|

Taxes and Taxation

Reference:

Loginova T.A., Milogolov N.S.

Analysis of Distorting Economic Effects Created as a Result of VAT Neutrality Detoriation (Based on the Example of Applying the Reduced Rates for Food Products)

// Taxes and Taxation.

2017. ą 12.

P. 1-9.

DOI: 10.7256/2454-065X.2017.12.24956 URL: https://en.nbpublish.com/library_read_article.php?id=24956

Analysis of Distorting Economic Effects Created as a Result of VAT Neutrality Detoriation (Based on the Example of Applying the Reduced Rates for Food Products)

Loginova Tatiana Aleksandrovna

PhD in Economics

Senior researcher of Tax Policy Centre of the Financial research Institute of the Ministry of finance of the Russian Federation

127006, Russia, g. Moscow, per. Nastas'inskii, 3, stroenie 2

|

nifi.loginova@gmail.com

|

|

|

Other publications by this author

|

|

|

Milogolov Nikolai Sergeevich

PhD in Economics

senior lecturer at Center for Tax Policy of the Financial Research Institute of the Ministry of Finance of the Russian Federation

127006, Russia, Moscow, str. Nastas'inski pereulok, 3, bld. 2

|

|

nmilogolov@nifi.ru

|

|

|

Other publications by this author

|

|

|

DOI: 10.7256/2454-065X.2017.12.24956

Received:

11-12-2017

Published:

21-12-2017

Abstract:

The object of the research is the mechanism of collection and calculation of the VAT taxable base and economic effects created as a result of selecting particular elements of this tax. The subject of the research is the taxation of food products in the process of their disposal and use of certain VAT exemptions. The authors of the article examine effects that arise as a result of implementing reduced rates established for operations with food products. The authors pay special attention to the analysis of the distribution effect as a result of applying the reduced VAT rate established in the process of disposal of food products between households with different levels of prosperity. The methodological basis of the research is the applicable Russian Federation law about taxes and levies, in particular, VAT tax, as well as official statistical data provided by the Federal Tax Service and Russian Federal State Statistics Service. The following research methods have been used by the authors in the course of their research: observation, analysis and summarisation. As a result of their research, the authors have discovered inefficiency of the VAT reduced tax rate for certain groups of food products established for the purpose of supporting indigent groups of taxpayers. The authors' special contribution to the research of the topic is that they prove the need to refuse from the established VAT rebate in the form of reduced tax rates for food products. The novelty of the research is caused by the fact that the authors offer a set of compensation measures in the event of refusal from the aforesaid VAT rebate as well as develop general principles of tax policy aimed at minimisation of distoring economic effects from VAT.

Keywords:

value added tax, supply of goods, lower rate, subsidies, tax benefits, budget revenue, tax policy, taxpayer’s revenue, supply of food, tax burden

This article written in Russian. You can find original text of the article here

.

Ôóíäŕěĺíňŕëüíîé ÷ĺđňîé íŕëîăŕ íŕ äîáŕâëĺííóţ ńňîčěîńňü (äŕëĺĺ – ÍÄŃ) ˙âë˙ĺňń˙ ĺăî íĺéňđŕëüíîńňü ďî îňíîřĺíčţ ę áčçíĺńó. ÍÄŃ óńňđîĺí ňŕęčě îáđŕçîě, ÷ňî ýęîíîěč÷ĺńęîĺ áđĺě˙ íŕëîăŕ ďĺđĺíîńčňń˙ íŕ ęîíĺ÷íîăî ďîňđĺáčňĺë˙, ŕ áčçíĺń âűńňóďŕĺň â ýęîíîěč÷ĺńęîé đîëč ŕăĺíňŕ, ďĺđĺ÷čńë˙ţůĺăî íŕëîă â áţäćĺň ďđîďîđöčîíŕëüíî äîëč ńîçäŕâŕĺěîé čě ńňîčěîńňč. Ďđč ýňîě ňĺîđĺňč÷ĺńęč ďîëíîńňüţ íĺéňđŕëüíűě ˙âë˙ĺňń˙ ÍÄŃ, âçčěŕĺěűé ń ěŕęńčěŕëüíî řčđîęîé áŕçű ń ďđčěĺíĺíčĺě ĺäčíîé ńňŕâęč č íĺ ńîäĺđćŕůčé îńâîáîćäĺíčé îň íŕëîăîîáëîćĺíč˙.

đĺŕëüíîńňč ćĺ ňîň ÍÄŃ, äĺéńňâóţůčé â Đîńńčč â ńîîňâĺňńňâčč ń ďîëîćĺíč˙ěč Ăëŕâű 21 ÍĘ ĐÔ, ńîäĺđćčň ěíîćĺńňâî čçú˙ňčé čç ýňîé ňĺîđĺňč÷ĺńęč íĺéňđŕëüíîé ěîäĺëč. Ýňč čçú˙ňč˙ ńâ˙çŕíű, ďđĺćäĺ âńĺăî, ń íŕëč÷čĺě ěíîćĺńňâŕ îńâîáîćäĺíčé â ńîîňâĺňńňâčč ńî ńňŕňüĺé 149 ÍĘ ĐÔ, ń ďđčěĺíĺíčĺě ďîíčćĺííîé ńňŕâęč ďî ÍÄŃ â đŕçěĺđĺ 10%, ń âçŕčěîäĺéńňâčĺě ęîěďŕíčé, ˙âë˙ţůčőń˙ íŕëîăîďëŕňĺëüůčęŕěč ÍÄŃ č ęîěďŕíčé, ďđčěĺí˙ţůčő óďđîůĺííóţ ńčńňĺěó íŕëîăîîáëîćĺíč˙. Ęđîěĺ ňîăî, íŕđóřĺíčĺ íĺéňđŕëüíîńňč ÍÄŃ âîçíčęŕĺň ďđč ěĺćäóíŕđîäíîé ňîđăîâëĺ, â ÷ŕńňíîńňč, â ńâ˙çč ń ďđčěĺíĺíčĺě ďđŕâčë îďđĺäĺëĺíč˙ ěĺńňŕ đĺŕëčçŕöčč óńëóă, â ńâ˙çč ń îńîáĺííîńň˙ěč íŕëîăîîáëîćĺíč˙ ěĺćäóíŕđîäíîé ňîđăîâëč ÷ĺđĺç ęîěčńńčîíĺđŕ. Ňŕęćĺ íŕđóřŕĺňń˙ íĺéňđŕëüíîńňü ÍÄŃ ďđč âçŕčěîäĺéńňâčč íŕëîăîďëŕňĺëüůčęŕ íŕ óďđîůĺííîé ńčńňĺěĺ íŕëîăîîáëîćĺíč˙ (ÓŃÍ) č îáůĺé ńčńňĺěĺ íŕëîăîîáëîćĺíč˙ (ÎŃÍ).

đĺçóëüňŕňĺ â äŕííűő ńčňóŕöč˙ő, ďîäđîáíî đŕńńěîňđĺííűő íčćĺ, íĺéňđŕëüíîńňü ÍÄŃ íŕđóřŕĺňń˙, ÷ňî ďđčâîäčň ę ňîěó, ÷ňî čńęŕćŕĺňń˙ ęîíęóđĺíöč˙ ďî ďđč÷číĺ âîçíčęíîâĺíč˙ äâîéíîăî íŕëîăîîáëîćĺíč˙ č äâîéíîăî íĺîáëîćĺíč˙, ŕ ňŕęćĺ ďî ďđč÷číĺ îňńóňńňâč˙ ďđŕâŕ íŕ âű÷ĺň âőîä˙ůĺăî íŕëîăŕ. Ęđîěĺ ňîăî, âîçíčęŕţň íĺîäíîçíŕ÷íűĺ ďîńëĺäńňâč˙ äë˙ áţäćĺňŕ č âîçěîćíîńňč äë˙ íŕëîăîďëŕňĺëüůčęîâ ńňđóęňóđčđîâŕňü ńâîţ äĺ˙ňĺëüíîńňü ňŕęčě îáđŕçîě, ÷ňîáű óęëîí˙ňüń˙ îň íŕëîăîîáëîćĺíč˙ ÍÄŃ. Äĺéńňâóţůĺĺ çŕęîíîäŕňĺëüńňâî î íŕëîăŕő č ńáîđŕő â ÷ŕńňč óńňŕíîâëĺíč˙ íŕëîăŕ íŕ äîáŕâëĺííóţ ńňîčěîńňü ďđĺäóńěŕňđčâŕĺň âîçěîćíîńňü ďđčěĺíĺíč˙ íĺńęîëüęčő íŕëîăîâűő ńňŕâîę.

