|

Taxes and Taxation

Reference:

Avdeeva V.M.

Forms and methods of tax control of the application of corporate income tax preferences

// Taxes and Taxation.

2023. ą 6.

P. 1-7.

DOI: 10.7256/2454-065X.2023.6.69373 EDN: IIKRSO URL: https://en.nbpublish.com/library_read_article.php?id=69373

Forms and methods of tax control of the application of corporate income tax preferences

Avdeeva Valentina Mikhailovna

Postgraduate Student; Faculty of Taxes, Audit and Business Analysis; Financial University under the Government of the Russian Federation

125167, Russia, Moscow, Leningradsky Prospekt str., 49/2

|

valentinavdeeva1998@yandex.ru

|

|

|

Other publications by this author

|

|

|

DOI: 10.7256/2454-065X.2023.6.69373

EDN: IIKRSO

Received:

15-12-2023

Published:

22-12-2023

Abstract:

The control of the tax authorities over the correctness of the application of tax benefits and preferences aimed at supporting and stimulating various types of economic activity has a goal to put a barrier to possible abuses and fraud. In the process of implementing tax policy, attention should be paid to the analysis of the practice of applying and administering tax preferences established by tax legislation. The relevance of the research topic is determined by the need to determine the forms and methods of tax control for corporate income tax, within which the legality of the application of tax preferences is checked. The subject of the study is the tax control of the application of income tax preferences at the present stage of socio-economic development, as well as the transformation of forms and methods of tax control in the context of digitalization of the economy. The methodological basis of the study is the methodology of the system paradigm, the logical-epistemological method of cognition, the unity of structural and functional analysis of the problem. The methodological basis of the research is the ascent from the abstract to the concrete, the relationship between the general and the special, the dialectical and hypothetical research method, scientific abstraction and forecasting, analysis and synthesis, induction and deduction. As a result of the study, the methodology for conducting an on-site tax audit on income tax was determined, within the framework of which tax control measures are carried out to prevent abuse of preferences for this tax. The most popular trend of tax control is also identified - the digitalization of the work of tax authorities, which can lead to an increase in the number of tax revenues. In addition, in order to increase the effectiveness of tax control over the application of corporate income tax preferences, this article presents proposals regarding the rational and optimal management of income tax preferences, among which, for example, it is proposed to study the possibility of replacing some preferences with direct subsidies, which are subject to the budget control procedure, for budgetary transparency.

Keywords:

Tax control, corporate income tax, preferences, forms, methods, automated control system, tax audit, on-site tax audit, digitalization, digital economy

This article is automatically translated.

You can find original text of the article here.

Introduction Currently, not only individual organizations, but also the state as a whole, are doing a lot to understand the system of mechanisms for stimulating innovation and investment activities, but the reality is that the current regulatory framework does not contain specific norms that would allow the tax authorities to identify control tools in terms of tax control in the application of tax preferences profit of organizations. The gaps and inaccuracies in the current tax legislation, specifically in Article 82 of the Tax Code of the Russian Federation, are the fundamental reason for the distorted understanding of forms and methods of tax control, not only by tax authorities, but also by judicial authorities. A distorted understanding of the methods and forms of tax control, arising from gaps in the current tax legislation, contributes to the appearance of various types of inspections of taxpayers in the work of tax authorities, the procedure for which is not fixed by the current law. Nevertheless, courts quite often recognize the legality of their conduct and the legitimacy of collecting taxes and fees based on their results [2]. As an example, Ilyin A.Yu. [2] cites the verification of the procedure for fulfilling the obligation to pay tax. The Federal Antimonopoly Service of the West Siberian District says that this type of audit is one of the forms of tax control, which aims to establish good faith or dishonesty in the actions of a taxpayer in fulfilling the obligation to pay calculated amounts of taxes that have not been received by the budget. It is worth considering that a different understanding of the essence of this audit entails a violation of the interests of the state, since taxpayers who have abused the right provided for by current legislation (Article 45 of the Tax Code of the Russian Federation) actually evade taxes. Another form of tax control was named "control over the use of tax benefits" by the decision of the AC of the Chita region. On-site tax audit on corporate income tax Assessing the effectiveness of the activities of tax authorities primarily requires determining the effectiveness of tax control, which is predetermined by the relationship between the goals and consequences of tax control. On-site tax audit is one of the main and more effective forms of tax control, which is why it is most suitable for income tax control. Its basis is the study of objective and factual data, which are not always provided by taxpayers to the tax authorities in full. The main task of such a check is to make sure that the calculation is correct and taxes are paid on time. The result of the on-site tax audit is a conclusion about whether the taxpayer has tax debts to the state, and whether he uses illegal ways to reduce the tax burden, which subsequently entails additional tax charges, fees, fines in favor of the state. The interest of the tax authority, first of all, may be aroused if the inspectors have information that a legal entity uses tax avoidance schemes or other mandatory payments in its activities, that is, the activities of a single taxpayer in any way aroused the suspicions of the supervisory authority. If we talk about the stages of the audit, then, for example, Moseikin V.V. identifies four stages of conducting an on-site tax audit on income tax: the preparatory stage, conducting an audit, registration of audit materials and implementation of audit materials [4]. Kazimagomedova Z.A. in her work also addresses the stages of conducting an audit, highlighting the use of tax procedural actions of tax control and verification of separate divisions as separate stages of an on-site tax audit. From the point of view of the author of the study, the following stages of an on-site income tax audit can be distinguished: — Pre-test analysis. At this stage, it is necessary to determine the subject of the audit, that is, it is necessary to select taxpayers in respect of whom a tax audit will be conducted directly. In fact, this stage can be considered planning of tax control measures. — Conducting an on-site tax audit. Before the start of the inspection, the authorized person makes a decision on its conduct. This stage also includes the demand for documents, inventory, inspection, summoning as a witness, seizure, if necessary, it is also possible to involve an interpreter, or conduct an examination. The current legislation does not contain a list of documents that can be checked as part of an on-site tax audit. Based on practice, mostly auditors require constituent documents, tax returns, accounting statements, etc. In addition to the documents, the movement of funds on the taxpayer's current account is checked. Any actions and cash flows must be justified and confirmed by primary accounting documents. Clearly, special attention should be paid to checking the legitimacy of the application of tax preferences for income tax. — Registration of the results of the audit and making a decision on the taxpayer being audited. Upon completion of the audit, the tax authority must provide an act on the results of the audit, even if no violations could be detected. The registration of the audit results is one of the most important points, since the result of incorrect, incorrect registration of the audit results may be the inability to hold the person being checked accountable.

