Improving the banking service system based on the digital transformation of financial technologies: Candidate of Economic Sciences dissertation.

49. Voronov, D.S., & Ramenskaya, L.A. (2023). Estimation of the cost of capital and the discount rate based on Russian financial statistics. Journal of New Economy, 24(1), 50-80. https://doi.org/10.29141/2658-5081-2023-24-1-3

First Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The subject of the study. Taking into account the formed title, the article should be devoted to methodological approaches to pricing and quantification of risks of digital financial assets in Russia. The author does not deviate from the stated topic. At the same time, the final part of the article does not provide an answer to this question, although separate elements are contained in the text of the article. The research methodology is based on the application of a set of methods (analysis, synthesis, graphical, systematic, etc.). It is valuable that the author has prepared tables and figures to confirm his judgments. However, it is also important to specify the data sources on the basis of which they were built (in accordance with the requirements for the design of graphic objects). The relevance of the research on issues related to pricing and quantification of risks of digital financial assets is beyond question. Indeed, they are currently in the focus of active attention of both scientific researchers and representatives of government authorities of the Russian Federation and the Bank of Russia. At the same time, the potential readership is interested in well-reasoned proposals for solving existing problems. The scientific novelty is partially present in the material submitted for review. For example, it may be related to a developed scoring model, as well as a set of measures to modernize CFA market regulation and evaluate their effectiveness, subject to their argumentation. Style, structure, and content. From the point of view of the lack of colloquial and journalistic expressions, the article is written in a scientific style. The structure of the article is formed correctly. The content of the article is generally structured according to the points of the structure, but, first, it is important to provide an answer to the question stated in the title of the article in the conclusion, as well as clarify a number of points to ensure that the article is in high demand among the potential readership. In table 5, the author presented a set of measures to modernize the regulation of the CFA market and assess their effectiveness. How were the numerical values indicated in the column calculated by the author? How do these calculations differ from those made by other authors using their models? The author also claims that the developed integrated risk scoring model (Rtotal) allows investors to quantify infrastructure risks. And in what way is the author's developed model better than those that already exist? Moreover, it would also be interesting to identify areas for further research, taking into account the results obtained and the areas of demand for a potential readership. Bibliography. The bibliographic list compiled by the author includes 40 sources. It is valuable that its content includes both domestic and foreign scientific publications. Appeal to the opponents. On the one hand, the text contains references to the works of the authors listed in the bibliographic list. On the other hand, the author does not discuss the results obtained with those already contained in them. Accordingly, when carrying out the revision, it is important to compare the research results reflected in the text of the article with those found in scientific articles by other authors from the prepared bibliographic list. Conclusions and interest for the readership. Taking into account the above, we conclude that the article can be published after making adjustments based on the comments indicated in the text of the review, since if they are eliminated qualitatively, it will be in demand from a wide readership.

Second Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The subject of the study. Based on the above headline, we draw a conclusion about the subject of the study – methodological approaches to pricing and quantification of risks of digital financial assets in Russia. However, in conclusion, the author concludes that "the place of digital financial assets in modern investment theory has been clarified." It is important to ensure that the sections of the article are synchronized with each other and the stated title. The author has chosen the research methodology quite extensively and includes both general scientific research methods and specifically tailored to the chosen subject. The graphic objects (tables, figures) formed by the author also form a positive impression, but the remark on the indication of the data sources used as the basis for their construction has not been given, despite the previously mentioned remark. It is important for a potential readership to see a well-designed article and be able to independently familiarize themselves with the data sources in order to assess the reliability of the study. The relevance of the research on the issues stated in the title is beyond doubt, as this topic area is of interest to a wide range of potential readers: from the scientific community to representatives of government authorities of the Russian Federation and the Bank of Russia. However, it is important to note that the materials in which the authors focus on the argumentation of proposals to solve the current problems are of primary interest. Speaking of scientific novelty, the most interesting are the matrix of risks of investing in digital financial assets, the scoring model, as well as the presented measures to modernize the regulation of the CFA market and assess their effectiveness. The author claims that they are "based on a hybrid calculation methodology that includes extrapolation of historical data from the high-yield bond market, scenario VaR modeling, and a method for transferring the value of real risk management tools." However, this is not presented in the text. Moreover, a link has been made to one of the sources in the bibliographic list. Style, structure, and content. The style of presentation is mostly scientific, but it is recommended to remove the use of the abbreviation "RF" from the text. The structure of the article is formed correctly. The author builds the content of the article according to the structure. When finalizing, it is important to strengthen the reasoning of the conclusions presented in Table 5, as well as answer the questions mentioned in the previous review (regarding the justification of the judgments given in the conclusion), and then the article will have a very wide demand. It is valuable that the author supplemented the article with directions for further research. Bibliography. The bibliographic list reflected at the end of the reviewed article includes 41 sources. A positive impression is formed by its breadth in terms of the presence of various thematic aspects related to the subject of the study. Appeal to the opponents. On the one hand, the text contains references to the works of the authors listed in the bibliographic list. On the other hand, the authors discussed the results obtained with those already contained in them. In this regard, it is possible to conclude that there is an appeal to the opponents. As a recommendation for the future, it is also valuable to show differences in quantitative estimates of the effects of implementing the author's recommendations. Conclusions and interest for the readership. First of all, we consider it important to note the high level of relevance of the research and the qualitative choice of methodology for its implementation. Taking into account the comments indicated in the text of the review will ensure that the substantive and organizational component of the article is brought to a level that ensures high demand from the potential readership.

Third Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.