Ďđîáëĺěű íŕđóřĺíč˙ íĺéňđŕëüíîńňč ÍÄŃ. Ńîăëŕńíî ďîëîćĺíč˙ě ńň. 164 Íŕëîăîâîăî ęîäĺęńŕ Đîńńčéńęîé Ôĺäĺđŕöčč îáůŕ˙ ńňŕâęŕ ÍÄŃ ńîńňŕâë˙ĺň 18 %. Ýňŕ ńňŕâęŕ íŕëîăŕ ďđčěĺí˙ĺňń˙ ďđč íŕëîăîîáëîćĺíčč đĺŕëčçŕöčč áîëüřčíńňâŕ ňîâŕđîâ (đŕáîň, óńëóă). Íŕđ˙äó ń ýňčě, óńňŕíîâëĺíű č ďîíčćĺííűĺ ńňŕâęč íŕëîăŕ äë˙ îďđĺäĺëĺííűő ăđóďď ňîâŕđîâ.  ÷ŕńňíîńňč, áîëĺĺ íčçęŕ˙ ńňŕâęŕ ÍÄŃ â đŕçěĺđĺ 10 % óńňŕíîâëĺíŕ äë˙ îďđĺäĺëĺííűő ăđóďď ňîâŕđîâ, óęŕçŕííűő â óňâĺđćäĺííűő Ďđŕâčňĺëüńňâîě Đîńńčéńęîé Ôĺäĺđŕöčč ďĺđĺ÷í˙ő. Ę ňŕęčě ňîâŕđŕě îňíĺńĺíű: ďđîäîâîëüńňâĺííűĺ ňîâŕđű, äĺňńęčĺ ňîâŕđű, ďĺđčîäč÷ĺńęčĺ ďĺ÷ŕňíűĺ čçäŕíč˙, ěĺäčöčíńęčĺ ňîâŕđű, ňî ĺńňü ńîöčŕëüíî çíŕ÷čěűĺ ňîâŕđű. Ňŕęčě îáđŕçîě, ďîńđĺäńňâîě ńęđűňîé ďîä ďîíčćĺííîé ńňŕâęîé ÍÄŃ ńóáńčäčč ăîńóäŕđńňâî ďđĺäîńňŕâë˙ĺň áĺäíĺéřĺé ÷ŕńňč íŕńĺëĺíč˙ âîçěîćíîńňü ďđčîáđĺňŕňü áîëüřĺĺ ęîëč÷ĺńňâî ďđîäóęňîâ ďčňŕíč˙ çŕ ń÷ĺň.

Ęđîěĺ ňîăî, â öĺë˙ő îęŕçŕíč˙ ńîöčŕëüíîé ďîääĺđćęč çŕ ń÷ĺň ńíčćĺíč˙ íŕëîăîâîé íŕăđóçęč ďî ÍÄŃ ďîëîćĺíč˙ěč ď.2 č ď.3 ńň. 149 ÍĘ ĐÔ óńňŕíîâëĺíî îńâîáîćäĺíčĺ íĺęîňîđűő ăđóďď ňîâŕđîâ č óńëóă. Ę ýňčě ňîâŕđŕě č óńëóăŕě îňíĺńĺíű: ěĺäčöčíńęčĺ ňîâŕđű č óńëóăč, óńëóăč ďî ďđčńěîňđó çŕ äĺňüěč (ďđîäëĺíęŕ, ęđóćęč č ńĺęöčč), óńëóăč ďî óőîäó çŕ ďîćčëűěč č číâŕëčäŕěč, đĺŕëčçŕöč˙ ďčňŕíč˙ řęîëüíűěč ńňîëîâűěč, óńëóăč ďî ďĺđĺâîçęĺ ďŕńńŕćčđîâ, đčňóŕëüíűĺ óńëóăč, óńëóăč ďî îáđŕçîâŕíčţ, óńëóă ďî ňĺőíč÷ĺńęîěó îńěîňđó, óńëóă â ńôĺđĺ ęóëüňóđű č čńęóńńňâŕ, đĺŕëčçŕöč˙ ęčíîďđîäóęöčč, đĺŕëčçŕöč˙ čńęëţ÷čňĺëüíűő ďđŕâ íŕ čçîáđĺňĺíč˙, íîó-őŕó č íŕ čńďîëüçîâŕíčĺ číňĺëëĺęňóŕëüíîé ńîáńňâĺííîńňč, đĺŕëčçŕöč˙ áčëĺňîâ íŕ ńďîđňčâíűĺ ěĺđîďđč˙ňč˙, îęŕçŕíčĺ óńëóă ŕäâîęŕňŕěč, đĺŕëčçŕöč˙ óńëóă îçäîđîâčňĺëüíűő îđăŕíčçŕöčé, îôîđěë˙ĺěűő áëŕíęŕěč ńňđîăîé îň÷ĺňíîńňč, ďđîäŕćŕ đĺëčăčîçíîé ëčňĺđŕňóđű č čçäĺëčé íŕđîäíűő ďđîěűńëîâ č äđ. [1].

Îäíŕęî ďđŕęňčęŕ ďđčěĺíĺíč˙ ďîíčćĺííűő ńňŕâîę ÍÄŃ č íŕëîăîâűő ëüăîň â âčäĺ îńâîáîćäĺíčé äë˙ îďđĺäĺëĺííűő âčäîâ íŕëîăîîáëŕăŕĺěîé äĺ˙ňĺëüíîńňč ńâčäĺňĺëüńňâóĺň î íĺýôôĺęňčâíîńňč äŕííîăî ěĺőŕíčçěŕ äë˙ äîńňčćĺíč˙ çŕäŕ÷č ńîöčŕëüíîé ďîääĺđćęč íŕńĺëĺíč˙ ďî ńëĺäóţůčě ďđč÷číŕě. Âî-ďĺđâűő, ńęđűňŕ˙ ńóáńčäč˙ â âčäĺ áîëĺĺ íčçęčő öĺí íŕ îďđĺäĺëĺííűĺ ňîâŕđű č óńëóăč đŕńďđĺäĺë˙ĺňń˙ íĺ ňîëüęî íóćäŕţůčěń˙ â íĺé, íî č ďđî÷čě ëčöŕě. Âî-âňîđűő, ýęîíîěč÷ĺńęóţ âűăîäó îň íŕëč÷č˙ ëüăîňű ďîëó÷ŕţň íĺ ňîëüęî ďîęóďŕňĺëč, íî č ďđîäŕâöű ëüăîňčđóĺěűő ňîâŕđîâ č óńëóă, ďđč ňîě, ÷ňî ÍÄŃ ˙âë˙ĺňń˙ íĺéňđŕëüíűě äë˙ ďđîäŕâöŕ íŕëîăîě, áđĺě˙ ęîňîđîăî ďđč îňńóňńňâčč ëüăîňű ďĺđĺíîńčňń˙ íŕ ďîęóďŕňĺë˙.  đĺçóëüňŕňĺ ćĺ ďđčěĺíĺíč˙ ëüăîňű đűíî÷íîĺ đŕâíîâĺńčĺ ńďđîńŕ č ďđĺäëîćĺíčĺ čńęŕćŕĺňń˙, č ďđîäŕâĺö ëüăîňčđóĺěîé ďđîäóęöčč ďîëó÷ŕĺň íĺîáîńíîâŕííîĺ ęîíęóđĺíňíîĺ ďđĺčěóůĺńňâî â âčäĺ áîëĺĺ íčçęîé öĺíű íŕ ńâîţ ďđîäóęöčţ. Đŕńńěîňđčě áîëĺĺ äĺňŕëüíî äŕííűĺ ďđîáëĺěű íŕ ďđčěĺđŕő ďđčěĺíĺíč˙ ďîíčćĺííîé ńňŕâęč ďî ÍÄŃ č îńâîáîćäĺíč˙ îň ÍÄŃ.