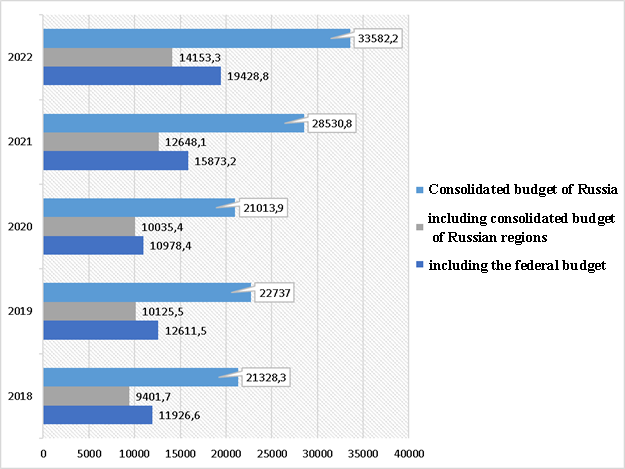

Summing up, we can identify several areas that require improving the methodology of such checks. This includes the improvement of the legislative framework of tax control, and professional development of employees, as well as the use of information technology in the framework of on-site income tax audits. The elaboration of these areas can significantly increase the effectiveness of income tax control, including in the field of control over the application of tax advantages and benefits for corporate income tax. Tax control of the application of corporate income tax preferences in modern conditions The modern world is in a state of drastic digital transformation, as well as in an environment where the need for large-scale and permanent economic and other innovations is increasing exponentially. Digital technologies play a key role here. The increasing role of scientific and technological progress in socio-economic progress is successfully reflected in modern economic theory.The development of the digital economy has led to a revision of the concept of tax administration, including tax control. If we talk about an earlier period, then, for example, in 2010, there was the introduction of informing individual taxpayers about the amounts of tax arrears through the Taxpayer's Personal Account, since 2011 – the creation of the Tax Service Federal Tax Service, as well as the creation of a Federal Information Address Resource (FIAS). In 2013, the launch of the pilot project ASK VAT-2 took place. The course taken by the Federal Tax Service of the Russian Federation is related to the implementation of dialogue interaction with taxpayers, the main principles of which are a risk-based approach, selectivity, creating conditions for achieving mutual benefit of the state and controlled entities, etc.[3]. According to the data presented in Figure 1, tax revenues to the consolidated budget of the Russian Federation in 2022 amounted to 3,3582.2 billion rubles, which is 117.7% compared to 2021. Due to the fact that 2022 was a record year for additional taxes and fees. But since the report of the Federal Tax Service of Russia reflects an increase in the number of inspections by 25%, but it also included inspections suspended due to the pandemic, it is advisable to compare the level of tax revenues for 2022 and the pre-pandemic level of 2018-2019 – this comparison demonstrates a trend of high revenue levels. The growth of tax revenues as a result of the introduction of information systems by the Federal Tax Service of the Russian Federation, which allowed to restore order with taxes, and today form the basis of tax administration.