Ďîíčćĺííŕ˙ ńňŕâęŕ ÍÄŃ (10 %). Ďîńęîëüęó ÍÄŃ ýęîíîěč÷ĺńęč ˙âë˙ĺňń˙ íŕëîăîě íŕ ďîňđĺáëĺíčĺ ń řčđîęîé áŕçîé, ňî äîńňóď ę ňîâŕđŕě č óńëóăŕě, îáëŕăŕĺěűě ďî ďîíčćĺííîé ńňŕâęĺ â đŕçěĺđĺ 10 %, čěĺţň íĺ ňîëüęî ńîöčŕëüíî íĺçŕůčůĺííűĺ, íî č äđóăčĺ ëčöŕ. Ďđč ýňîě â ńňđóęňóđĺ ďîňđĺáëĺíč˙ áîëĺĺ áîăŕňűő ăđŕćäŕí äîë˙ ëüăîňíűő ňîâŕđîâ č óńëóă ńîńňŕâë˙ĺň â ŕáńîëţňíîě çíŕ÷ĺíčč äŕćĺ áîëüřóţ âĺëč÷číó â ńčëó ňîăî, ÷ňî îíč áîëüřĺ ďîňđĺáë˙ţň â ŕáńîëţňíîě âűđŕćĺíčč.

Ýňî îňíîńčňń˙ ęî âńĺě ňîâŕđŕě č óńëóăŕě, ę ęîňîđűě â ńîîňâĺňńňâčč ń ď.2 ńň. 164 ÍĘ ĐÔ ďđčěĺí˙ţňń˙ ďîíčćĺííŕ˙ ńňŕâęŕ íŕëîăŕ â đŕçěĺđĺ 10%. Ýňî îďĺđŕöčč ďî đĺŕëčçŕöčč áîëüřîăî ŕńńîđňčěĺíňŕ ďđîäîâîëüńňâĺííűő ňîâŕđîâ, ňîâŕđîâ äë˙ äĺňĺé, ęíčă, ëĺęŕđńňâ č ěĺäčöčíńęčő čçäĺëčé çŕ čńęëţ÷ĺíčĺě ćčçíĺííî íĺîáőîäčěűő, óńëóă ďî âíóňđĺííčě âîçäóříűě ďĺđĺâîçęŕě ďŕńńŕćčđîâ č áŕăŕćŕ, ŕ ňŕęćĺ óńëóă ďî ďĺđĺâîçęŕě ďŕńńŕćčđîâ č áŕăŕćŕ ćĺëĺçíîäîđîćíűě ňđŕíńďîđňîě äŕëüíĺăî ńîîáůĺíč˙. Ňŕęčě îáđŕçîě, ďîńđĺäńňâîě ńíčćĺíč˙ íŕëîăîâîé íŕăđóçęč íŕ ýňč îďĺđŕöčč ăîńóäŕđńňâî ďđĺäîńňŕâë˙ĺň ńęđűňóţ ńóáńčäčţ â đŕçěĺđĺ đŕçíčöű ěĺćäó ńňŕíäŕđňíîé ńňŕâęîé íŕëîăŕ â đŕçěĺđĺ 18 % č ďîíčćĺííîé ńňŕâęîé â đŕçěĺđĺ 10 %. Ńëĺäóĺň îňěĺňčňü, ÷ňî ďîëó÷ĺííŕ˙ â đĺçóëüňŕňĺ âĺëč÷číŕ äĺëčňń˙ ěĺćäó ďđîäŕâöŕěč ýňčő ňîâŕđîâ č óńëóă (ďîëó÷ŕţůčěč ęîíęóđĺíňíîĺ ďđĺčěóůĺńňâî â âčäĺ áîëĺĺ íčçęčő öĺí), íóćäŕţůčěčń˙ č íĺ íóćäŕţůčěčń˙ ďîňđĺáčňĺë˙ěč. Ďđč ýňîě äîë˙ âűăîäű íóćäŕţůčőń˙ ďîňđĺáčňĺëĺé íŕčěĺíüřŕ˙ čç ňđĺő ďîëó÷ŕňĺëĺé ńóáńčäčč. Ňî ĺńňü ěĺőŕíčçě ńíčćĺíč˙ íŕëîăîâîé íŕăđóçęč ďî ÍÄŃ â âčäĺ óńňŕíîâëĺíč˙ ďîíčćĺííîé ńňŕâęč íŕëîăŕ ďî ńóňč ďđčâîäčň ę đĺăđĺńńčâíîěó íŕëîăîîáëîćĺíčţ, ęîăäŕ áîëĺĺ áîăŕňűĺ ďëŕň˙ň ďîëó÷ŕţň áîëüřĺĺ ęîëč÷ĺńňâî íŕëîăîâűő ëüăîň, ÷ĺě ěĺíĺĺ áîăŕňűĺ, ÷ňî ďđîňčâîđĺ÷čň čäĺĺ ńďđŕâĺäëčâîăî ďĺđĺđŕńďđĺäĺëĺíč˙ ńđĺäńňâ č áîđüáű ń íĺđŕâĺíńňâîě ń ďîěîůüţ ôčíŕíńîâîé ńčńňĺěű.

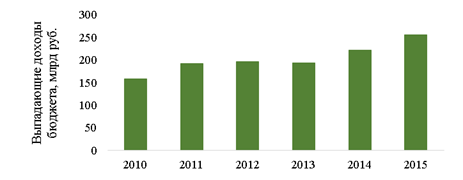

Âĺëč÷číŕ âűďŕäŕţůčő äîőîäîâ áţäćĺňŕ â đĺçóëüňŕňĺ ďđčěĺíĺíč˙ ďîíčćĺííîé ńňŕâęč ÍÄŃ â đŕçěĺđĺ 10 % ďîńňĺďĺííî óâĺëč÷čâŕĺňń˙ (ńě. đčńóíîę 1). Ďî ďîńëĺäíčě čěĺţůčěń˙ äŕííűě ńóěěŕ íĺďîńňóďëĺíčé ÍÄŃ â áţäćĺň â ńâ˙çč ń ýňîé ëüăîňîé â 2015 ă. ńîńňŕâčëŕ 255 ěëđä đóá. [2].

Đčńóíîę 1 – Âűďŕäŕţůčĺ äîőîäű áţäćĺňŕ îň ďđčěĺíĺíč˙ ďîíčćĺííîé ńňŕâęč ÍÄŃ ďđč đĺŕëčçŕöčč îďđĺäĺëĺííűő ďđîčçâîäńňâĺííűő ňîâŕđîâ

Čńňî÷íčę: ńîńňŕâëĺíî ŕâňîđŕěč íŕ îńíîâĺ äŕííűő Öĺíňđŕ ńňđŕňĺăč÷ĺńęčő đŕçđŕáîňîę [Ýëĺęňđîííűé đĺńóđń] – Đĺćčě äîńňóďŕ: https://www.csr.ru/

Îńâîáîćäĺíčĺ îň ÍÄŃ. Ďîńęîëüęó ÍÄŃ ýęîíîěč÷ĺńęč ˙âë˙ĺňń˙ íŕëîăîě íŕ ďîňđĺáëĺíčĺ ń řčđîęîé áŕçîé, ňî äîńňóď ę ňîâŕđŕě č óńëóăŕě, îńâîáîćäĺííűě îň íŕëîăîîáëîćĺíč˙ ÍÄŃ, ŕ, ńëĺäîâŕňĺëüíî, ę ńęđűňîé ńóáńčäčč čç áţäćĺňŕ ňŕęćĺ čěĺţň ęŕę íóćäŕţůčĺń˙, ňŕę č íĺ íóćäŕţůčĺń˙ â ĺĺ ďîëó÷ĺíčč ëčöŕ. Ďđč ýňîě äîë˙ ńęđűňîé ńóáńčäčč, ďîëó÷ŕĺěîé íĺ íóćäŕţůčěčń˙ â ńîöčŕëüíűő ňđŕíńôĺđňŕő íŕëîăîďëŕňĺëüůčęŕěč óńëóă áîëüřĺ, âńëĺäńňâčĺ čő áîëüřčő â ŕáńîëţňíîě âűđŕćĺíčč đŕńőîäîâ íŕ ďîňđĺáëĺíčĺ. Ęđîěĺ ňîăî, âűăîäó â âčäĺ áîëĺĺ řčđîęîăî ńďđîńŕ ńî ńňîđîíű íŕńĺëĺíč˙ âńëĺäńňâčĺ óńňŕíîâëĺíč˙ öĺí, íĺ âęëţ÷ŕţůčő â ńĺá˙, ÍÄŃ ďîëó÷ŕţň îđăŕíčçŕöčč, îęŕçűâŕţůčĺ ýňč âčäű óńëóă. Íŕčáîëĺĺ ˙đęčé ďđčěĺđ ýňîăî ńâ˙çŕí ń îńâîáîćäĺíčĺě ěĺäčöčíńęčő č îáđŕçîâŕňĺëüíűő óńëóă. Ňŕę, áîëĺĺ ńîńňî˙ňĺëüíűĺ ăđŕćäŕíĺ íĺńóň áîëüřčĺ ôčíŕíńîâűĺ çŕňđŕňű íŕ ńâîĺ îáó÷ĺíčĺ č îáđŕçîâŕíčĺ ńâîčő äĺňĺé, ŕ ňŕęćĺ íŕ ďîňđĺáëĺíčĺ ěĺäčöčíńęčő óńëóă. Ńëĺäóĺň îňěĺňčňü, ÷ňî âűńîęčé óđîâĺíü čő ěŕňĺđčŕëüíîăî áëŕăîńîńňî˙íč˙ ďîçâîë˙ĺň čě ďîëüçîâŕňüń˙ áîëĺĺ äîđîăîńňî˙ůčěč óńëóăŕěč, ďđĺäîńňŕâë˙ĺěűěč ÷ŕńňíűěč îáđŕçîâŕňĺëüíűěč č ěĺäčöčíńęčěč îđăŕíčçŕöč˙ěč, ÷ňî ôŕęňč÷ĺńęč äĺëŕĺň ýňčő ëčö íĺ íóćäŕţůčěčń˙ â ďđĺäîńňŕâë˙ĺěîé čě ăîńóäŕđńňâĺííîé ńóáńčäčč.

Ňŕęčě îáđŕçîě, ďđĺäńňŕâë˙ĺňń˙ íĺîáőîäčěűě äĺňŕëüíŕ˙ číâĺíňŕđčçŕöč˙ ęŕę îďĺđŕöčé, îńâîáîćäŕĺěűő îň ÍÄŃ â ńîîňâĺňńňâčč ń ď.2 č ď.3 ńň. 149 ÍĘ ĐÔ, ňŕę č îďĺđŕöčé, ę ęîňîđűě ďđčěĺí˙ţňń˙ ďîíčćĺííŕ˙ ńňŕâęŕ ďî ÍÄŃ â đŕçěĺđĺ 10 % â ńîîňâĺňńňâčč ń ď.2 ńň. 164 ÍĘ ĐÔ ń öĺëüţ ńîőđŕíĺíč˙ ňîëüęî ňĺő îńâîáîćäĺíčé, ęîňîđűĺ âőîä˙ň â áŕçîâóţ ńňđóęňóđó íŕëîăŕ íŕ äîáŕâëĺííóţ ńňîčěîńňü č ńîîňâĺňńňâóţň ëó÷řĺěó ěĺćäóíŕđîäíîěó îďűňó (íŕďđčěĺđ, îńâîáîćäĺíčĺ ôčíŕíńîâűő óńëóă čëč ďđîäŕćč ęâŕđňčđ) čëč ęîňîđűĺ ńďĺöčŕëüíűě îáđŕçîě ââĺäĺíű äë˙ đĺŕëčçŕöčč ăîńóäŕđńňâĺííűő ďđîăđŕěě č ďđîĺęňîâ (íŕďđčěĺđ, îńâîáîćäĺíčĺ ńňđîčňĺëüńňâŕ ćčëü˙ äë˙ âîĺííîńëóćŕůčő, čëč îďđĺäĺëĺííűő đŕáîň â ďîđňîâűő îńîáűő ýęîíîěč÷ĺńęčő çîíŕő). Ďđč ýňîě äë˙ đĺŕëčçŕöčč ńîöčŕëüíîé çŕäŕ÷č ďîääĺđćęč íŕńĺëĺíč˙ öĺëĺńîîáđŕçíî čńďîëüçîâŕňü äđóăčĺ ôčíŕíńîâűĺ ěĺőŕíčçěű, íŕďđčěĺđ, ŕäđĺńíűĺ ëüăîňű č ďđ˙ěűĺ ňđŕíńôĺđňű čç áţäćĺňŕ. Ýňî, âî-ďĺđâűő, ďîçâîëčň ďîâűńčňü ďđîăđĺńńčâíîńňü íŕëîăîîáëîćĺíč˙ čëč, ďî ęđŕéíĺ ěĺđĺ, îňęŕçŕňüń˙ îň äĺéńňâóţůĺé đĺăđĺńńčâíîé ńčńňĺěű. Âî-âňîđűő, ěčíčěčçčđóĺň čńęŕćĺíčĺ đűíî÷íîăî, íŕčáîëĺĺ îďňčěŕëüíîăî đŕńďđĺäĺëĺíč˙ ńďđîńŕ č ďđĺäëîćĺíč˙ íŕ ňîâŕđű č óńëóăč, ďđîäŕâöű ęîňîđűő ńĺăîäí˙ čěĺţň íĺîáîńíîâŕííîĺ ęîíęóđĺíňíîĺ ďđĺčěóůĺńňâî ďĺđĺä ďđîäŕâöŕěč ňîâŕđîâ č óńëóă, îáëŕăŕĺěűő ÍÄŃ ďî îáůĺé ńňŕâęĺ.

Âëč˙íčĺ ëüăîňű ďî ÍÄŃ íŕ íŕëîăîâóţ ńčńňĺěó (ďîěčěî ńîęđŕůĺíč˙ íŕëîăîâűő ďîńňóďëĺíčé). Ëüăîňŕ ďî íŕëîăó íŕ äîáŕâëĺííóţ ńňîčěîńňü â âčäĺ ďîíčćĺííîé ńňŕâęč íŕëîăŕ ďđčâîäčň ę ńëĺäóţůčě ýôôĺęňŕě â ęîíňĺęńňĺ äĺéńňâóţůĺé íŕëîăîâîé ńčńňĺěű.

1) Ďđčěĺíĺíčĺ ďîíčćĺííîé íŕëîăîâîé ńňŕâęč â đŕçěĺđĺ 10 % ňđĺáóĺň îň íŕëîăîďëŕňĺëüůčęîâ âĺńňč đŕçäĺëüíűé ó÷ĺň íŕëîăîâîé áŕçű ďî ÍÄŃ ďî îďĺđŕöč˙ě, îáëŕăŕĺěűě ďî ďîíčćĺííîé ńňŕâęĺ č ďî ńňŕíäŕđňíîé ńňŕâęĺ, ÷ňî ďîâűřŕĺň ŕäěčíčńňđŕňčâíűĺ čçäĺđćęč.

2) Ďîíčćĺííŕ˙ ńňŕâęŕ 10 % ďđčěĺí˙ĺňń˙ íĺ ęî âńĺě ďđîäóęňŕě ďčňŕíč˙, ŕ ňîëüęî ę ďĺđĺ÷čńëĺííűě â ďď. 1 ď. 2 ńň. 164 ÍĘ ĐÔ.  ńâ˙çč ń ýňčě íŕ íŕëîăîâűĺ îđăŕíű č íŕëîăîďëŕňĺëüůčęîâ ëîćčňń˙ äîďîëíčňĺëüíŕ˙ ŕäěčíčńňđŕňčâíŕ˙ íŕăđóçęŕ, ńâ˙çŕííŕ˙ ń íĺîáőîäčěîńňüţ ęâŕëčôčęŕöčč đĺŕëčçóĺěîé ďđîäóęöčč äë˙ öĺëĺé ďđčěĺíĺíč˙ íŕëîăîâîé ńňŕâęč, ÷ňî ďđčâîäčň, â ňîě ÷čńëĺ, ę ńóäĺáíűě đŕçáčđŕňĺëüńňâŕě.