Source: compiled by the author on the basis of statistical data from Rosstat Figure 1 - Dynamics of tax receipts, fees and other mandatory payments to the budget system of the Russian Federation in 2018-2022, billion rubles Today, tax authorities, implementing the functions of control and supervision over compliance with tax legislation, actively use software packages, interdepartmental information exchange, as well as a system for submitting tax and accounting reports in electronic form [1]. Of the greatest interest is the VAT-3 ASC, as well as the possibility of implementing an automated control system for the reimbursement of income tax, within which tax control over the application of tax preferences for NGOs is implemented. Value added tax – VAT, occupies a certain niche in the established automated tax control system. This is due to the fact that this tax is one of the most important elements of the formation of the federal budget of the Russian Federation, which occupies a leading position among tax revenues to the federal budget. The procedure for calculating corporate income tax raises the greatest number of questions when discussing the prospects for its algorithmization [6]. According to Sinelnikov-Murylev S.G., the transition to automated fulfillment of tax obligations is impossible without significant simplification and redesign of applied taxes. Taking into account the numerous practical problems arising from the complexity of calculating income tax, the scientific literature often suggests replacing this tax with consumption taxes, including various VAT changes, a cash flow tax, etc. [8]. However, all these proposals, by simplifying the taxation technique, distance the taxation of corporate profits from the taxation of "economic profits", thereby distorting the conditions of competition between companies with different levels of profitability. Conclusions Thus, the introduction of information technologies into the daily work of tax authorities and the gradual withdrawal of traditional forms of tax control into the background are among the trends in socio-economic development.The development of the digital platform of tax authorities has facilitated the simplification of taxpayers' understanding of taxation, made it more transparent and ensured equal competition for doing business. In addition, in order to ensure rational and optimal tax control over the application of income tax preferences, it is necessary to limit the duration of the provision and application of each tax benefit and conduct an assessment at the end to ensure their effectiveness in relation to the goals expected at the time of their introduction, and subsequently decide whether to resume or cancel them. Also, in order to ensure budgetary transparency, to explore the possibility of replacing some preferences with direct subsidies, which are subject to the budget control procedure.

References

1. Vishnevsky, V.P. (2019). Digital economy in the conditions of the fourth industrial revolution: opportunities and limitations. Bulletin of St. Petersburg University. Series: Economics, 4, 606-627.

2. Ilyin, A. Yu. (2014) Legal content of types, forms and methods of tax control. Financial law, 1, 28-34.

3. Molchanov, E. G. (2019). Innovative tools of tax administration in the context of the “Digital Economy in the Russian Federation” program. Accounting and statistics, 3(55), 55-64.

4. Moseykin, V.V. (2006). On-site tax audit on corporate income tax: main stages, procedures and related problems. Bulletin of Omsk State University. Series: Economics, 3.

5. Sekushin, A. Yu. (2021). Digitalization and tax control: the experience of foreign administrations and the possibilities of its implementation in Russia, 3, 26-38.

6. Sinelnikov-Murylev, S. G. (2022). Digitalization of tax administration in Russia: opportunities and risks. Economic policy, 2, 8-33.

7. Sinenko, O. A. (2020). Tax risks in the context of digitalization of the economy. Asia-Pacific region: economics, politics, law, 3, 15-32.

8. Carton, B., Corugedo, E. F., & Hunt, M. B. L. Corporate Tax Reform: From Income to Cash Flow Taxes. IMF Working Paper. WP/19/13. 201.

Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The reviewed article is devoted to the study of forms and methods of tax control of the application of corporate income tax preferences. The methodology of the study is based on the analysis of official state statistics data on the receipts of taxes and fees to the budget system of the Russian Federation over the past five years, visualization of the results of the analysis. The authors rightly attribute the relevance of the work to the fact that the current regulatory framework does not contain specific norms that would allow the tax authorities to identify control tools in terms of tax control in the field of application of corporate income tax preferences. The scientific novelty of the reviewed study consists in the conclusions that in order to rationalize the application of income tax preferences, it is necessary to limit the duration of the provision and application of each tax benefit and conduct an assessment to ensure their effectiveness in relation to the goals expected at the time of their introduction, and subsequently decide on their resumption or cancellation. Structurally, the following sections are highlighted in the article: Introduction, On-site tax audit on corporate income tax, Tax control of the application of corporate income tax preferences in modern conditions, Conclusions, Bibliography. In the publication, the authors proceed from the fact that checking the procedure for fulfilling the obligation to pay tax is one of the forms of tax control, which aims to establish good faith or bad faith in the actions of a taxpayer in fulfilling the obligation to pay calculated amounts of taxes that have not been received by the budget, believing that a different understanding of the essence of this check entails a violation of the interests of the state. The publication highlights the following stages of an on-site tax audit on income tax: pre-verification analysis, conducting an on-site tax audit, processing the results of the audit and making a decision on the taxpayer being audited; the main features of the work at each stage are outlined. The article notes that the development of the digital economy has led to a revision of the concept of tax administration, including tax control. The authors conclude that the introduction of information technologies into the work of tax authorities and the gradual departure of traditional forms of tax control are one of the trends in improving financial control, and also believe that the development of the digital platform of tax authorities has facilitated taxpayers' understanding of taxation, made it more transparent and ensured equal competition for doing business. The bibliographic list includes 8 sources – scientific publications of domestic and foreign authors on the topic under consideration. The text contains targeted references to bibliographic sources, which confirms the existence of an appeal to opponents. Among the shortcomings that need to be eliminated, it should be noted the presence of inconsistent phrases and missing words in sentences. The reviewed material corresponds to the direction of the journal "Taxes and Taxation", reflects the results of the work carried out by the authors, contains elements of scientific novelty and practical significance, may arouse interest among readers, and is recommended for publication taking into account the comments made.

|

Eng

Eng