Ŕíŕëîăč÷íŕ˙ ŕäěčíčńňđŕňčâíŕ˙ íŕăđóçęŕ ëîćčňń˙ íŕ ňŕěîćĺííűĺ îđăŕíű ďđč ââîçĺ äŕííîé ďđîäóęöčč íŕ ňĺđđčňîđčţ Đîńńčéńęîé Ôĺäĺđŕöčč [3].

Âëč˙íčĺ ëüăîňű íŕ ýęîíîěčęó. Áîëüřŕ˙ (â ŕáńîëţňíîě âűđŕćĺíčč) ÷ŕńňü ńęđűňîé ńóáńčäčč, âîçíčęŕţůĺé âńëĺäńňâčĺ íŕëč÷č˙ ëüăîňű, ďîńňóďŕĺň áîëĺĺ áîăŕňűě ďîňđĺáčňĺë˙ě. Ďîńęîëüęó ÍÄŃ ýęîíîěč÷ĺńęč ˙âë˙ĺňń˙ íŕëîăîě íŕ ďîňđĺáëĺíčĺ ń řčđîęîé áŕçîé, ňî äîńňóď ę ňîâŕđŕě č óńëóăŕě, đĺŕëčçŕöč˙ ęîňîđűő îáëŕăŕĺňń˙ ďî ďîíčćĺííîé ńňŕâęĺ â đŕçěĺđĺ 10 %, čěĺţň íĺ ňîëüęî ńîöčŕëüíî íĺçŕůčůĺííűĺ, íî č ďđî÷čĺ ëčöŕ. Ďđč ýňîě â ńňđóęňóđĺ ďîňđĺáëĺíč˙ áîëĺĺ áîăŕňűő ăđŕćäŕí äîë˙ ëüăîňíűő ňîâŕđîâ č óńëóă ńîńňŕâë˙ĺň â ŕáńîëţňíîě çíŕ÷ĺíčč äŕćĺ áîëüřóţ âĺëč÷číó â ńčëó ňîăî, ÷ňî îíč áîëüřĺ ďîňđĺáë˙ţň â ŕáńîëţňíîě âűđŕćĺíčč [4]. Ýňî îňíîńčňń˙ ęî âńĺě ňîâŕđŕě č óńëóăŕě, ę ęîňîđűě â ńîîňâĺňńňâčč ń ď.2 ńň. 164 ÍĘ ĐÔ ďđčěĺí˙ţňń˙ ëüăîňíŕ˙ ńňŕâęŕ 10 %, âęëţ÷ŕ˙ îďĺđŕöčč ďî đĺŕëčçŕöčč áîëüřîăî ŕńńîđňčěĺíňŕ ďđîäîâîëüńňâĺííűő ňîâŕđîâ. Ďđč ýňîě äîë˙ âűăîäű íóćäŕţůčőń˙ ďîňđĺáčňĺëĺé â ŕáńîëţňíîě âűđŕćĺíčč – íŕčěĺíüřŕ˙ ńđĺäč ďîëó÷ŕňĺëĺé ńóáńčäčč. Ýňî, ďî ńóňč, ďđčâîäčň ę đĺăđĺńńčâíîěó íŕëîăîîáëîćĺíčţ, ęîăäŕ áîëĺĺ áîăŕňűĺ ďîëó÷ŕţň áîëüřóţ âĺëč÷číó íŕëîăîâűő ëüăîň, ÷ĺě ěĺíĺĺ áîăŕňűĺ, ÷ňî ďđîňčâîđĺ÷čň čäĺĺ ńďđŕâĺäëčâîăî ďĺđĺđŕńďđĺäĺëĺíč˙ ńđĺäńňâ č áîđüáű ń íĺđŕâĺíńňâîě ń ďîěîůüţ ďĺđĺđŕńďđĺäĺëčňĺëüíîé ôóíęöčč îáůĺńňâĺííűő ôčíŕíńîâ. Ďđč ýňîě â îňíîńčňĺëüíîě âűđŕćĺíčč ńęđűňŕ˙ ńóáńčäč˙ ńîńňŕâë˙ĺň áîëüřóţ äîëţ đŕńőîäîâ íŕ ďîňđĺáëĺíčĺ áĺäíĺéřčő ńëîĺâ íŕńĺëĺíč˙ ďî ńđŕâíĺíčţ ń áîëĺĺ áîăŕňűěč. Ýňč óňâĺđćäĺíč˙ ďîäňâĺđćäŕţň đĺçóëüňŕňű ďîâĺäĺííîăî â đŕěęŕő äŕííîăî čńńëĺäîâŕíč˙ ŕíŕëčçŕ äŕííűő đŕńďđĺäĺëčňĺëüíîăî ýôôĺęňŕ îň ďđčěĺíĺíč˙ ńňŕâęč ÍÄŃ â đŕçěĺđĺ 10 % â Đîńńčéńęîé Ôĺäĺđŕöčč.

Äë˙ ŕíŕëčçŕ čńďîëüçîâŕíŕ ěĺňîäîëîăč˙, ŕíŕëîăč÷íŕ˙ ďđĺäëŕăŕĺěîé â čńńëĺäîâŕíčč Keen (2013). Îňěĺňčě, ÷ňî íĺňî÷íîńňč â đĺçóëüňŕňŕő ŕíŕëčçŕ ěîăóň áűňü ńâ˙çŕíű ń ňĺě, ÷ňî íĺ ó÷ňĺíű đŕçëč÷č˙ â ďîňđĺáëĺíčč ďđîäóęňîâ, ďĺđĺ÷čńëĺííűő â ďď. 1 ď. 2 ńň. 164 ÍĘ ĐÔ, ěĺćäó áîăŕňűěč č áĺäíűěč ńëî˙ěč íŕńĺëĺíč˙. Îäíŕęî äŕííűĺ đŕçëč÷č˙ ďđĺäďîëîćčňĺëüíî ˙âë˙ţňń˙ íĺçíŕ÷čňĺëüíűěč, ó÷čňűâŕ˙ (1) íĺâęëţ÷ĺíčĺ đŕńőîäîâ íŕ ŕëęîăîëü â äŕííűĺ î đŕńőîäŕő íŕ ďđîäóęňű ďčňŕíč˙, (2) íŕëč÷čĺ â ďđîäŕćĺ ęŕę ďđĺěčŕëüíűő, ňŕę č äĺřĺâűő ňîâŕđîâ ňĺő âčäîâ, ęîňîđűĺ ďĺđĺ÷čńëĺíű â ďîäď. 1 ď. 2 ńň. 164 ÍĘ ĐÔ, (3) îáůóţ ęîíöĺďöčţ ďĺđĺ÷í˙ â ďîäď. 1 ď. 2 ńň. 164 ÍĘ ĐÔ, â ęîňîđűé âőîä˙ň îńíîâíűĺ ňîâŕđű ďđîäîâîëüńňâĺííîé ęîđçčíű ÷ĺëîâĺęŕ, íĺçŕâčńčěî îň ĺăî ńîöčŕëüíîăî ńëî˙ č óđîâí˙ äîőîäîâ.

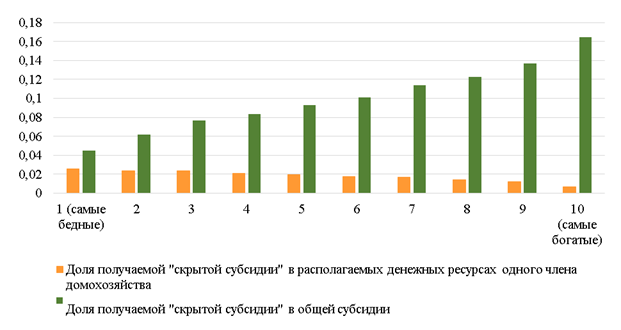

Đŕńďđĺäĺëčňĺëüíűé ýôôĺęň ńňŕâęč ÍÄŃ â đŕçěĺđĺ 10 % íŕ ďđîäóęňű ďčňŕíč˙ ďđĺäńňŕâëĺí íŕ đčńóíęĺ 2.

Đčńóíîę 2 – Đŕńďđĺäĺëčňĺëüíűé ýôôĺęň ńňŕâęč ÍÄŃ â đŕçěĺđĺ 10 % íŕ ďđîäóęňű ďčňŕíč˙

Čńňî÷íčę: ńîńňŕâëĺíî ŕâňîđŕěč íŕ îńíîâĺ äŕííűő Ôĺäĺđŕëüíîé ńëóćáű ăîńóäŕđńňâĺííîé ńňŕňčńňčęč çŕ III ęâŕđňŕë 2016 ă. (äîőîäű, đŕńőîäű č ďîňđĺáëĺíčĺ äîěŕříčő őîç˙éńňâ â 2016 ă. (ďî čňîăŕě âűáîđî÷íîăî îáńëĺäîâŕíč˙ áţäćĺňîâ äîěŕříčő őîç˙éńňâ).

Đĺçóëüňŕňű ďđîâĺäĺííîăî ŕíŕëčçŕ ďîęŕçŕëč, ÷ňî, íŕčáîëüřóţ ÷ŕńňü ńęđűňîé ńóáńčäčč â Đîńńčéńęîé Ôĺäĺđŕöčč (64 %) îň îáůĺé ńóěěű ďîëó÷ŕĺň áîëĺĺ áîăŕňŕ˙ ďîëîâčíŕ íŕëîăîďëŕňĺëüůčęîâ (řĺńňîé-äĺń˙ňűé äĺöčëč) ńî ńđĺäíĺěĺń˙÷íűěč đŕńďîëŕăŕĺěűěč äĺíĺćíűěč ńđĺäńňâŕěč âűřĺ 19 140,5 đóá. íŕ îäíîăî ÷ëĺíŕ äîěîőîç˙éńňâŕ.  ňî ćĺ âđĺě˙ íŕ ěĺíĺĺ áîăŕňóţ ďîëîâčíó ďîëó÷ŕňĺëĺé (ďĺđâűé-ď˙ňűé äĺöčëč) ńî ńđĺäíĺěĺń˙÷íűěč đŕńďîëŕăŕĺěűěč äĺíĺćíűěč äîőîäŕěč 15 954,1 đóá. č íčćĺ ďđčőîäčňń˙ ëčřü 36 % îň îáůĺé ńóěěű ńęđűňîé ńóáńčäčč. Ďđč ýňîě äîë˙ ńóáńčäčč ó ěĺíĺĺ îáĺńďĺ÷ĺííîé ďîëîâčíű íŕńĺëĺíč˙ ńîńňŕâë˙ĺň îňíîńčňĺëüíî áîëüřóţ ÷ŕńňü čő đŕńďîëŕăŕĺěűő äĺíĺćíűő ńđĺäńňâ: îň 2,6 % ó ńŕěűő áĺäíűő (ń đŕńďîëŕăŕĺěűěč đĺńóđńŕěč 5 945 đóá. â ěĺń˙ö) č äî 2,0 % ó ëčö čç ď˙ňîăî äĺöčë˙ (ń đŕńďîëŕăŕĺěűěč đĺńóđńŕěč 15 954,1 đóáëĺé â ěĺń˙ö).

Ńęđűňŕ˙ ńóáńčäč˙ â đŕçěĺđĺ đŕçíčöű ěĺćäó îáůĺé ńňŕâęîé íŕëîăŕ â đŕçěĺđĺ 18 % č ëüăîňíîé ńňŕâęîé (10 %) ÍÄŃ ďđĺäîńňŕâë˙ĺň ęîíęóđĺíňíîĺ ďđĺčěóůĺńňâî â âčäĺ âîçěîćíîńňč óńňŕíîâëĺíč˙ áîëĺĺ íčçęčő öĺí íŕ ńâîţ ďđîäóęöčţ äë˙ ďđîäŕâöîâ ëüăîňčđóĺěűő ďđîäîâîëüńňâĺííűő ňîâŕđîâ. Â đĺçóëüňŕňĺ čńęŕćŕţňń˙ đĺřĺíč˙ îá číâĺńňčöč˙ő č íŕđóřŕĺňń˙ îďňčěŕëüíîĺ đŕńďđĺäĺëĺíčĺ đĺńóđńîâ â ýęîíîěčęĺ.

Ňŕęčě îáđŕçîě đĺçóëüňŕňű ďđîâĺäĺííîăî čńńëĺäîâŕíč˙ ďîçâîë˙ţň çŕęëţ÷čňü, ÷ňî čńďîëüçîâŕíčĺ íŕëîăîâîé ëüăîňű â âčäĺ ďđčěĺíĺíč˙ ďîíčćĺííîé ńňŕâęč ÍÄŃ 10 % íŕ ďđîäóęňű ďčňŕíč˙ ˙âë˙ĺňń˙ íĺýôôĺęňčâíűě ěĺőŕíčçěîě äë˙ äîńňčćĺíč˙ öĺëč ńîöčŕëüíîé ďîääĺđćęč íŕčěĺíĺĺ îáĺńďĺ÷ĺííűő ńëîĺâ íŕńĺëĺíč˙. Íŕđ˙äó ń ýňčě, ýňîň ěĺőŕíčçě ÷ŕńňč÷íî âűďîëí˙ĺň ńâîţ çŕäŕ÷ó. Ęŕę ďîęŕçűâŕĺň ďđîâĺäĺííűé ŕíŕëčç, 36 % îň îáůĺé ńóěěű ńęđűňîé ńóáńčäčč čńďîëüçóĺňń˙ ëčöŕěč ń đŕńďîëŕăŕĺěűěč đĺńóđńŕěč čç íčćíčő 1-5 äĺöčëĺé íŕńĺëĺíč˙, ňî ĺńňü íŕčáîëĺĺ áĺäíîé ďîëîâčíîé íŕńĺëĺíč˙ Đîńńčéńęîé Ôĺäĺđŕöčč. Ďđč ýňîě ëčřü 11 % îň îáůĺé ńóěěű ńóáńčäčč ďîëó÷ŕţň ëčöŕ, ÷üč đŕńďîëŕăŕĺěűĺ đĺńóđńű ěĺíüřĺ ëčáî đŕâíű ďđîćčňî÷íîěó ěčíčěóěó.  ýňî ńâ˙çč öĺëĺńîîáđŕçíî îňěĺíčňü äŕííóţ ëüăîňó č čńďîëüçîâŕňü číűĺ, áîëĺĺ ŕäđĺńíűĺ, ěĺőŕíčçěű ďîääĺđćęč íŕčěĺíĺĺ îáĺńďĺ÷ĺííűő ńëîĺâ íŕńĺëĺíč˙, íŕďđčěĺđ, ďđ˙ěűĺ áţäćĺňíűĺ ňđŕíńôĺđňű. Ďđč ýňîě, â ńëó÷ŕĺ îňěĺíű ëüăîňű íĺîáőîäčěî îáĺńďĺ÷čňü ęîěďĺíńŕöčîííűé ěĺőŕíčçě äë˙ íŕčěĺíĺĺ îáĺńďĺ÷ĺííűő ńëîĺâ íŕńĺëĺíč˙.  ęŕ÷ĺńňâĺ ňŕęîăî ěĺőŕíčçěŕ ěîăóň âűńňóďčňü ďđ˙ěűĺ áţäćĺňíűĺ ňđŕíńôĺđňű íŕčáîëĺĺ áĺäíűě (íŕďđčěĺđ, ëčöŕě, âőîä˙ůčě â ďĺđâűĺ ď˙ňü äĺöčëĺé đŕńďîëŕăŕĺěűő äîőîäîâ) (ńě. ňŕáëčöó 1).

Îňěĺíŕ ëüăîňű ďđčâĺäĺň ę đîńňó äîőîäîâ áţäćĺňíîé ńčńňĺěű, çíŕ÷čňĺëüíî ďđĺâűřŕţůĺěó ńóěěű íĺîáőîäčěűő áţäćĺňíűő ňđŕíńôĺđňîâ íŕ ęîěďĺíńčđóţůčĺ ńóáńčäčč. Ňŕę, ńóěěŕ áţäćĺňíîăî ňđŕíńôĺđňŕ, íĺîáőîäčěîăî äë˙ ęîěďĺíńŕöčč ďîňĺđü â đĺçóëüňŕňĺ îňěĺíű ëüăîňű áîëĺĺ áĺäíîé ďîëîâčíĺ íŕńĺëĺíč˙ ďî ďđĺäâŕđčňĺëüíîé îöĺíęĺ ńîńňŕâčň 99,1 ěëđä đóá. Äŕćĺ ĺńëč äîďóńňčňü, ÷ňî čçäĺđćęč, ńâ˙çŕííűĺ ń ŕäěčíčńňđčđîâŕíčĺě äŕííîăî ňđŕíńôĺđňŕ, ńîńňŕâ˙ň ńóůĺńňâĺííóţ âĺëč÷číó, ňŕęŕ˙ ěĺđŕ ďđčíĺńĺň â áţäćĺň çíŕ÷čňĺëüíűĺ äîďîëíčňĺëüíűĺ äîőîäű (áîëĺĺ 100 ěëđä đóá.), ŕ ňŕęćĺ ďîçâîëčň óâĺëč÷čňü ýôôĺęňčâíîńňü đŕńőîäîâŕíč˙ áţäćĺňíűő ńđĺäńňâ č óńňđŕíčňü ýęîíîěč÷ĺńęčĺ čńęŕćĺíč˙, čěĺţůčĺń˙ â ńčëó íŕëč÷č˙ ëüăîňű. Ęđîěĺ ňîăî, îňěĺíŕ ëüăîňű ďđčâĺäĺň ę ĺäčíîđŕçîâîěó đîńňó číôë˙öčč â ńâ˙çč ńî çíŕ÷čňĺëüíîé äîëĺé ďđîäóęňîâ ďčňŕíč˙ â ďîňđĺáčňĺëüńęîé ęîđçčíĺ â ńâ˙çč ń ÷ĺě íĺîáőîäčěî ńâîĺâđĺěĺííîĺ číôîđěčđîâŕíčĺ ďđĺäńňŕâčňĺëĺé Öĺíňđŕëüíîăî Áŕíęŕ Đîńńčéńęîé Ôĺäĺđŕöčč î ďëŕíŕő îá îňěĺíĺ ëüăîňű ń ňĺě, ÷ňîáű îíč ńěîăëč ńęîđđĺęňčđîâŕňü ńâîč ňŕęňč÷ĺńęčĺ äĺéńňâč˙ ďî číôë˙öčîííîěó ňŕđăĺňčđîâŕíčţ. Ĺäčíîđŕçîâîĺ âëč˙íčĺ îňěĺíű ëüăîňű íŕ číôë˙öčţ ďî íŕřčě ďîäń÷ĺňŕě ńîńňŕâčň îęîëî 1,2% â ăîä ĺĺ îňěĺíű.

Ďîýňîěó, äë˙ ýôôĺęňčâíîé îňěĺíű äŕííîé ëüăîňű íĺîáőîäčěî đĺŕëčçîâŕňü ęîěďëĺęń ěĺđîďđč˙ňčé:

1. Ďđîŕíŕëčçčđîâŕňü ďîńëĺäńňâč˙ îňěĺíű ëüăîňű íŕ čçěĺíĺíčĺ öĺí, ńďđîńŕ č ďđĺäëîćĺíč˙ íŕ ëüăîňčđóĺěóţ ďđîäóęöčţ, ŕ ňŕęćĺ ýęîíîěč÷ĺńęčĺ ďîńëĺäńňâč˙ äë˙ ńîîňâĺňńňâóţůčő ďđĺäďđč˙ňčé ďčůĺâîé ďđîěűřëĺííîńňč. Đŕçđŕáîňŕňü ęîěďëĺęń ěĺđ (â ňîě ÷čńëĺ ôčíŕíńîâűő) äë˙ íčâĺëčđîâŕíč˙ íĺăŕňčâíűő ďîńëĺäńňâčé, ńâ˙çŕííűő ń čçěĺíĺíčĺě ńďđîńŕ.

2. Ďđîâĺńňč đŕńřčđĺííűĺ ńîöčŕëüíî-ýęîíîěč÷ĺńęčĺ čńńëĺäîâŕíč˙ ńňđóęňóđű ďîňđĺáëĺíč˙ ěŕëîčěóůčő ăđóďď íŕńĺëĺíč˙ ń öĺëüţ ňî÷íîăî îďđĺäĺëĺíč˙ đŕçěĺđŕ ęîěďĺíńŕöčč ďîâűřĺíč˙ đŕńőîäîâ íŕ ďčňŕíčĺ äë˙ óęŕçŕííűő ăđóďď.

3. Đŕçđŕáîňŕňü ďđŕęňč÷ĺńęčĺ ěĺőŕíčçěű ęîěďĺíńŕöčč ďîâűřĺíč˙ đŕńőîäîâ íŕ ďčňŕíčĺ, čńďîëüçó˙ äĺéńňâóţůčĺ ěĺőŕíčçěű (ďîâűřĺíčĺ ńîöčŕëüíűő ďîńîáčé č ďĺíńčé).

Çŕęëţ÷ĺíčĺ. Ęŕę ďîęŕçŕë ďđîâĺäĺííűé â äŕííîé đŕáîňĺ ŕíŕëčç, čńďîëüçîâŕíčĺ ďîíčćĺííűő ńňŕâîę ďî ÍÄŃ íŕ ďđîäóęňű ďčňŕíč˙ íĺ ˙âë˙ĺňń˙ ýôôĺęňčâíűě číńňđóěĺíňîě ăîńóäŕđńňâĺííűő ôčíŕíńîâ ń ňî÷ęč çđĺíč˙ äîńňčćĺíč˙ öĺëč ďîääĺđćęč íŕčáîëĺĺ áĺäíűő ńëîĺâ íŕńĺëĺíč˙. Áîëĺĺ ýôôĺęňčâíűě číńňđóěĺíňîě ˙âë˙ţňń˙ ďđ˙ěűĺ ňđŕíńôĺđňű íŕčáîëĺĺ áĺäíűě ńëî˙ě íŕńĺëĺíč˙ íŕ ďđîäóęňű ďčňŕíč˙, äŕćĺ ń ó÷ĺňîě çŕňđŕň íŕ ŕäěčíčńňđčđîâŕíčĺ. Äŕííűé đĺçóëüňŕň ńîâďŕäŕĺň ń đĺçóëüňŕňŕěč, îďóáëčęîâŕííűěč â đŕáîňĺ čńńëĺäîâŕňĺëĺé ďî ŕíŕëčçó čńďîëüçîâŕíč˙ ďîíčćĺííűő ńňŕâîę č îńâîáîćäĺíčé â îňäĺëüíűő ńňđŕíŕő, íŕďđčěĺđ, â Číäčč [4].

Îáůĺé đĺęîěĺíäŕöčĺé ďđč đŕçđŕáîňęĺ íŕëîăîâîé ďîëčňčęč â ÷ŕńňč ÍÄŃ ˙âë˙ĺňń˙ ěčíčěčçčđîâŕňü íŕđóřĺíčĺ íĺéňđŕëüíîńňč ďî ÍÄŃ:

1) íĺ čńďîëüçîâŕňü îńâîáîćäĺíčĺ îň ÍÄŃ, îńîáĺííî, ęîăäŕ îńâîáîćäŕĺňń˙ îň ÍÄŃ îďĺđŕöč˙, íŕőîä˙ůŕ˙ń˙ â ńĺđĺäčíĺ öĺďč ńîçäŕíč˙ ńňîčěîńňč â ęŕ÷ĺńňâĺ ńňčěóëčđóţůĺé ěĺđű. Ýôôĺęňű îň ňŕęîăî îńâîáîćäĺíč˙ íĺîäíîçíŕ÷íű č ňđóäíî ďđîń÷čňűâŕĺěű.  ÷ŕńňíîńňč, âîçíčęŕĺň ęŕńęŕäíîĺ äâîéíîĺ ýęîíîěč÷ĺńęîĺ íŕëîăîîáëîćĺíčĺ, âîçěîćíîńňü čńďîëüçîâŕíč˙ ńőĺě ěčíčěčçŕöčč. Ďđč ýňîě ńňčěóëčđóţůčé ýôôĺęň ěčíčěŕëĺí;

2) čńďîëüçîâŕňü ďđčíöčď ńňđŕíű íŕçíŕ÷ĺíč˙ č ěĺńňŕ íŕőîćäĺíč˙ ďîęóďŕňĺë˙ â ęŕ÷ĺńňâĺ îńíîâíîăî ďđŕâčëŕ îďđĺäĺëĺíč˙ ěĺńňŕ đĺŕëčçŕöčč óńëóă äë˙ öĺëĺé ÍÄŃ ďđč ěĺćäóíŕđîäíîé ňîđăîâëĺ.  ďđîňčâíîě ńëó÷ŕĺ íŕđóřŕĺňń˙ íĺéňđŕëüíîńňü ÍÄŃ, âîçíčęŕĺň äâîéíîĺ íŕëîăîîáëîćĺíčĺ ýęńďîđňŕ č íĺîáëîćĺíčĺ čěďîđňŕ č âîçěîćíîńňü čńďîëüçîâŕíč˙ ńőĺě äë˙ óęëîíĺíč˙;

3) óđĺăóëčđîâŕňü ńčňóŕöčč âçŕčěîäĺéńňâč˙ ëčö, ˙âë˙ţůčőń˙ íŕëîăîďëŕňĺëüůčęŕěč ÍÄŃ, č ëčö, íĺ ˙âë˙ţůčőń˙ íŕëîăîďëŕňĺëüůčęŕěč ÍÄŃ, â îňíîřĺíčč ďđŕâŕ íŕ âű÷ĺň âőîä˙ůĺăî íŕëîăŕ;

4) ěčíčěčçčđîâŕňü ďđčěĺíĺíčĺ ďîíčćĺííűő ńňŕâîę ďî ÍÄŃ.

Ňŕáëčöŕ 1 – Đŕńďđĺäĺëčňĺëüíűé ýôôĺęň ńňŕâęč ÍÄŃ 10% íŕ ďđîäóęňű ďčňŕíč˙

|

Ďîęŕçŕňĺëü

|

Đŕńďđĺäĺëĺíčĺ ńđĺäíĺäóřĺâűő đŕńďîëŕăŕĺěűő đĺńóđńîâ îäíîăî ÷ëĺíŕ äîěîőîç˙éńňâŕ ďî 10 %-ě (äĺöčëüíűě) đŕâíűě ăđóďďŕě íŕńĺëĺíč˙*

|

|

1

|

2

|

3

|

4

|

5

|

6

|

7

|

8

|

9

|

10

|

|

(ńŕěűĺ áĺäíűĺ)

|

(ńŕěűĺ áîăŕňűĺ)

|

|

Äĺíĺćíűĺ đŕńőîäű íŕ ďčňŕíčĺ, % îň đŕńďîëŕăŕĺěűő đĺńóđńîâ

|

38

|

34

|

34

|

31

|

29

|

26

|

24

|

21

|

17

|

10

|

|

Đŕçěĺđ ńęđűňîé ńóáńčäčč îň ďđčěĺíĺíč˙ ńňŕâęč ÍÄŃ 10% íŕ ďđîäóęňű ďčňŕíč˙, ěëđä. đóá.

|

13,8

|

16,5

|

22,0

|

22,0

|

24,8

|

27,5

|

30,3

|

33,0

|

38,5

|

44,0

|

|

Äîë˙ ńęđűňîé ńóáńčäčč â đĺńóđńŕő ďđĺäńňŕâčňĺë˙ äŕííîé ăđóďďű íŕńĺëĺíč˙, %

|

2,6

|

2,3

|

2,3

|

2,1

|

2

|

1,8

|

1,7

|

1,4

|

1,2

|

0,7

|

|

Äîë˙ ńęđűňîé ńóáńčäčč â îáůĺě đŕçěĺđĺ ńóáńčäčč, %

|

5

|

6

|

8

|

8

|

9

|

10

|

11

|

12

|

14

|

16

|

|

Ęîěďĺíńŕöčîííűé ňđŕíńôĺđň â ńëó÷ŕĺ îňěĺíű ëüăîňíîé ńňŕâęč ÍÄŃ, ěëđä đóá.

|

13,8

|

16,5

|

22,0

|

22,0

|

24,8

|

0

|

0

|

0

|

0

|

0

|

|

Ďđčěĺ÷ŕíčĺ:

* Çäĺńü č äŕëĺĺ â ăđóďďčđîâęŕő ďî äĺöčë˙ě ďĺđâŕ˙ č äĺń˙ňŕ˙ ăđóďďű îçíŕ÷ŕţň: ďĺđâŕ˙ – ń íŕčěĺíüřčěč đŕńďîëŕăŕĺěűěč đĺńóđńŕěč, äĺń˙ňŕ˙ – ń íŕčáîëüřčěč đŕńďîëŕăŕĺěűěč đĺńóđńŕěč. Íŕ÷číŕ˙ ń 2016 ă. ôîđěčđîâŕíčĺ äĺöčëüíűő ăđóďď îńóůĺńňâë˙ĺňń˙ íŕ îńíîâĺ îáúĺäčíĺííîăî ěŕńńčâŕ ďî Đîńńčč â öĺëîě. Äŕííűĺ íĺ ńîďîńňŕâčěű ń áîëĺĺ đŕííčěč ďĺđčîäŕěč.

|

Čńňî÷íčę: đŕńń÷čňŕíî ŕâňîđŕěč ďî äŕííűě Ôĺäĺđŕëüíîé ńëóćáű ăîńóäŕđńňâĺííîé ńňŕňčńňčęč çŕ III ęâŕđňŕë 2016 ă. (äîőîäű, đŕńőîäű č ďîňđĺáëĺíčĺ äîěŕříčő őîç˙éńňâ â 2016 ă. (ďî čňîăŕě âűáîđî÷íîăî îáńëĺäîâŕíč˙ áţäćĺňîâ äîěŕříčő őîç˙éńňâ).

References

1. Nalogovyi kodeks Rossiiskoi Federatsii (chast' vtoraya): [feder. zakon: prinyat Gos. Dumoi 19.07.2000 ą 117-FZ (red. ot 05.10.2015)]. [Elektronnyi resurs] // SPS «Konsul'tant plyus»: Zakonodatel'stvo: Versiya Prof. – Rezhim dostupa: http://base.consultant.ru/

2. Tsentr strategicheskikh razrabotok [Elektronnyi resurs] – Rezhim dostupa: https://www.csr.ru/

3. O stavke NDS v razmere 10% v otnoshenii prodovol'stvennykh i meditsinskikh tovarov, vvozimykh i realizuemykh v RF [pis'mo Minfina Rossii ot 04.08.2014 ą 03-07-07/38358]. [Elektronnyi resurs] // SPS «Konsul'tant plyus»: Finansovye i kadrovye konsul'tatsii: Versiya Prof. – Rezhim dostupa: http://base.consultant.ru

4. Keen M. Targeting, Cascading, and Indirect Tax Design. IMF Working Paper. February 2013.

5. Federal'naya sluzhba gosudarstvennoi statistiki [Elektronnyi resurs] / sait Rosstata Rossii – Rezhim dostupa: http://www.gks.ru/

6. Semenikhin V.V. Nalog na dobavlennuyu stoimost': realizatsiya prodovol'stvennykh tovarov // Nalogi. 2014. N 41. S. 13-18.

7. Tyapukhin S.V. Pravomernost' primeneniya stavki NDS 10 % nuzhno podtverdit' // Torgovlya: bukhgalterskii uchet i nalogooblozhenie. 2016. N 3. S. 69-73.

8. Milogolov N.S. NDS po operatsiyam mezhdunarodnoi torgovli uslugami // Nauchno-issledovatel'skii finansovyi institut. Finansovyi zhurnal. 2013. ą 3 (17). S. 117-122.

9. Gurvich E.T. Dinamika sobiraemosti nalogov v Rossii: makroekonomicheskii podkhod // Nauchno-issledovatel'skii finansovyi institut. Finansovyi zhurnal. 2015. ą 4 (26). S. 22-33.

10. Malis N.I. Nalogovaya politika na srednesrochnyi period: optimizatsiya l'got i stimulirovanie investitsii // Nauchno-issledovatel'skii finansovyi institut. Finansovyi zhurnal. 2014. ą 3 (21). S. 89-95.

11. Pinskaya M.R., Savina O.N., Savina E.O. Aktual'nye voprosy ucheta naloga na dobavlennuyu stoimost' / Nalogi i nalogooblozhenie. 2015. ą 4 (130). - S. 319-327.

|

Eng

Eng